-

07 August 2025 | Policy Analysis

Budget legislation expected to result in 16 million more uninsured -

02 August 2025 | Country Update

“One Big Beautiful Bill” Act will severely impact rural healthcare -

05 September 2024 | Policy Analysis

Oregon Further Expands Public Insurance Using Affordable Care Act’s Basic Health Program -

01 June 2024 | Policy Analysis

Reforming Medicare Advantage -

02 February 2024 | Country Update

Record Enrollment in Affordable Care Act Marketplace Plans 10 Years after Opening -

02 February 2024 | Country Update

California Provides Medicaid Eligibility to All Undocumented Residents -

02 February 2024 | Policy Analysis

Rise of Uninsured with post-COVID-19 Medicaid Disenrollment -

01 May 2023 | Country Update

New Maximums on Insulin Prices -

01 May 2023 | Country Update

Enrollment in Obamacare Marketplaces Increases after Boost to Subsidies Extended -

01 May 2023 | Policy Analysis

Rise of Uninsured with Lifting of COVID-19 Emergency Measures

3.3. Overview of the statutory financing system

Each US state is required to provide a set of mandatory health benefits to qualifying citizens under federal law, with an option to provide additional benefits through the state planning process and legislature. Better known as Medicaid and the Children’s Health Insurance Program (CHIP), each state’s health plan is funded through federal and state dollars. In the state of Oregon, the Oregon Health Plan (OHP) has provided Medicaid and CHIP to its citizens since 1993 [1]. Often recognized as a national leader in health care reform through broad coverage eligibility criteria, the state covers 1.4 million Oregonians who earn up to 138% of the federal poverty level (FPL), or roughly $21,000/year for one person, or more than $43,000/year for a family of four [1, 2].

In 2024, Oregon used Section 1331 of the Affordable Care Act to further expand eligibility for publicly funded health insurance from 138% to 200% of FPL for people who would otherwise be eligible for federally subsidized marketplace coverage. This policy change increases the income limit to qualify for public insurance in Oregon to $30,000/year for individuals ($62,400/year for a family of four) [3].

In addition to reducing transitions on to and off of public insurance, referred to as “churn”, Oregon’s Basic Health Program uses mostly federal dollars to provide tens of thousands more people coverage for essential health benefits without premiums or co-pays. The uninsured rate in Oregon prior to the eligibility expansion was 6% [5], and officials expect the plan to cover 100,000 individuals by 2027, 30,000 of whom would not have had insurance otherwise [5].

Only two other states, New York and Minnesota, have expanded their Medicaid benefits beyond the traditional federal income limits allowed under the Affordable Care Act (138%), yet Oregon is the first do so without passing on premiums or cost-sharing to Basic Health Plan enrollees.

References

[1] Oregon Health Authority. Brief history of health services prioritization in Oregon. Available from: https://www.oregon.gov/oha/HPA/DSI-HERC/Documents/Brief-History-Health-Services-Prioritization-Oregon.pdf

[2] OPB. Oregon health plan eligibility checks near completion. Available from: https://www.opb.org/article/2024/07/02/oregon-health-plan-eligibility-checks-near-completion

[3] Medicaid Planning Assistance. Federal poverty guidelines. Available from: https://www.medicaidplanningassistance.org/federal-poverty-guidelines

[4] Oregon Health Authority. Oregon Health Plan Bridge program. Available from: https://www.oregon.gov/oha/hsd/ohp/pages/bridge.aspx?utm_medium%3Demail%26utm_source%3Dgovdelivery

[5] Oregon Health Authority. Basic Health Program presentation. 2023 Jul 11. Available from: https://www.oregon.gov/oha/OHPB/MtgDocs/5.0%20Basic%20Health%20Program%20presentation_07.11.23.pdf

Traditionally Medicare, the public insurance program for seniors, the disabled, and those with other select medical conditions, was managed directly through the public system. This changed in 1997 when the Centers for Medicare and Medicaid Services (CMS) offered beneficiaries an option to receive their coverage through private insurance companies, called Medicare Part C, or Medicare Advantage (MA).

The attractiveness of MA is its expanded coverage and other benefits. Whereas many MA plans cover dental, vision, hearing and drugs, traditional Medicare does not, and beneficiaries must take out supplemental policies to expand coverage to this level. Other differences are that MA may pay all or part of the Medicare Part B (outpatient) premium, and may add non-health benefits, such as gym or food club memberships.

With these perceived advantages to traditional Medicare, and with encouragement from the federal government and aggressive advertising by MA plans, the MA enrollment rate has grown, especially in the past few years. In 2023, 51% of all Medicare beneficiaries were enrolled in MA plans (Ochieng, et al. 2023).

However, MA has some serious disadvantages compared to traditional Medicare. MA beneficiaries generally are required to stay within often narrow care networks, which may not include providers they need. Meanwhile, traditional Medicare beneficiaries can see any provider they want. MA plans have more prior authorization restrictions and higher claim denial rates than traditional Medicare. And many of the denied claims – 1.5 million last year – are wrongful (Grimm, 2022). MA plans may restrict benefits, such as the number of hospital days covered or the drugs in their formulary. The supplemental benefits, like dental and hearing, typically have spending limits that can result in high out-of-pocket costs for many. Finally, it is difficult for prospective beneficiaries to discern these issues prior to signing up for MA, or to determine differences between MA plans.

Moreover, providers have difficulties with MA. They spend much time filling out authorization forms and arguing with insurers to get necessary care approved. Seeing their patients go without needed tests and treatments can take a toll on their morale. They also face delays in, or lack of, payment from the MA company.

Recently, more disadvantages to MA have emerged. The Medicare Payment Advisory Commission (MedPAC), an independent body advising Congress on Medicare, estimates that MA has been overcharging the government for its services by 22%, or by $83 billion a year (MedPAC, 2024a), purportedly by selecting less-sick patients and upcoding their conditions. The Commission estimates that Medicare Part B premiums will be about $13 billion higher in 2024 because of higher MA spending.

Despite these drawbacks, MedPAC believes that patients have the right to choose between the two types of Medicare. Some may want to avoid the provider network and utilization constraints whereas others may prefer the additional benefits found in MA. At the same time MedPAC calls for a major overhaul of the MA program (MedPAC, 2024b). Areas needing improvement are the coding system, risk adjustments, the quality bonus system, and the transparency of plan benefits and restrictions (MedPAC, 2024a; MedPAC, 2024b). Additionally, the CMS is cutting MA payments slightly: base payment will fall 0.16% in 2025 (Herman, 2024).

Authors

References

Grimm, C.A. (2022). Some Medicare Advantage organization denials of prior authorization requests raise concerns about beneficiary access to medically necessary care. Office of Inspector General, Report in Brief, April 2022. https://oig.hhs.gov/oei/reports/oei-09-18-00260.asp

Herman, B. (2024). Biden administration sticks with slight cuts to 2025 Medicare Advantage payments. Stat News, 1 April 2024. https://www.statnews.com/2024/04/01/joe-biden-2025-medicare-advantage-payment-health-insurance

MedPAC (2024a). MedPAC releases March 2024 Report to the Congress: Medicare Payment Policy. 15 March 2024. https://www.medpac.gov/document/medpac-releases-march-2024-report-to-the-congress-medicare-payment-policy

MedPAC (2024b). MedPAC March 2024 Report to the Congress: Executive Summary. https://www.medpac.gov/document/march-2024-report-to-the-congress-medicare-payment-policy

Ochieng, N., Biniek, J.F., Freed, M., Damico, A., and Neuman, T. (2023) Medicare Advantage in 2023: Enrollment update and key trends. Kaiser Family Foundation. 9 August 2023. https://www.kff.org/medicare/issue-brief/medicare-advantage-in-2023-enrollment-update-and-key-trends

During the most recent open enrollment period for the Affordable Care Act (ACA), or Obamacare, an additional two million people took advantage of enhanced subsidies to purchase Marketplace coverage. As of its 13th anniversary, over 16 million Americans, a new record, now receive coverage through Obamacare’s Marketplaces. The recent enrollment surge is due in part to enhanced subsidies that were included during the COVID-era American Rescue Plan and recently extended through 2025 as part of the Inflation Reduction Act. In the coming year, many more Americans may need enhanced subsidies as they transition to the Marketplace after losing their Medicaid coverage as another COVID-era policy that maintained Medicaid enrollees’ eligibility begins to unwind.

Authors

References

Biden-Harris Administration Celebrates the Affordable Care Act’s 13th Anniversary and Highlights Record-Breaking Coverage. HHS.gov. Published March 23, 2023. Accessed April 11, 2023. https://www.hhs.gov/about/news/2023/03/23/biden-harris-administration-celebrates-affordable-care-acts-13th-anniversary-highlights-record-breaking-coverage.html

Cox C, Pollitz K, Ortaliza J. Nine Changes to Watch in ACA Open Enrollment 2023. KFF. Published October 27, 2022. Accessed April 11, 2023. https://www.kff.org/policy-watch/nine-changes-to-watch-in-open-enrollment-2023

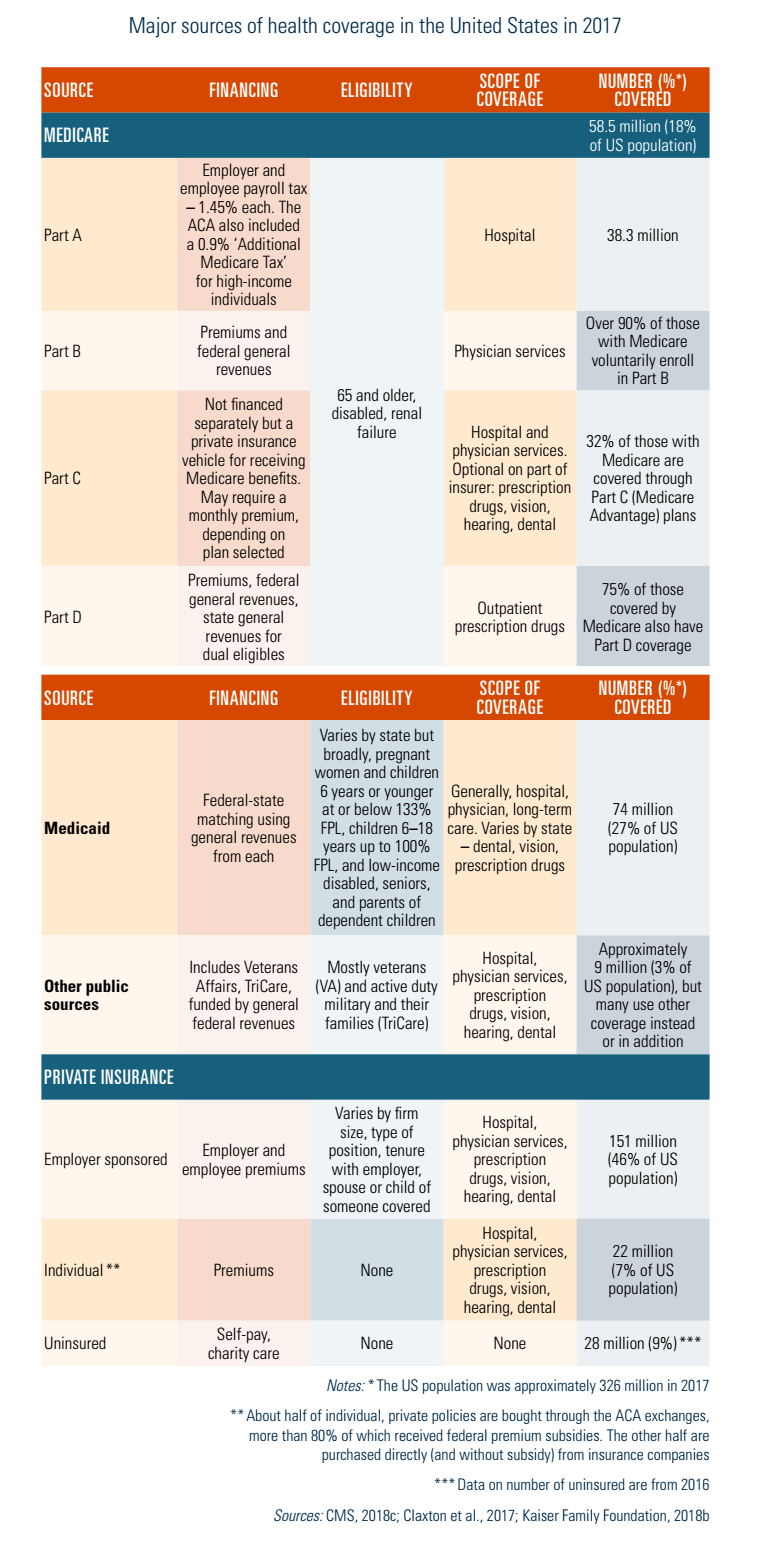

3.3.1. Medicare

The next three sections discuss the major sources of coverage in the United States. Table3.5 presents a summary of the sources of health care coverage, how they are financed, who is eligible, and the breadth, depth and scope of coverage as of 2017. Unlike citizens in other high-income countries, only a minority of the US population is covered by the public financing system, mainly through Medicare (seniors and disabled people) and Medicaid (poor and near-poor population); the latter is discussed in section 3.3.2. Rather, a majority of the population receives their coverage from private health insurance and most of them obtain it through an employer (section 3.5).

Table3.5

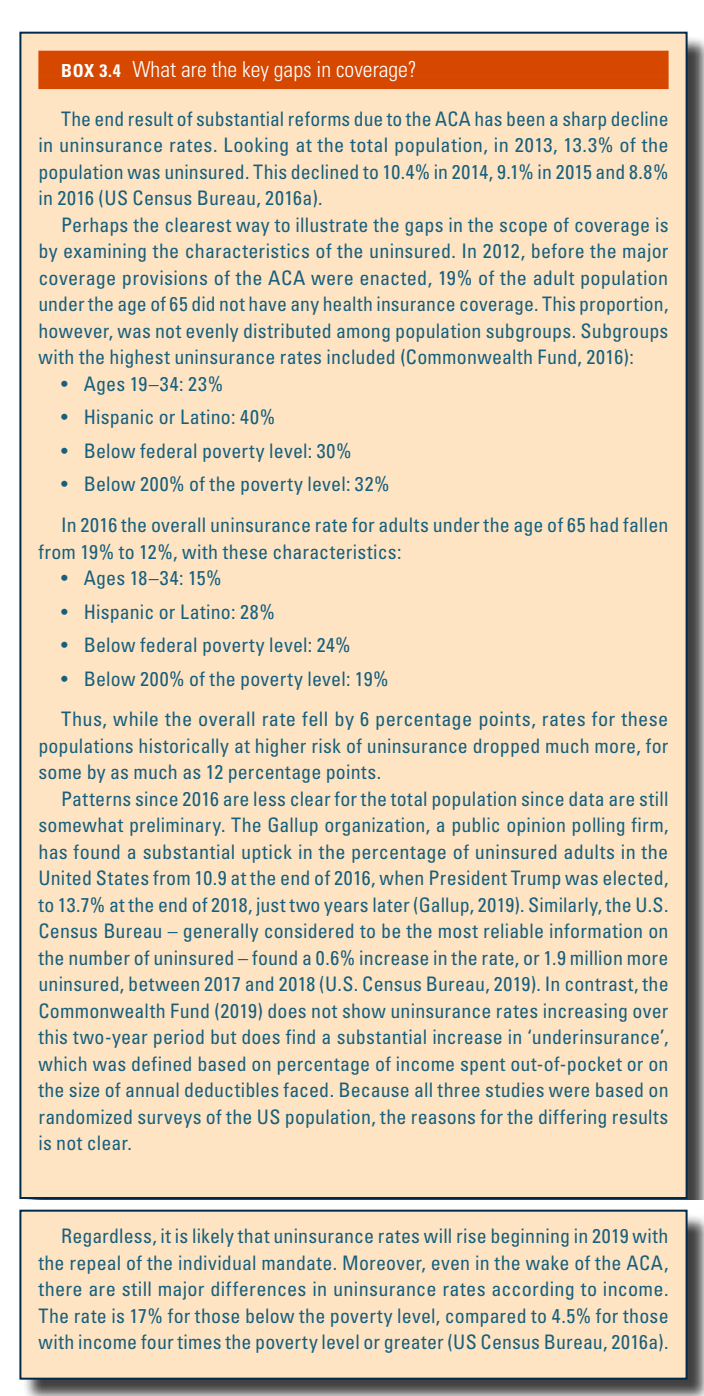

It is noteworthy, however, that the ACA expanded both the public and private sectors, both of which resulted in a decline in the number of uninsured persons (see Box3.4) More uninsured poor and near-poor individuals and families are receiving Medicaid coverage in the states that chose optional expansion, and many others who are uninsured, whose incomes are too high to qualify for Medicaid, are receiving subsidies that are used to purchase private health insurance. Before discussing these types of coverage, however, the Medicare programme is described.

Box3.4

Coverage

Breadth of coverage

The Medicare programme provides health insurance coverage to nearly all Americans aged 65 and older, as well as to many disabled Americans – those who have received federal disability payments for two or more years, as well as people with end-stage renal disease and amyotrophic lateral sclerosis (ALS) (64 million people, 18% of the total US population in 2018). Medicare is divided into four parts, labelled Parts A, B, C and D.

- Part A, Hospital Coverage includes not only hospital care, but also some post-acute nursing home, home health and hospice care. Individuals and their spouses aged 65 and older who worked for at least 10 years during which time they contributed federal payroll taxes that supported both Social Security (the US statutory retirement pension system) and Medicare are entitled to Part A coverage. In 2017, 58.5 million people were enrolled (CMS, 2018a).

- Part B, Supplemental Medical Insurance is a voluntary programme with essentially the same eligibility requirements as Part A. It covers physicians’ services (both inpatient and outpatient); outpatient care; medical equipment, tests and X-rays; home health care; some preventive care; and a variety of other medical services. Despite its voluntary nature, over 90% of those eligible enrol in it because it is heavily subsidized, as discussed in subsection Revenue collection below.

- Part C, Medicare Advantage is an alternative to Parts A and B. Enrolment is voluntary. It provides coverage for the same services and, at the discretion of the organization offering coverage, sometimes additional benefits such as vision, hearing and/or dental care. One of the main differences between Part C and the preceding two Parts, which are sometimes called “traditional Medicare”, is that Part C coverage is offered through private organizations (e.g. insurers and HMOs). Put another way, when a beneficiary receives a service under Part A or B, the Medicare programme pays the provider directly for services (though payments are processed through private organizations called Medicare Administrative Contractors (MACs)). In contrast, under Part C, Medicare pays the Medicare Advantage plan a fixed amount of money per month for each enrollee based on the characteristics (e.g. demographics, medical diagnoses) of the particular enrollees in the plan. (The formula is a complicated one that has been revised several times over the years.) Enrollees sometimes also pay a premium to the Part C health plan depending on the size of the plan’s bid for providing services; the average in 2017 was US$ 36 per month (Kaiser Family Foundation, 2017c).

- Part D, Prescription Drug Coverage began in 2006 and is also voluntary. Prior to that, Medicare did not provide coverage for prescription drugs received outside hospital. Similar to Part C, Part D benefits are provided through private organizations (usually insurers, HMOs or PPOs). In 2018 there were typically two dozen choices among Part D plans in each state – in addition to dozens of Medicare Advantage plans providing drug coverage in many urban areas. Like Part C, premiums and benefits vary by plan, with competition occurring based not only on premium differences, but also on differences in benefits and, in particular, the drugs that are included on a plan’s formulary that are listed as “preferred” drugs and which therefore are subject to lower or zero patient co-payments.

Research has shown that, historically, Part C plans have been paid more than their costs (CBO, 2007). As a result, the ACA introduced significant changes to payment rate calculations in order to reduce the gap between payment and average expenditure per enrollee. These efforts have been successful: average payments to Part C plans were 114% of traditional Medicare spending per enrollee in 2009, and by 2018 that figure had been reduced to 101% (Skopec et al., 2019). For this payment, a Part C organization is responsible for providing or paying for the service, enjoying part of the financial gain from excess revenues and being at risk of financial loss for shortfalls. A second difference from traditional Medicare is that Medicare Advantage plans tend to cover beneficiaries living in a defined geographical area, covering one or more counties (a geographical subdivision of a state). Thirdly, plans compete with one another in part on the basis of premiums. That is, rather than all beneficiaries paying the same premium, as they do under Part B, in Part C each plan sets its own premium, which will depend not only on the costs of providing required services but also whether additional benefits are offered. Premiums are paid directly to health plans. Fourthly, as noted, most Medicare Advantage plans offer coverage for some types of services not covered by Parts A and B, such as vision, hearing or dental care.

The specific benefits under Part C depend on the type of health plan in which a beneficiary enrols. HMOs are the most common, followed by PPOs and private FFS plans. The last of these is different from the others in various ways: enrollees are generally not limited to a particular network or providers; providers can charge more, meaning that OOP expenses can be higher than with other Part C plans such as HMOs; and physicians typically are paid on a FFS basis. The law allowing for private FFS plans was established by Congress in 1997 as an option for beneficiaries who did not want to be subject to utilization management techniques typically used by managed care plans (Miller, 2007).

In 2017, 34% of Medicare beneficiaries were enrolled in Medicare Advantage plans, nearly 50% higher than just five years before. The remaining 65% remained in “traditional Medicare”. While it was anticipated that cuts in payment to Medicare Advantage plans under the ACA would reduce enrolment by as much as 35%, this did not occur, with the proportion of beneficiaries joining them continuing to rise through 2017. This appears to have occurred because plans responded to payment reductions by reducing their costs, while still offering optional benefits not available through traditional Medicare (Guterman, Skopec & Zuckerman, 2018).

About 75% of Medicare beneficiaries are covered under Part D – about 60% from “stand-alone” plans that provide coverage only for prescription drugs, and the remaining 40% from the drug benefits provided through Medicare Advantage plans (Kaiser Family Foundation, 2019b). Most other beneficiaries have drug coverage from another source, such as from a former employer, but 15% do not have any drug coverage (Kaiser Family Foundation, 2019b).

Scope of coverage

In general, Medicare covers most medically necessary services as determined by providers. Unlike many private health insurance plans, pre-authorization is not required for hospitalizations. With the onset of coverage of outpatient prescription drugs in 2006, and the gradual increase in coverage for preventive services in recent years (which is being expanded through the ACA), the main services not covered are extended long-term care and dental care. There are a few other explicit exclusions: cosmetic surgery, acupuncture, hearing aids and, except in limited circumstances, glasses. Some of these services, however, are covered under selected Medicare Advantage plans.

The largest of these excluded services is extended long-term care. Precisely which services are covered by Medicare is rather complex because the programme does include some coverage for nursing home and home health care. This coverage, however, is aimed at acute-care illnesses. Skilled nursing care must be deemed medically necessary by a physician; custodial care is not covered. Moreover, nursing home care can only be covered if it follows an inpatient hospital stay of at least three days and coverage is provided for a maximum of 100 consecutive days.

Medicare is not involved in determining whether a particular service to a specific beneficiary is covered. Rather, these decisions are generally made by private organizations that contract with Medicare. This is a result of a compromise between legislators and providers to assuage provider concerns about the government making coverage decisions, dating back to the mid-1960s when the Medicare legislation was being debated in Congress. Under Parts A and B, Medicare contracts with MACs. Coverage decisions are made directly by the private health plan under Parts C and D. The Medicare programme has a formal appeals process when disputes occur (see section 2.8.4).

Depth of coverage

As implied above, Medicare coverage is both broad and wide: nearly all seniors are covered and almost all services are covered, the two major exceptions being long-term care and routine dental care. Coverage is not as deep, however. As a result, almost 90% of all beneficiaries obtain some form of supplemental insurance coverage. In 2015 Medicare paid just over half – 54% – of total medical and long-term care expenses. Another 9% was paid on behalf of beneficiaries by Medicare Advantage (Part C) managed care plans; an additional 7% was paid by private payers (including employers and Medigap insurers); 7% was paid by Medicaid on behalf of low-income beneficiaries; 6% was paid by miscellaneous sources including the VHA, and the remaining 17% constituted direct, OOP spending. Note that the above figures do not include premium payments made by beneficiaries (computations made by Kaiser Family Foundation for the authors based on 2015 Medicare Current Beneficiary Survey Data).

Coverage for hospital care under Part A contains two significant gaps. Firstly, there is a deductible for each inpatient hospital stay; in 2018 the amount was US$ 1340. Secondly, for those rare stays that exceed 60 days, there are substantial daily co-payments: US$ 335 per day for days 61–90 and US$ 670 per day for days 91–150.[5] There are no monthly premiums for Part A.

As noted, Part A’s nursing home coverage is limited because it is only for short-term skilled care following a hospital admission, rather than for long-term care. For eligible stays, up to 100 days are covered. During the first 20 days there are no co-payments, but there is a substantial daily co-payment for days 21–100 of a stay: US$ 168 in 2018. In contrast, there is no co-payment for home health care services.

Coverage for physicians’ and other medical services under Part B are also subject to patient cost-sharing. The patient is responsible for 20% of all covered expenses (with no maximum) after meeting an annual deductible of US$ 183 in 2018. The 20% coinsurance requirement is perhaps the main reason why the vast majority of Medicare beneficiaries seek some form of supplemental insurance coverage, which is discussed below. Monthly premiums vary by income; individuals with incomes below US$ 85 000 or couples with incomes below US$ 170 000 paid US$ 134 per month in 2018. Those with higher income pay considerably more. Premiums are often deducted from Social Security payments.

It is difficult to generalize about the depth of coverage under Part C because each plan has its own benefit structure. Federal minimum requirements are that coverage be at least as comprehensive as under Parts A and B. As noted, most Part C plans offer additional services, including prescription drug coverage. Those enrolling in Part C generally are required to pay the US$ 134 Part B premium, and many pay additional amounts based on the total cost of the plan they choose.

Beneficiaries obtain outpatient prescription drug coverage in one of three ways: a Part C Medicare Advantage plan (discussed above), a stand-alone drug insurance plan called a Prescription Drug Plan (PDP) under Part D of Medicare, or employer-provided job or retiree health insurance coverage. In 2018 premiums for PDPs averaged US$ 43 a month (Kaiser Family Foundation, 2019b).

Whereas Part D drug benefits vary depending on a particular plan’s benefit structure, there is a standard benefit structure that health plans are allowed to offer that in 2018 had the following benefits. The beneficiary paid a US$ 405 annual deductible for drug expenses. For annual drug spending between US$ 405 and US$ 3700, the plan paid 75% of expenses and thus the beneficiary was subject to a 25% coinsurance rate. After that, the beneficiary enters the “doughnut hole” where there is no coverage at all. After spending US$ 5000 annually in OOP costs, Medicare generally covers 95% of remaining costs. Importantly, even 5% patient cost-sharing can cause considerable financial harm for those with chronic diseases who use extremely expensive brand-name drugs. At the time of writing various Congressional legislative proposals are being considered to deal with this problem.

As noted, almost 90% of Medicare beneficiaries have some form of supplemental insurance coverage. The main sources in 2013 were as follows (Kaiser Family Foundation, 2017d).

- Former (and occasionally, current) employers: 22% of beneficiaries have such coverage. It is considered desirable because it often covers a greater share of expenses than private (“Medigap”) insurance and because premiums are usually partially subsidized by the employer.

- Medicare Advantage plans: 34% have this form of coverage. It is usually included as a form of supplemental insurance because, as noted, these plans tend to cover some expenses beyond what is paid for by Parts A and B.

- Medicaid: 15% have this coverage, which is available to Medicare beneficiaries with low incomes and assets. This group, which qualifies for both Medicaid and Medicare, is referred to as “dual eligible”. It covers most services at zero or nominal costs. Of note is the fact that Medicaid often becomes a payer of last resort when a beneficiary is institutionalized in a nursing home and “spends down” their income and assets.

- Medigap: 15% of beneficiaries purchase (unsubsidized) private health insurance. Premiums vary by health plan; to illustrate, the annual premium cost of the most popular benefit configuration in California in 2010, for a 65-year-old woman, varied from US$ 1626 (from the lowest cost insurer) to US$ 5467 (the highest cost insurer) (California Department of Insurance, 2010).

The Medigap market is unusual in two respects. Firstly, unlike most other types of insurance, in which states are responsible for insurance regulation, Medigap is subject to strong federal oversight. Secondly, Medigap policies must conform to strict benefit standardization requirements; health plans are only allowed to sell benefit configurations that exactly match federal standards. This facilitates comparison shopping; once the beneficiary chooses among the modest number of benefit designations desired, all insurance plans must provide exactly those (and no more) benefits, which means that the beneficiary mainly needs to compare premiums across the various plan choices.

Revenue collection

Revenue collection differs among the various parts of Medicare. Part A was designed to be a social insurance programme, and accordingly it is financed almost entirely (excepting beneficiary cost-sharing requirements) through a payroll tax with nearly all seniors as well as many disabled Americans automatically eligible for coverage. Parts B and D, in contrast, are voluntary and funded by a combination of general revenue and premium contributions by beneficiaries. Part C is funded by sources similar to Parts A and B.

Overview of Medicare expenditures

In 2016 total Medicare expenditures were US$ 679 billion (Boards of Trustees, 2017). It is difficult to break this down by type of service because that is only done for the 66% of beneficiaries who are not in Medicare Advantage plans. Among those in the so-called “traditional” (FFS) Medicare, 30% is spent on inpatient hospital care and 14% on physicians’ services. Other key components are outpatient prescription drugs (20%) and hospital outpatient services (10%). In spite of the fact that Medicare services seniors and the disabled populations, just 10% was spent on nursing home and home health care. This reflects the programme’s traditional orientation towards covering acute rather than long-term care (CMS, 2012a).

Revenue in the four different parts of Medicare

Workers in the United States and their employers are subject to a mandatory payroll tax that fully funds Part A of Medicare. Since 1990 the rates have not changed; they are 15.3% of payroll up to a “taxable maximum”, evenly split between the employer and employees. Self-employed individuals are responsible for paying the entire amount themselves. Of the 15.3%, 12.4% is earmarked for Social Security (the federal pension system) and 2.9% for Part A of Medicare. Because employees are often unaware of their employer’s contribution, they may think of the tax as being a total of 7.65%.

The system is somewhat regressive because the Social Security component of the tax applies only to the first US$ 128 400 of earned income in 2018. This is ameliorated somewhat, however, because since 1994 there has been no taxable maximum on the Medicare component. The ACA increased the overall progressivity of the tax system by raising the Medicare tax by 0.9% for individuals earning more than US$ 200 000, and married couples earning more than US$ 250 000. In addition, it imposes an additional 3.8% tax on unearned (mainly, investment) income for these wealthier Americans, although this is not earmarked for Medicare.

Part B is funded by two sources. Premiums, which are paid monthly by beneficiaries as deductions from their Social Security cheques, cover 25% of total revenue. The remaining amount is paid by general federal revenues. In 2018 the premium for most beneficiaries was US$ 134 per month. Those with incomes above US$ 85 000 (individual) or US$ 170 000 (family) pay more on a sliding scale.

The Supplementary Medicare Insurance (Part B) Trust Fund’s adequacy is not of great significance because each year, Part B premiums and general revenues are re-set so as to meet projected expenses. In contrast, with regard to the Hospital Insurance (Part A) Trust Fund, each year the Board of Trustees reports on the solvency of the Fund, going 75 years into the future. In their 2017 report the Trustees indicated that the Trust Fund was projected to be depleted in 2029. Nevertheless, the report noted that the future solvency of the Trust Fund will depend heavily on how successful Medicare is in controlling future expenditures (Boards of Trustees, 2017), calling on the government to “address Medicare’s remaining financial challenges”, preferably “in the near future” (p. 9). It should be recognized, however, that even if the Trust Fund becomes depleted, the amount of the deficit will be relatively small in the short run, giving Congress time to adjust benefits downwards or revenue upwards. Moreover, the projects only apply to Part A of Medicare. Parts B (physician) and Part D (prescription drugs) are covered by general federal revenues and individual premiums, and thus are not subject to solvency concerns (van de Water, 2018).

The funding sources for Part C are the same as noted earlier for Parts A and B. Some companies charge a premium in addition to the Part B premium, but others do not. On average, in 2017 the monthly premium for Part C plans covering prescription drugs was US$ 36, in addition to the Part B premium (the latter of which is usually required for Part C coverage; Kaiser Family Foundation, 2017d).

Similar to Part B, Part D is subsidized through general federal revenues, which pay for 74.5% of programme costs. Most of the remainder of the funding comes from beneficiary premiums. The federal government also contributes towards the premiums and cost-sharing requirements of low-income Medicare beneficiaries. While there is not a Trust Fund per se for Part D, there is a “Part D account” that is under the purview of the Board of Trustees.

Pooling of funds and risk in Medicare

In Medicare there are separate Trust Funds for Parts A and B to pool revenue. In considering the Trust Funds, it is necessary to understand that Medicare, in the same way as Social Security pensions, is funded on a “pay-as-you-go” basis – which is typical in social insurance programmes worldwide. That is, contributions made by workers and their employers are not earmarked for the workers themselves but instead are used to pay for the expenses associated with current retirees. It is, in essence, an intergenerational transfer. Technically, though, all contributions are directed to the trust funds and all payments are made from the trust funds.

Medicare Part A funds are pooled into the Hospital Insurance Trust Fund from the 2.9% mandatory payroll tax paid by employers and employees (1.45% each). These funds pay for hospital services for all Medicare enrollees. Part B and D funds are pooled at the level of general federal revenues in the Supplementary Medical Trust Fund programme. For Medicare Advantage (Part C), financial resources flow from the government, which is the principal collection agency, to private insurance companies that sell insurance and pool funds. Payment to Part C plans from the government is capitated and risk-adjusted based on beneficiaries’ health conditions, dual-eligible (Medicaid) status, disability eligibility status and institutional status. Pooling for Part D is similar to Part C in that general revenue funds are paid to private health plans on a capitated risk-adjusted basis.

Purchasing and purchaser–provider relations

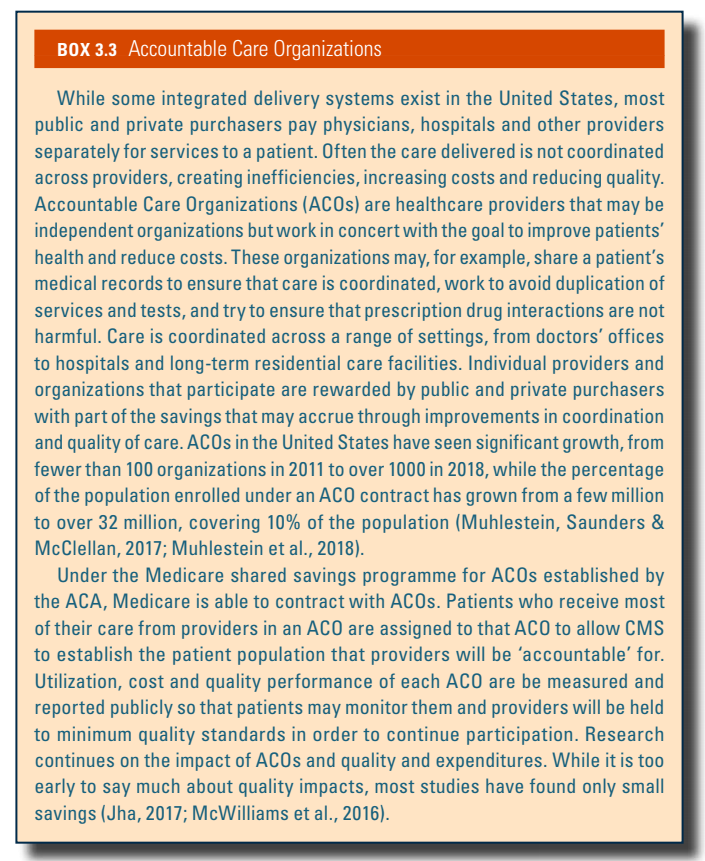

The role of purchasing and purchaser–provider relations in Medicare depend on whether a Medicare beneficiary belongs to the traditional (FFS) Medicare system or is in a Medicare Advantage plan, most of which rely on managed care. Since the passage of the ACA, the CMS has also begun contracting with teams of providers to coordinate care in the hope of improving quality and reducing costs. These groups are called ACOs and are discussed further in Box3.3.

Box3.3

Traditional Medicare

An unusual aspect of the physician payment system regards the “assignment” of services. Physicians can choose to accept assignment for all services, or alternatively to do so on a selective basis. For assigned services, Medicare pays its share (generally, 80% of the Medicare fee after the patient meets a small annual deductible) directly to the physician, which removes the risk of default on most of the bill. In return, the physician agrees to accept the Medicare fee schedule amount as payment in full for the service. For non-assigned services, Medicare pays its share directly to the patient, and as a result the physician needs to collect their entire bill from the patient. The advantage to the physician is that they are allowed to bill the patient up to 9.25% (15% of 95% of the Medicare fee schedule) more than the amount for the service as specified by the Medicare fee schedule.

Medicare has made it advantageous to physicians to become “participating providers”, in which they agree to accept all services on assignment. Incentives to do so include 5% more in reimbursement from Medicare, being listed in a national directory of participating physicians and faster claims payments. In response to these incentives, over time, assignment rates have risen from 50% from the mid-1960s to the 1980s to almost 100%, mainly because almost all physicians have chosen to become participating physicians (MedPAC, 2011, 2016).

Medicare Advantage

Under Medicare Advantage (Part C) and Part D, the Medicare programme contracts with insurers and managed care companies to provide benefits to programme beneficiaries. For Part C, the CMS contracts with health plans to provide managed health care coverage for all Part A and Part B services, as well as other services not generally covered by traditional Medicare. Rates are not negotiated between the government and Medicare Advantage plans. Rather, the plans provide bids for counties that they wish to serve. The federal government establishes a “benchmark” that is a dollar amount. It is based on a number of factors including the cost of providing services under traditional Medicare in a specific county. For bids over the benchmark,[6] enrollees pay the difference in premiums. If the bid is lower than the benchmark, this amount is split between the plan and Medicare. The plan can either provide rebates to enrollees or, more commonly, enhance benefits. Part C plans are required by the CMS to provide additional services in an amount equal to any excess remaining in their plans for the contract year and to return any remaining funds to the Medicare Trust Fund.

- 5. Medicare’s benefit structure is based on a “benefit period”, which begins with a hospitalization and ends after 60 days have elapsed from discharge from a hospital or nursing home. The benefits mentioned in the text apply to each benefit period, with the exception of the 60 lifetime-reserve days, which can be used only once and are subject to the same substantial daily co-payments discussed above. ↰

- 6. For a discussion of how the benchmark is set and policy issues surrounding it, see Health Affairs (2011). ↰

For coverage starting in January 2024, enrollment in the Affordable Care Act Marketplace reached a new record of 21 million enrollees. Part of this Marketplace enrollment growth stems from the April 2023 expiration of a COVID-era policy that maintained Medicaid enrollee eligibility, leaving millions of previous Medicaid enrollees looking for publicly subsidized Marketplace coverage. Other reasons for continued Marketplace enrollment growth included increased subsidies reported on previously, as well as increased funding for navigator programs to help consumers shop for plans.

Despite the Medicaid disenrollment beginning in April 2023, Medicaid coverage has increased since the pandemic began (88 million as of September 2023 compared to 71 million in February 2020). Coverage in publicly sponsored (Medicaid) or subsidized (Marketplace) plans combined has also reached a new record of 105 million individuals. One in three Americans are covered by Medicaid or ACA-related coverage expansions in the 10th year after these health reforms were implemented.

Authors

References

3.3.2. Medicaid

Unlike Medicare, which is available to nearly all individuals aged 65 and older, Medicaid is a means-tested programme. It is designed to provide health insurance for those with the lowest income levels and fewest assets, the disabled, and to poor seniors with Medicare coverage, as well as the disabled and seniors who have exhausted their financial resources, often as a result of very high long-term care expenses. Medicaid is a key resource for some of the poorest and sickest Americans.

Medicaid programmes are state-based but they are funded jointly by the states and the federal government. In return for federal dollars, states are required to meet certain federal government standards. Participation by the states is voluntary, though historically all the states have chosen to participate. Services are largely purchased from the private sector. This section of the chapter also includes information about CHIP, a coverage programme for children in families whose incomes exceed Medicaid eligibility limits but who do not have private coverage.

Coverage[7]

Breadth of coverage

Medicaid covers several distinct population groups. The breadth of coverage varies across states according to these population groups.

The main groups covered by Medicaid are:

- low-income children

- low-income pregnant women

- low-income disabled persons

- low-income senior citizens

- low-income parents of dependent children.

For adults, in some states that have not chosen to expand eligibility under the ACA (described below), not only are there income restrictions but also asset limitations that can preclude eligibility. Even more significantly, in those states Medicaid does not generally provide coverage to low-income adults who do not care for dependent children.

Even before the ACA, Medicaid eligibility requirements had been liberalized over the years. Originally, to be eligible for Medicaid, it was necessary to also be receiving cash assistance payments (often connoted as “welfare”). This is no longer true as states have expanded eligibility to other groups and those with higher incomes, taking advantage of the federal government matching funds to provide further assistance to their residents.

Compared to Medicare, Medicaid covers roughly 15 million more Americans (a total of 74 million), including 55% of Americans with incomes below the poverty level (Kaiser Family Foundation, 2017e). As noted, the breadth of coverage varies considerably by eligibility group. Children and pregnant women have the most liberal eligibility requirements. States are required to cover pregnant women and children up to the age of 6 if their incomes are at or below 138% of the federal poverty level (FPL), and children aged 6–18 up to 100% of the FPL. (In 2018 the federal poverty level was US$ 12 140 for a single individual and US$ 25 100 for a family of four.) Many states employ even higher thresholds. When combined with CHIP coverage, the typical state provides coverage to children aged 0–5 up to 216% of the FPL, children aged 6–18 to 155%, and pregnant women up to 258%. Thus, coverage of pregnant women and children is quite broad. To illustrate the critical role that Medicaid plays for pregnant women, the programme pays for half of all births in the United States (Kaiser Family Foundation, 2017f).

Coverage is somewhat narrower for seniors and the disabled, however, with the typical state providing coverage up to 73% of the FPL (Kaiser Family Foundation, 2017g). It should be considered, however, that most of these people have Medicare coverage as well, so Medicaid is providing them with supplementary insurance that covers Medicare’s co-payments and some uncovered services, especially long-term care. Nevertheless, lower-income Medicare beneficiaries who are not eligible for Medicaid coverage usually do not have access to other forms of supplemental insurance coverage, and therefore are at financial risk associated with Medicare’s co-payments as well as services not covered by the programme.

With respect to one particular disabled population of note – those with HIV or AIDS – Medicaid provided coverage for 42% of this population in 2014 (Kates & Dawson, 2017). To be eligible, one must not only be disabled through HIV/AIDS, but also have an income that is low enough to qualify. Of particular importance is the programme’s coverage of antiretroviral drugs. However, despite Medicaid coverage for this vulnerable population, HIV/AIDS care constitutes only about 1.5% of the total programme expenditures (Kaiser Family Foundation, 2013).

Low-income parents of dependent children face the most stringent eligibility requirements if they are among the states that did not expand Medicaid eligibility. Most notable is Texas, where coverage is provided only to those with incomes up to 18% of the FPL (that is, an annual income even as low as US$ 4000 would disqualify the parent of a family of three from coverage in that state). Most states provide coverage up to 138% of the FPL since that is a requirement of the voluntary Medicaid expansions. This illustrates the large variation in breadth of coverage that currently exists between states.

Implementation of the Medicaid expansions, resulting from the ACA, dramatically increased the breadth of coverage for the poor and near-poor under the age of 65 in most states. Beginning in 2014, states that chose to expand their Medicaid coverage received 100% of the costs of coverage for new enrollees up to 138% of the FPL from the federal government.[8] The federal contribution gradually decreases to 90% of state costs after three years. For states that choose to expand Medicaid coverage, no categorical restrictions are allowed – for example, poor and near-poor adults without children are eligible. Finally, there are no restrictions on the possession of assets. One important caveat applies to the information provided above. Medicaid does not cover undocumented residents, nor are states required to cover legal residents during their first five years in the United States. Currently, the federal government will provide matching funds to make Medicaid coverage available to pregnant women and children who are legal immigrants with fewer than five years of residency. As of 2016, about half of states had done so (Kaiser Family Foundation, 2017h).

Scope of coverage

The scope of coverage under Medicaid is generally wide but varies by state. Federal law requires that states provide the following services (this is only a partial list of the more significant ones): inpatient and outpatient hospital, physician, nurse practitioner (NP), laboratory and radiology, nursing home and home health care for those aged 21 and older, health screening for those under age 21, family planning and transportation.

Other services are optional for states. This designation means that if a state chooses to cover the service, it will receive matching funds from the federal government. Optional services include some major services such as prescription drugs and dental care, but also such things as care provided by professionals besides physicians and NPs, durable medical equipment, glasses, rehabilitation, various types of institutional care, home and community-based services, personal care services and hospice care.

While technically “optional”, many of these services are covered to some extent by the states. All states, for example, provide some prescription drug coverage. Many states limit the number or type of services, as discussed below. It is estimated that for populations that states are required to cover under Medicaid, 31% of Medicaid spending is for these optional services (MACPAC, 2017b).

Depth of coverage

It is difficult to summarize Medicaid’s depth of coverage, except to say that like most aspects of the programme, it varies considerably by state and by population group. While a few states impose nominal co-payments under federally approved waivers, they are, as yet, generally not very significant. In contrast, coverage is often not deep in three meaningful ways: (1) some states have been given waivers by the federal government to impose premiums and non-trivial cost-sharing requirements on some Medicaid beneficiaries, and in a few recent cases, require evidence of working; (2) states often put restrictions on the number of services and/or types that are covered; and (3) access to private practising physicians is often limited, meaning that enrollees may have to seek care from public facilities or clinics. Waivers allowing imposition of work requirements are the focus of active litigation in several states (NASHP, 2020).

It was noted earlier that there are a number of mandatory services covered by Medicaid, including inpatient and outpatient hospital and physician care, home health services, laboratory and X-ray services, to name a few (a full list of required services is available on Medicaid’s website). States are, however, allowed to set limits to the number of such services provided, for both mandatory and optional services – a marked difference between Medicare and most private insurance policies provided through employment. These can significantly reduce the depth of coverage under the programme. In 2012, for example, many states had instituted visit co-payments, typically between US$ 1 and US$ 4, and a number also limit the number of prescriptions that can be filled; a typical limit is 4–6 per month depending on the state (Kaiser Family Foundation, 2012a).

Finally, because Medicaid provider payments are low compared to other insurance, access to care in physicians’ offices has been problematic, a situation that has existed since the programme’s inception. (Provider payment is discussed in more detail in section 3.7.) In 2016 Medicaid physician fees, on average, were only 72% as high as Medicare’s for all services, and 66% as high for primary care services (Kaiser Family Foundation, 2016). Medicare fees, in turn, tend to be lower than those paid by private insurers. Low physician payment rates put patients with Medicaid at a distinct disadvantage in obtaining care from privately practising office-based physicians – meaning they sometimes need to go to outpatient clinics or even the emergency room to obtain needed care. A 2011 national physician survey found that 31% of physicians said they would not accept any new Medicaid patients (Decker, 2012). One development with the potential to provide more mainstream access to physician office care is the movement towards the use of managed care in the Medicaid programme. About 75% of Medicaid beneficiaries are in managed care plans (CMS, 2016a). While the exact nature of these arrangements varies both between and within states, they may include capitation (rather than FFS) for providers and/or primary care case management. An important development is the use of managed care not only for pregnant women and children, but also for those with chronic diseases and those who are jointly covered by Medicare and Medicaid. States often prefer managed care as a means of both enhancing quality and controlling costs. It is critical, however, that capitation rates paid to managed care organizations be sufficient to provide high-quality care with access to physician offices (Kaiser Family Foundation, 2010).

Revenue collection

Medicaid is financed jointly between the federal and state governments. In general, both finance their shares from general revenues – mainly taxes. Unlike Parts A and B of Medicare, there is no trust fund dedicated to the programme’s financing.

In 2016 total Medicaid expenditures were US$ 565 billion – 85% of the US$ 672 billion spent on Medicare and 17% of total health expenditures in the United States. Medicaid constitutes almost 10% of the federal government budget and 16% of state spending. The only state budget component with a larger share is elementary and secondary education, which constitutes roughly 24% of total state spending (CMS, 2018b; MACPAC, 2017c).

About 60% of total Medicaid spending is devoted to acute care, and 40% to long-term care (MACPAC, 2017a). Of note is the fact that while only about one quarter of enrollees are senior citizens or the disabled, they account for over 60% of programme spending. In fact, average spending for a disabled enrollee (US$ 16 859 in 2014) or a senior (US$ 13 063) exceeded spending for children (US$ 2577) and non-elderly adults (US$ 3278) by about five-fold (Kaiser Family Foundation, 2014).

Pooling of funds and risk in Medicaid

Some of the more general issues surrounding the pooling of funds in the US health care system are discussed in section 3.2.2. Currently, the main pooling activity that occurs in Medicaid is through the Federal Medical Assistance Percentage (FMAP) formula, which allots a greater proportion of federal government dollars to states with lower per capita incomes.

The formula by which states’ respective shares of federal Medicaid monies are divided up is called the FMAP. The following formulas are used:

- federal share: 1–0.45 x (state per capita income/US per capita income)

- state share: 0.45 x (state per capita income/US per capita income).

Thus, states where per capita income is at the national average will receive 55%. By law, no state pays more than 50%, with the poorest state receiving about 76%. On average, the federal government share is 57%. It is important to note that this formula does not apply to states that have taken advantage of the ACA’s Medicaid expansion. After a three-year transition period, the federal government pays 90% of costs for all such new Medicaid beneficiaries, regardless of state per capita income.

The above formula is applicable to most Medicaid expenditures for medical services. Some services, and administrative costs, are determined by separate laws. Administrative costs, for example, are split 50/50 between the federal and state government irrespective of the state’s per capita income.

A perennial issue surrounding the FMAP formula is that it does not respond to the counter-cyclical nature of Medicaid. When there is an economic downturn, state revenues fall. This is problematic for states in several ways.

- Since the formula is in part based on national income, if all states have declining per capita income during a recession, they will not, on average, receive higher federal government contributions.

- During such an economic downturn, unemployment rises, which means Medicaid eligibility (and therefore costs) also rises.

- The formula is based on past rather than current per capita income. For example, the 2018 FMAP was based on incomes during 2013, 2014 and 2015 (Mitchell, 2018).

- 7. Unless otherwise noted, factual information in this section was obtained from Kaiser Family Foundation (2013b). ↰

- 8. Just after the November 2018 elections 36 states and the District of Columbia had adopted Medicaid expansion, although a small handful are in the process of implementing it. Fourteen states had not done so, including four of the nine states with the highest population: Texas, Florida, Georgia and North Carolina. Medicaid expansion in Utah and Idaho, both Republican states, has proved more controversial than expected with ballot measures defying political leadership to squash such plans (Pear, 2019). ↰

Budget legislation signed by President Trump in July 2025, combined with Congress’s decision not to extend “enhanced” premium subsidies in the Affordable Care Act (ACA) marketplaces, is predicted to increase the number of uninsured Americans by 16 million by the year 2034, according to the Congressional Budget Office (CBO) [1,2]. In 2024, it was estimated that there were 27.2 million uninsured Americans, well below the 49 million in 2010, prior to the implementation of the ACA [3, 4].

The new legislation, named the “One Big Beautiful Bill” (OBBB) Act, was intended to extend Trump’s tax legislation from his first term, which otherwise was about to expire. This required generating trillions of dollars in savings from government programs. Below, we discuss the major reasons that the number of uninsured Americans is expected to rise so much.

Medicaid work verification requirements

The CBO estimates the largest share of Medicaid savings ($326 billion over 10 years) to come from changing Medicaid expansion eligibility by implementing work requirements [5]. Prior to the OBBB, federal law prohibited linking Medicaid eligibility to working or looking for work. However, states could obtain waivers from the federal government to implement work requirements. These demonstration waivers were approved in several states during the first Trump administration, though later rescinded by the Biden administration. Georgia is currently the only state with an approved work requirement waiver, though more than a dozen have applied for waivers to implement them [6].

Under the OBBB, working-age individuals enrolled in or applying for Medicaid expansion in any state would be required to verify they are working or participating in qualifying activities (e.g., looking for work, job training) at least 80 hours per month. Parents of dependent children age 13 or younger or individuals who are medically frail are exempted from work requirements [7] (effective 31 December 2026, although the Secretary of Health and Human Services can extend this deadline by two years for states acting in good faith to implement the requirements).

Already, 64% of working-age individuals enrolled in Medicaid, who are not covered by disability insurance, report working part or full time [8]. Evidence from Arkansas’s attempt to implement a work requirement waiver in 2018 resulted in 25% (18,000) of those eligible for the work requirement losing Medicaid coverage, an increase in the uninsurance rate in the state, with no change in unemployment rates. Many people lost Medicaid because they had trouble reporting and verifying their work or other qualifying activities. Of the 13 states that had approved or in-progress demonstrations to implement work requirements during the first Trump administration, Michigan Medicaid was estimated to lose 100,000 otherwise eligible individuals due to work requirements, prior to a judge blocking implementation [10]. The CBO estimates that 18.5 million people will be subject to work requirements each year, and in 10 years, 5.2 million fewer adults will be enrolled in Medicaid. Few of these are expected to find other coverage, given provisions in the OBBB that those who are not eligible for Medicaid due to work requirements are also ineligible for marketplace subsidies, thus increasing the number of those without insurance by a further 4.8 million [11].

In addition to work requirements, the OBBB requires states to redetermine eligibility at least every 6 months instead of annually (effective 2026, resulting in a budget reduction of $63 billion over 10 years [12]). Further, retroactive coverage is limited to 1 month for expansion enrollees, a decrease from 3 months of retroactive coverage in federal law prior to the OBBB.

Other Medicaid changes

Changes to financing Medicaid expansion enacted through the OBBB include the elimination of temporary incentives (+5% to the federal matching rate for 2 years) for the 12 states that have not already expanded Medicaid, essentially disincentivizing those who have not expanded already to now do so (effective 1 January 2026) [13]. The OBBB will also limit federal matching for providing emergency services to individuals who would otherwise be eligible for Medicaid expansion but for their immigration status (effective 1 October 2026). Regarding premiums and out-of-pocket payments, the OBBB eliminates optional enrollment fees and premiums but requires states to charge up to $35 in cost-sharing for the expansion population. However, many services (e.g., primary care, mental health, substance use services) and providers (e.g., rural health clinics, federally qualified health centres) are exempt from cost sharing (effective 1 October 2028 [7] and expected to reduce the federal budget by $7 billion over 10 years).

Provider taxes that currently help finance Medicaid in many states will also be affected by the OBBB. Specifically, states that have expanded Medicaid will have the provider tax limit, referred to as the safe harbour limit, reduced from 6% to 3.5%. This policy is expected to decrease provider tax revenue for the state Medicaid program in 22 expansion states, mostly through taxes to hospitals on their net patient revenues [14]. These changes to provider taxes will begin in 2028 with 0.5% reductions occurring in expansion states until the 3.5% limit is reached and are expected to reduce federal Medicaid spending by $191 billion over 10 years [12]. In addition to financing changes specific to Medicaid expansion, more broadly, the OBBB includes new limits to payments that state Medicaid programs can make to hospitals and nursing facilities via Medicaid managed care programs, affecting provider payments in approximately 30 states [14] (effective upon enactment, expected to reduce the budget by $149 billion over 10 years).

Changes to marketplaces

While the original premium subsidies that went into effect in 2014 resulted in millions of Americans obtaining health insurance coverage, many were still unable to afford the premiums. One reason is that they were available only to those whose incomes were no more than four times the federal poverty level (currently, $15,650 for an individual and $32,150 for a family of four). Another consideration was that premiums could vary by a factor of three depending on age, resulting in older prospective purchasers frequently facing premiums that represented a significant portion of their income. In 2021, legislation passed under the Biden Administration expanded premium subsidies so that no one would pay more than 8.5% of their income for a so-called “benchmark plan.” Coverage became more affordable, particularly for people close to retirement. These enhanced subsidies will end after 2025, as Congress did not extend them under the OBBB. As a result, on average, policyholders will face more than a 75% increase in their out-of-pocket premiums [15, 2].

As noted, CBO predicts an increase of 16 million uninsured persons by 2034. An estimated 4.2 million will be the result of the expiration of the enhanced premiums. Another 0.9 million will be due to other changes made to the marketplaces. One of the most significant ones is the shortening of the open enrollment period from 2.5 months to 1.5 months.

Impacts on access to healthcare and health

OBBB provisions will lower access to healthcare in several ways. The drop in insured people due to Medicaid and ACA cuts will reduce patients’ ability to obtain healthcare. In addition, reductions in the number of insured will lead to financial distress for healthcare providers such as physicians and hospitals. This will result in a reduction in services and the closing of hospitals, further reducing access to care for many Americans [16]. Rural clinics and hospitals, which see a higher proportion of Medicaid patients, will be heavily affected.

Access to care will also be affected by limitations on the amount of federal loan money medical students can obtain [17], making it more difficult for students to finance medical school. This may discourage students from entering medical school, thereby exacerbating an existing physician shortage. Rural areas will be especially hard hit as they will need to pay physicians more for them to pay off their medical school debts.

The health impacts of the bill have been estimated. The estimates are based on drafts of the bill by the House or Senate and vary based on the estimated loss of insurance and services arising from the bills. Gaffney and colleagues estimate that, due to the loss of Medicaid and ACA insurance, the proposed House version of the bill would increase deaths by between 8,200 and 24,600 annually, with a mid-range of 16,642 [18]. The Leonard Davis Institute (LDI) at the University of Pennsylvania and the Center for Disease Modeling and Analysis at Yale University predict a total of 42,500 additional deaths annually from the bill’s changes: 11,300 due to people losing coverage from loss of Medicaid or ACA; 18,200 from low-income Medicare beneficiaries losing Medicaid prescription drug subsidies, and 13,000 from low staffing in nursing homes [19]. The LDI estimates that the impact of the loss of access to treatment for opioid use disorder will result in a doubling of the overdose rate, increasing the rate of fatal overdoses by approximately 1,000 each year [20]. The LDI also estimates that the projected loss of Supplemental Nutrition Assistance Program (SNAP) benefits by 3.2 million Americans will result in 93,000 premature deaths by 2029.

As of yet, there are no estimates of the impacts on health inequities, but it is evident that the insurance losses from this bill will be felt by lower-income and disadvantaged persons who rely on Medicaid and the ACA marketplace. The same can be said of the reductions in SNAP.

References

[1] Basu SY, Patel S, Berkowitz SA. Projected Health System and Economic Impacts of 2025 Medicaid Policy Proposals [Internet]. JAMA Health Forum. 2025 Jul 3;6(7):e253187 [cited 5 August 2025]. Available from: https://jamanetwork.com/journals/jama-health‑forum/fullarticle/2836460

[2] Congressional Budget Office. Letter to the Honorable Ron Wyden, Frank Pallone, Jr., and Richard E. Neal: Estimated effects on the number of uninsured people in 2034 resulting from policies incorporated within CBO’s baseline projections and H.R. 1 [Internet]. Washington, DC: CBO; 4 June 2025 [cited 5 August 2025]. Available from: https://www.cbo.gov/system/files/2025-06/Wyden-Pallone-Neal_Letter_6-4-25.pdf

[3] National Center for Health Statistics. U.S. uninsured rate drops 15% since 2020 [Internet]. Washington, DC: NCHS; 24 June 2025 [cited 5 August 2025]. Available from: https://www.cdc.gov/nchs/pressroom/releases/20250624.html

[4] Statista. Americans without health insurance [Internet]. Statista; [cited 5 August 2025]. Available from: https://www.statista.com/statistics/200955/americans-without-health-insurance

[5] Congressional Budget Office. Estimated budgetary effects of H.R. 1, the One Big Beautiful Bill Act [Internet]. Washington, DC: CBO; 4 June 2025 [cited 5 August 2025]. Available from: https://www.cbo.gov/publication/61461

[6] Kaiser Family Foundation. Section 1115 Waiver Tracker: Work Requirements [Internet]. San Francisco: KFF; 2025 Aug 1 [cited 5 August 2025]. Available from: https://www.kff.org/report-section/section-1115-waiver-tracker-work-requirements

[7] Kaiser Family Foundation. Tracking the Medicaid Provisions in the 2025 Budget Bill [Internet]. San Francisco: KFF; 8 July 2025 [cited 5 August 2025]. Available from: https://www.kff.org/tracking-the-medicaid-provisions-in-the-2025-budget-bill

[8] Hinton E, Rudowitz R. 5 Key Facts About Medicaid Work Requirements [Internet]. San Francisco: Kaiser Family Foundation; 18 February 2025 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/5-key-facts-about-medicaid-work-requirements

[9] Basu S, Patel S, Berkowitz SA. Projected Health System and Economic Impacts of 2025 Medicaid Policy Proposals. N Engl J Med. 13 June 2019;380(24):2287–96. doi: 10.1056/NEJMsr1901772.

[10] Gordon R. More Than 100,000 Michigan Residents Nearly Lost Medicaid Coverage under Work Requirements [Internet]. New York: The Commonwealth Fund; 12 May 2025 [cited 5 August 2025]. Available from: https://www.commonwealthfund.org/blog/2025/michigan-residents-nearly-lost-medicaid-coverage

[11] Hinton E, Diana A, Rudowitz R. A Closer Look at the Work Requirement Provisions in the 2025 Federal Budget Reconciliation Law [Internet]. San Francisco: Kaiser Family Foundation; 30 July 2025 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/a-closer-look-at-the-work-requirement-provisions-in-the-2025-federal-budget-reconciliation-law

[12] Kaiser Family Foundation. Health Provisions in the 2025 Federal Budget Reconciliation Law: Medicaid [Internet]. San Francisco: KFF; 4 August 2025 [cited 5 August 2025]. Available from: https://www.kff.org/report-section/health-provisions-in-the-2025-federal-budget-reconciliation-law-medicaid

[13] Rudowitz R, Corallo B, Garfield R. New Incentive for States to Adopt the ACA Medicaid Expansion: Implications for State Spending [Internet]. San Francisco: Kaiser Family Foundation; 17 March 2021 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/new-incentive-for-states-to-adopt-the-aca-medicaid-expansion-implications-for-state-spending

[14] Hulver S, Burns A, Mathers J. Reconciliation language could lead to cuts in Medicaid state-directed payments to hospitals and nursing facilities [Internet]. San Francisco: Kaiser Family Foundation; 27 June 2025 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/reconciliation-language-could-lead-to-cuts-in-medicaid-state-directed-payments-to-hospitals-and-nursing-facilities

[15] Ortaliza J, McGough M, Cox C, Pestaina K, Rudowitz R, Burns A. How Will the One Big Beautiful Bill Act Affect the ACA, Medicaid, and the Uninsured Rate? [Internet]. San Francisco: Kaiser Family Foundation; 18 June 2025 [cited 5 August 2025]. Available from: https://www.kff.org/policy-watch/how-will-the-2025-budget-reconciliation-affect-the-aca-medicaid-and-the-uninsured-rate

[16] Liptak K, Holmes K. Inside Trump’s last 24 hours as he willed his agenda bill over the finish line. CNN [Internet]. 3 July 2025 [cited 5 August 2025]. Available from: https://amp.cnn.com/cnn/2025/07/03/politics/how-trump-passed-agenda-bill

[17] Liptak K, Holmes K. How the Passage of the “Big, Beautiful Bill” Could Impact Med Students and Hospitals. U.S. News & World Report [Internet]. 18 July 2025 [cited 5 August 2025]. Available from: https://www.usnews.com/news/national-news/articles/2025-07-18/how-the-passage-of-the-big-beautiful-bill-could-impact-med-students-and-hospitals

[18] Smith J, Johnson A, Lee R. Projected Effects of Proposed Cuts in Federal Medicaid Funding on Health Outcomes. Ann Intern Med. 15 July 2025;25(7):716–723. doi: 10.7326/ANNALS-25-00716.

[19] Werner RM, Coe NB, Roberts ET, Galvani AP, Pandey A, Ye Y. Projected Mortality Impacts of House-Passed Budget Reconciliation Bill Provisions [Internet]. Washington, DC: U.S. Senate; 3 June 2025 [cited 5 August 2025]. Available from: https://www.sanders.senate.gov/wp-content/uploads/LDI-Yale-Letter-Final-1.pdf

[20] Leonard Davis Institute Staff. Estimated Overdose Deaths Due to the Loss of MOUD in the One Big Beautiful Bill Act [Internet]. Philadelphia: University of Pennsylvania; 2 July 2025 [cited 5 August 2025]. Available from: https://ldi.upenn.edu/our-work/research-updates/estimated-overdose-deaths-due-to-the-loss-of-moud-in-the-one-big-beautiful-bill-act

Rural healthcare is likely to be severely affected by provisions in President Donald Trump’s “One Big Beautiful Bill” Act, which was signed into law on 4 July 2025. Cuts to Medicaid will disproportionately affect rural areas as a higher proportion of rural residents are Medicaid recipients. In addition, cuts to provider taxes, which help finance the state’s share of Medicaid, will reduce financial support to rural providers and facilities (McKinley, 2025). Cuts to state-directed payment programmes could further reduce provider payments. If reductions in the number of insured patients and lower provider payments lead to financial distress for healthcare providers, it would result in reduced service availability and hospitals closing, further lowering access to care for rural residents (Egan & Luhby, 2025).

As part of the bill, Congress provisioned USD 50 billion for a “Rural Health Transformation Program”, intended to offset the effects of Medicaid cuts on rural communities. States that provide a plan for “rural health transformation” will receive funding from a pot of USD 10 billion per year from 2026 through 2030 (Hohman, 2025). Many believe that these funds will be insufficient to cover the losses from other provisions in the bill (McKinley, 2025). The National Association of Rural Health Clinics states that it is unclear if facilities will receive a portion of the funding (Hohman, 2025).

Authors

References

Egan, M & Luhby, T. (2025). Here’s who stands to gain from the “big, beautiful bill”. And who may struggle. CNN, 4 July 2025. https://www.cnn.com/2025/07/03/business/trump-big-beautiful-bill-business-economy

Hohman, S. (2025). What Trump's “One Big Beautiful Bill” Means for Rural Health Clinics. National Association of Rural Health Clinics, 7 August 2025. https://www.narhc.org/News/31439/What-Trumps-One-Big-Beautiful-Bill-Means-for-Rural-Health-Clinics

McKinley Abel, A. (2025). NRHA Statement on Senate Passing the One Big Beautiful Bill Act. National Rural Health Association, 1 July 2025. https://www.ruralhealth.us/blogs/2025/07/nrha-statement-on-senate-s-one-big-beautiful-bill-act

Authors

References

Dietz M, et al. 2023. “California’s Uninsured in 2024: Medi-Cal Expands to All Low-Income Adults, but Half a Million Undocumented Californians Lack Affordable Coverage Options.” UC Berkeley Labor Center. https://laborcenter.berkeley.edu/californias-uninsured-in-2024

Kaiser Family Foundation. 2023. Key Facts on Health Coverage of Immigrants. https://www.kff.org/racial-equity-and-health-policy/fact-sheet/key-facts-on-health-coverage-of-immigrants

Medicaid is a means-tested public insurance program for the poor and disabled in the US. It is jointly administered by the states and federal government, and covers eligible children, parents, pregnant women, and seniors in poverty and people with disabilities. Exact eligibility varies from state to state. One drawback to Medicaid is that people “churn” in and out of it if their income changes or if they haven’t provided the information needed to verify their income or residency (Weixel, 2023).

During COVID-19, access to Medicaid was expanded by requiring states to maintain continuous coverage of anyone enrolled on or after 18 March 2020 (Cubanski et al., 2023). In return, states received a 6.2% increase in their federal matching rate. State programs could not implement more restrictive eligibility standards or increase premiums.

By preventing states from disenrolling people from coverage during the pandemic, the continuous enrollment provision preserved coverage for many and expanded access to healthcare. Total Medicaid enrollment increased 32% from February 2020 to November 2022 (Corallo and Moreno, 2023). Although states increased Medicaid spending as a result of the provisions, the enhanced federal funding is estimated to have exceeded the higher state costs (Corallo and Moreno, 2023).

The continuous Medicaid enrollment features of the COVID emergency measures ended on 31 March 2023, and the enhanced federal funding of states was phased out through 31 December 2023 (Cubanski, 2023). With the lifting of continuous enrollment, states began reviewing eligibility for Medicaid on a regular basis and are ending Medicaid coverage for anyone that they determined is no longer eligible or who did not provide proper documentation (Weixel, 2023).

As of 30 January 2024, over 16 million beneficiaries have been disenrolled (KFF, 2024). Of these, 70% had their coverage terminated for procedural reasons (KFF, 2024). Around two-thirds of the “unwinding” is yet to come, so millions more could lose Medicaid in the future (Galewitz et al., 2023). Some of the disenrolled have been able to obtain employer-sponsored coverage or get insurance through an Affordable Care Act plan (Galewitz et al., 2023). However, other ineligibles do not make enough to afford an ACA plan nor does their employer provide insurance.

Procedural problems that recipients cite have led to termination include renewal forms sent to outdated addresses, miscalculated income levels, and difficult to interpret documents (Galewitz et al., 2023). Some recipients believe that their state has used the process to discourage enrollment (Galewitz et al., 2023). Some states are attempting to address these issues and have temporarily paused procedural terminations for some enrollees while they address problems in the renewal process. These issues in establishing eligibility point to common administrative and technical barriers that prevent many who are eligible from signing up or remaining enrolled.

Authors

References

Corallo, B. and Moreno, S. (2023). Analysis of Recent National Trends in Medicaid and CHIP Enrollment. https://www.kff.org/coronavirus-covid-19/issue-brief/analysis-of-recent-national-trends-in-medicaid-and-chip-enrollment

Cubanski, J., et al. (2023). What Happens When COVID-19 Emergency Declarations End? Implications for Coverage, Costs, and Access. https://www.kff.org/coronavirus-covid-19/issue-brief/what-happens-when-covid-19-emergency-declarations-end-implications-for-coverage-costs-and-access

Galewitz, P., Houghton, K., Kelman, B and Liss S. (2023). “Worse Than People Can Imagine”: Medicaid “Unwinding” Breeds Chaos in States. Kaiser Family Foundation Health News. 2 November 2023.

KFF. (2024). Medicaid Enrollment and Unwinding Tracker. Kaiser Family Foundation, 30 January 2024. https://www.kff.org/report-section/medicaid-enrollment-and-unwinding-tracker-overview

Weixel, N. (2023). Why millions of people could lose Medicaid next month 03/22/23 https://thehill.com/policy/healthcare/3911215-why-millions-of-people-could-lose-medicaid-next-month

The Inflation Reduction Act of 2022 initiated several reforms to Medicare prescription drug coverage. Two notable ones are a $2,000 annual out-of-pocket limit for Medicare-covered prescription drugs (beginning in 2025) and implementation of negotiation of Medicare drug prices (beginning in 2026). One of the earliest changes begins in 2023, when patient cost-sharing requirements for insulin are limited to $35 per month. Millions of seniors are expected to pay less for insulin after the $35 monthly cap as average monthly out-of-pocket spending on insulin was estimated at $58 in 2020, with 37% of beneficiaries paying more than $35, and 24% more than $70.

References

U.S. Department of Health and Human Services. Assistant Secretary for Planning and Evaluation. “Insulin Affordability and the Inflation Reduction Act: Medicare Beneficiary Savings by State and Demographics.” January 24, 2023. https://aspe.hhs.gov/sites/default/files/documents/bd5568fa0e8a59c2225b2e0b93d5ae5b/aspe-insulin-affordibility-datapoint.pdf

COVID-19 emergency measures are expected to end on 11 May 2023. These measures, enacted in early 2020, increased access to health care in several ways, one of which was through expanding access to Medicaid, the governmental insurance for the poor and disabled. Medicaid, jointly administered by the states and federal government, covers children, parents, pregnant women, and seniors in poverty and people with disabilities. Exact eligibility varies from state to state. One drawback to Medicaid is that people “churn” in and out of it if their income changes or if they can’t provide the information needed to verify their income or residency.

Under the 2020 emergency measures, state Medicaid programs were required to maintain continuous coverage of anyone enrolled on or after 18 March 2020. In return, they received a 6.2% increase in their federal matching rate. State programs could not implement more restrictive eligibility standards or increase premiums.

By preventing states from disenrolling people from coverage during the pandemic, the continuous enrollment provision preserved coverage for many and expanded access to health care. Total Medicaid enrollment increased 32% from February 2020 to November 2022. Although states increased Medicaid spending as a result of the provisions, the enhanced federal funding is estimated to have exceeded the higher state costs.

The continuous Medicaid enrollment features of the emergency measures ended on 31 March 2023, and the enhanced federal funding of states will be phased out through 31 December 2023. With the lifting of continuous enrollment, states will once again review eligibility for Medicaid on a regular basis and end Medicaid coverage for anyone that is no longer eligible. The time it will take states to assess everyone’s eligibility will vary, with some states planning to complete the process within a few months, others over a year.

Up to 15 million of the 85 million people currently with Medicaid could lose coverage. Some of those will be able to obtain employer-sponsored coverage or get insurance through an Affordable Care Act (ACA) plan. However, other ineligibles will not make enough to afford an ACA plan nor will their employer provide insurance. Additionally, in the chaotic process of reassessing Medicaid eligibility, nearly 7 million people could lose coverage because of administrative barriers like lost or incomplete paperwork.

Authors

References

Corallo, B. & Moreno, S. (2023). Analysis of Recent National Trends in Medicaid and CHIP Enrollment. https://www.kff.org/coronavirus-covid-19/issue-brief/analysis-of-recent-national-trends-in-medicaid-and-chip-enrollment