-

07 August 2025 | Policy Analysis

Budget legislation expected to result in 16 million more uninsured -

05 September 2024 | Policy Analysis

Oregon Further Expands Public Insurance Using Affordable Care Act’s Basic Health Program

6.1. Analysis of recent reforms

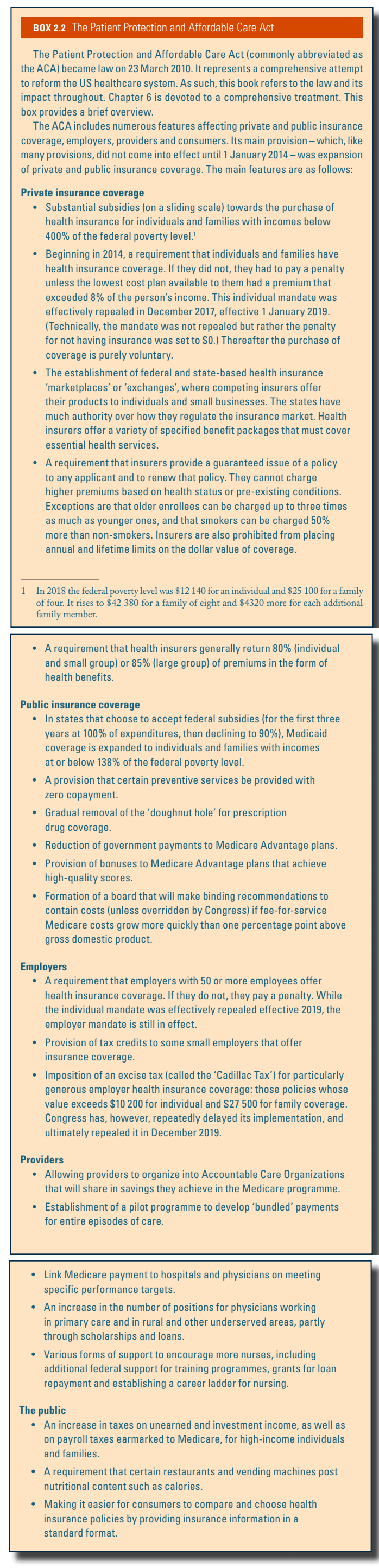

Efforts to reform the health system in the United States date back several decades. These efforts are reviewed in section 2.1 and Box2.2. In many ways the ACA represents the next step in a process that began with the passage of Medicare (public insurance mostly for the elderly) and Medicaid (public insurance for some of the poor) in 1965.

Box2.2

Budget legislation signed by President Trump in July 2025, combined with Congress’s decision not to extend “enhanced” premium subsidies in the Affordable Care Act (ACA) marketplaces, is predicted to increase the number of uninsured Americans by 16 million by the year 2034, according to the Congressional Budget Office (CBO) [1,2]. In 2024, it was estimated that there were 27.2 million uninsured Americans, well below the 49 million in 2010, prior to the implementation of the ACA [3, 4].

The new legislation, named the “One Big Beautiful Bill” (OBBB) Act, was intended to extend Trump’s tax legislation from his first term, which otherwise was about to expire. This required generating trillions of dollars in savings from government programs. Below, we discuss the major reasons that the number of uninsured Americans is expected to rise so much.

Medicaid work verification requirements

The CBO estimates the largest share of Medicaid savings ($326 billion over 10 years) to come from changing Medicaid expansion eligibility by implementing work requirements [5]. Prior to the OBBB, federal law prohibited linking Medicaid eligibility to working or looking for work. However, states could obtain waivers from the federal government to implement work requirements. These demonstration waivers were approved in several states during the first Trump administration, though later rescinded by the Biden administration. Georgia is currently the only state with an approved work requirement waiver, though more than a dozen have applied for waivers to implement them [6].

Under the OBBB, working-age individuals enrolled in or applying for Medicaid expansion in any state would be required to verify they are working or participating in qualifying activities (e.g., looking for work, job training) at least 80 hours per month. Parents of dependent children age 13 or younger or individuals who are medically frail are exempted from work requirements [7] (effective 31 December 2026, although the Secretary of Health and Human Services can extend this deadline by two years for states acting in good faith to implement the requirements).

Already, 64% of working-age individuals enrolled in Medicaid, who are not covered by disability insurance, report working part or full time [8]. Evidence from Arkansas’s attempt to implement a work requirement waiver in 2018 resulted in 25% (18,000) of those eligible for the work requirement losing Medicaid coverage, an increase in the uninsurance rate in the state, with no change in unemployment rates. Many people lost Medicaid because they had trouble reporting and verifying their work or other qualifying activities. Of the 13 states that had approved or in-progress demonstrations to implement work requirements during the first Trump administration, Michigan Medicaid was estimated to lose 100,000 otherwise eligible individuals due to work requirements, prior to a judge blocking implementation [10]. The CBO estimates that 18.5 million people will be subject to work requirements each year, and in 10 years, 5.2 million fewer adults will be enrolled in Medicaid. Few of these are expected to find other coverage, given provisions in the OBBB that those who are not eligible for Medicaid due to work requirements are also ineligible for marketplace subsidies, thus increasing the number of those without insurance by a further 4.8 million [11].

In addition to work requirements, the OBBB requires states to redetermine eligibility at least every 6 months instead of annually (effective 2026, resulting in a budget reduction of $63 billion over 10 years [12]). Further, retroactive coverage is limited to 1 month for expansion enrollees, a decrease from 3 months of retroactive coverage in federal law prior to the OBBB.

Other Medicaid changes

Changes to financing Medicaid expansion enacted through the OBBB include the elimination of temporary incentives (+5% to the federal matching rate for 2 years) for the 12 states that have not already expanded Medicaid, essentially disincentivizing those who have not expanded already to now do so (effective 1 January 2026) [13]. The OBBB will also limit federal matching for providing emergency services to individuals who would otherwise be eligible for Medicaid expansion but for their immigration status (effective 1 October 2026). Regarding premiums and out-of-pocket payments, the OBBB eliminates optional enrollment fees and premiums but requires states to charge up to $35 in cost-sharing for the expansion population. However, many services (e.g., primary care, mental health, substance use services) and providers (e.g., rural health clinics, federally qualified health centres) are exempt from cost sharing (effective 1 October 2028 [7] and expected to reduce the federal budget by $7 billion over 10 years).

Provider taxes that currently help finance Medicaid in many states will also be affected by the OBBB. Specifically, states that have expanded Medicaid will have the provider tax limit, referred to as the safe harbour limit, reduced from 6% to 3.5%. This policy is expected to decrease provider tax revenue for the state Medicaid program in 22 expansion states, mostly through taxes to hospitals on their net patient revenues [14]. These changes to provider taxes will begin in 2028 with 0.5% reductions occurring in expansion states until the 3.5% limit is reached and are expected to reduce federal Medicaid spending by $191 billion over 10 years [12]. In addition to financing changes specific to Medicaid expansion, more broadly, the OBBB includes new limits to payments that state Medicaid programs can make to hospitals and nursing facilities via Medicaid managed care programs, affecting provider payments in approximately 30 states [14] (effective upon enactment, expected to reduce the budget by $149 billion over 10 years).

Changes to marketplaces

While the original premium subsidies that went into effect in 2014 resulted in millions of Americans obtaining health insurance coverage, many were still unable to afford the premiums. One reason is that they were available only to those whose incomes were no more than four times the federal poverty level (currently, $15,650 for an individual and $32,150 for a family of four). Another consideration was that premiums could vary by a factor of three depending on age, resulting in older prospective purchasers frequently facing premiums that represented a significant portion of their income. In 2021, legislation passed under the Biden Administration expanded premium subsidies so that no one would pay more than 8.5% of their income for a so-called “benchmark plan.” Coverage became more affordable, particularly for people close to retirement. These enhanced subsidies will end after 2025, as Congress did not extend them under the OBBB. As a result, on average, policyholders will face more than a 75% increase in their out-of-pocket premiums [15, 2].

As noted, CBO predicts an increase of 16 million uninsured persons by 2034. An estimated 4.2 million will be the result of the expiration of the enhanced premiums. Another 0.9 million will be due to other changes made to the marketplaces. One of the most significant ones is the shortening of the open enrollment period from 2.5 months to 1.5 months.

Impacts on access to healthcare and health

OBBB provisions will lower access to healthcare in several ways. The drop in insured people due to Medicaid and ACA cuts will reduce patients’ ability to obtain healthcare. In addition, reductions in the number of insured will lead to financial distress for healthcare providers such as physicians and hospitals. This will result in a reduction in services and the closing of hospitals, further reducing access to care for many Americans [16]. Rural clinics and hospitals, which see a higher proportion of Medicaid patients, will be heavily affected.

Access to care will also be affected by limitations on the amount of federal loan money medical students can obtain [17], making it more difficult for students to finance medical school. This may discourage students from entering medical school, thereby exacerbating an existing physician shortage. Rural areas will be especially hard hit as they will need to pay physicians more for them to pay off their medical school debts.

The health impacts of the bill have been estimated. The estimates are based on drafts of the bill by the House or Senate and vary based on the estimated loss of insurance and services arising from the bills. Gaffney and colleagues estimate that, due to the loss of Medicaid and ACA insurance, the proposed House version of the bill would increase deaths by between 8,200 and 24,600 annually, with a mid-range of 16,642 [18]. The Leonard Davis Institute (LDI) at the University of Pennsylvania and the Center for Disease Modeling and Analysis at Yale University predict a total of 42,500 additional deaths annually from the bill’s changes: 11,300 due to people losing coverage from loss of Medicaid or ACA; 18,200 from low-income Medicare beneficiaries losing Medicaid prescription drug subsidies, and 13,000 from low staffing in nursing homes [19]. The LDI estimates that the impact of the loss of access to treatment for opioid use disorder will result in a doubling of the overdose rate, increasing the rate of fatal overdoses by approximately 1,000 each year [20]. The LDI also estimates that the projected loss of Supplemental Nutrition Assistance Program (SNAP) benefits by 3.2 million Americans will result in 93,000 premature deaths by 2029.

As of yet, there are no estimates of the impacts on health inequities, but it is evident that the insurance losses from this bill will be felt by lower-income and disadvantaged persons who rely on Medicaid and the ACA marketplace. The same can be said of the reductions in SNAP.

References

[1] Basu SY, Patel S, Berkowitz SA. Projected Health System and Economic Impacts of 2025 Medicaid Policy Proposals [Internet]. JAMA Health Forum. 2025 Jul 3;6(7):e253187 [cited 5 August 2025]. Available from: https://jamanetwork.com/journals/jama-health‑forum/fullarticle/2836460

[2] Congressional Budget Office. Letter to the Honorable Ron Wyden, Frank Pallone, Jr., and Richard E. Neal: Estimated effects on the number of uninsured people in 2034 resulting from policies incorporated within CBO’s baseline projections and H.R. 1 [Internet]. Washington, DC: CBO; 4 June 2025 [cited 5 August 2025]. Available from: https://www.cbo.gov/system/files/2025-06/Wyden-Pallone-Neal_Letter_6-4-25.pdf

[3] National Center for Health Statistics. U.S. uninsured rate drops 15% since 2020 [Internet]. Washington, DC: NCHS; 24 June 2025 [cited 5 August 2025]. Available from: https://www.cdc.gov/nchs/pressroom/releases/20250624.html

[4] Statista. Americans without health insurance [Internet]. Statista; [cited 5 August 2025]. Available from: https://www.statista.com/statistics/200955/americans-without-health-insurance

[5] Congressional Budget Office. Estimated budgetary effects of H.R. 1, the One Big Beautiful Bill Act [Internet]. Washington, DC: CBO; 4 June 2025 [cited 5 August 2025]. Available from: https://www.cbo.gov/publication/61461

[6] Kaiser Family Foundation. Section 1115 Waiver Tracker: Work Requirements [Internet]. San Francisco: KFF; 2025 Aug 1 [cited 5 August 2025]. Available from: https://www.kff.org/report-section/section-1115-waiver-tracker-work-requirements

[7] Kaiser Family Foundation. Tracking the Medicaid Provisions in the 2025 Budget Bill [Internet]. San Francisco: KFF; 8 July 2025 [cited 5 August 2025]. Available from: https://www.kff.org/tracking-the-medicaid-provisions-in-the-2025-budget-bill

[8] Hinton E, Rudowitz R. 5 Key Facts About Medicaid Work Requirements [Internet]. San Francisco: Kaiser Family Foundation; 18 February 2025 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/5-key-facts-about-medicaid-work-requirements

[9] Basu S, Patel S, Berkowitz SA. Projected Health System and Economic Impacts of 2025 Medicaid Policy Proposals. N Engl J Med. 13 June 2019;380(24):2287–96. doi: 10.1056/NEJMsr1901772.

[10] Gordon R. More Than 100,000 Michigan Residents Nearly Lost Medicaid Coverage under Work Requirements [Internet]. New York: The Commonwealth Fund; 12 May 2025 [cited 5 August 2025]. Available from: https://www.commonwealthfund.org/blog/2025/michigan-residents-nearly-lost-medicaid-coverage

[11] Hinton E, Diana A, Rudowitz R. A Closer Look at the Work Requirement Provisions in the 2025 Federal Budget Reconciliation Law [Internet]. San Francisco: Kaiser Family Foundation; 30 July 2025 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/a-closer-look-at-the-work-requirement-provisions-in-the-2025-federal-budget-reconciliation-law

[12] Kaiser Family Foundation. Health Provisions in the 2025 Federal Budget Reconciliation Law: Medicaid [Internet]. San Francisco: KFF; 4 August 2025 [cited 5 August 2025]. Available from: https://www.kff.org/report-section/health-provisions-in-the-2025-federal-budget-reconciliation-law-medicaid

[13] Rudowitz R, Corallo B, Garfield R. New Incentive for States to Adopt the ACA Medicaid Expansion: Implications for State Spending [Internet]. San Francisco: Kaiser Family Foundation; 17 March 2021 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/new-incentive-for-states-to-adopt-the-aca-medicaid-expansion-implications-for-state-spending

[14] Hulver S, Burns A, Mathers J. Reconciliation language could lead to cuts in Medicaid state-directed payments to hospitals and nursing facilities [Internet]. San Francisco: Kaiser Family Foundation; 27 June 2025 [cited 5 August 2025]. Available from: https://www.kff.org/medicaid/issue-brief/reconciliation-language-could-lead-to-cuts-in-medicaid-state-directed-payments-to-hospitals-and-nursing-facilities

[15] Ortaliza J, McGough M, Cox C, Pestaina K, Rudowitz R, Burns A. How Will the One Big Beautiful Bill Act Affect the ACA, Medicaid, and the Uninsured Rate? [Internet]. San Francisco: Kaiser Family Foundation; 18 June 2025 [cited 5 August 2025]. Available from: https://www.kff.org/policy-watch/how-will-the-2025-budget-reconciliation-affect-the-aca-medicaid-and-the-uninsured-rate

[16] Liptak K, Holmes K. Inside Trump’s last 24 hours as he willed his agenda bill over the finish line. CNN [Internet]. 3 July 2025 [cited 5 August 2025]. Available from: https://amp.cnn.com/cnn/2025/07/03/politics/how-trump-passed-agenda-bill

[17] Liptak K, Holmes K. How the Passage of the “Big, Beautiful Bill” Could Impact Med Students and Hospitals. U.S. News & World Report [Internet]. 18 July 2025 [cited 5 August 2025]. Available from: https://www.usnews.com/news/national-news/articles/2025-07-18/how-the-passage-of-the-big-beautiful-bill-could-impact-med-students-and-hospitals

[18] Smith J, Johnson A, Lee R. Projected Effects of Proposed Cuts in Federal Medicaid Funding on Health Outcomes. Ann Intern Med. 15 July 2025;25(7):716–723. doi: 10.7326/ANNALS-25-00716.

[19] Werner RM, Coe NB, Roberts ET, Galvani AP, Pandey A, Ye Y. Projected Mortality Impacts of House-Passed Budget Reconciliation Bill Provisions [Internet]. Washington, DC: U.S. Senate; 3 June 2025 [cited 5 August 2025]. Available from: https://www.sanders.senate.gov/wp-content/uploads/LDI-Yale-Letter-Final-1.pdf

[20] Leonard Davis Institute Staff. Estimated Overdose Deaths Due to the Loss of MOUD in the One Big Beautiful Bill Act [Internet]. Philadelphia: University of Pennsylvania; 2 July 2025 [cited 5 August 2025]. Available from: https://ldi.upenn.edu/our-work/research-updates/estimated-overdose-deaths-due-to-the-loss-of-moud-in-the-one-big-beautiful-bill-act

Each US state is required to provide a set of mandatory health benefits to qualifying citizens under federal law, with an option to provide additional benefits through the state planning process and legislature. Better known as Medicaid and the Children’s Health Insurance Program (CHIP), each state’s health plan is funded through federal and state dollars. In the state of Oregon, the Oregon Health Plan (OHP) has provided Medicaid and CHIP to its citizens since 1993 [1]. Often recognized as a national leader in health care reform through broad coverage eligibility criteria, the state covers 1.4 million Oregonians who earn up to 138% of the federal poverty level (FPL), or roughly $21,000/year for one person, or more than $43,000/year for a family of four [1, 2].

In 2024, Oregon used Section 1331 of the Affordable Care Act to further expand eligibility for publicly funded health insurance from 138% to 200% of FPL for people who would otherwise be eligible for federally subsidized marketplace coverage. This policy change increases the income limit to qualify for public insurance in Oregon to $30,000/year for individuals ($62,400/year for a family of four) [3].

In addition to reducing transitions on to and off of public insurance, referred to as “churn”, Oregon’s Basic Health Program uses mostly federal dollars to provide tens of thousands more people coverage for essential health benefits without premiums or co-pays. The uninsured rate in Oregon prior to the eligibility expansion was 6% [5], and officials expect the plan to cover 100,000 individuals by 2027, 30,000 of whom would not have had insurance otherwise [5].

Only two other states, New York and Minnesota, have expanded their Medicaid benefits beyond the traditional federal income limits allowed under the Affordable Care Act (138%), yet Oregon is the first do so without passing on premiums or cost-sharing to Basic Health Plan enrollees.

References

[1] Oregon Health Authority. Brief history of health services prioritization in Oregon. Available from: https://www.oregon.gov/oha/HPA/DSI-HERC/Documents/Brief-History-Health-Services-Prioritization-Oregon.pdf

[2] OPB. Oregon health plan eligibility checks near completion. Available from: https://www.opb.org/article/2024/07/02/oregon-health-plan-eligibility-checks-near-completion

[3] Medicaid Planning Assistance. Federal poverty guidelines. Available from: https://www.medicaidplanningassistance.org/federal-poverty-guidelines

[4] Oregon Health Authority. Oregon Health Plan Bridge program. Available from: https://www.oregon.gov/oha/hsd/ohp/pages/bridge.aspx?utm_medium%3Demail%26utm_source%3Dgovdelivery

[5] Oregon Health Authority. Basic Health Program presentation. 2023 Jul 11. Available from: https://www.oregon.gov/oha/OHPB/MtgDocs/5.0%20Basic%20Health%20Program%20presentation_07.11.23.pdf

6.1.1. Aims, objectives and goals of the ACA

The ACA reflected the broad public goals of the Obama Administration and the Democrats in Congress who passed this legislation. Any broad consensus as to goals disguised deep divisions within society as to how those goals could best be achieved. Testimony to this was the election of Donald Trump with his campaign promise to repeal the ACA.

At the time that the ACA was being formulated uninsurance was a major problem in the United States. About 44 million people (15% of the population) were uninsured, 56 million (19%) had been uninsured for at least part of the year and 32 million (11%) had been uninsured for more than a year (Cohen &d Martinez, 2007; Connors & Gostin, 2010). An additional 41 million people were estimated to be underinsured (Commonwealth Fund, 2017). To increase access the ACA included both private and public insurance. To lower the uninsured rate an individual mandate requiring that nearly everyone have health insurance was included, with government premium subsidies for low- and middle-income uninsured individuals and families who were ineligible for Medicaid or employer-sponsored insurance. Guaranteed issue (requiring insurers to sell policies to all who wished to buy them, including those with pre-existing conditions) and community rating were also adopted to reduce the percentage uninsured (exceptions are explained below). To address underinsurance, problems of access were managed by setting up required health benefits for insurance policies, an end to cancellation of insurance when a recipient became ill and made claims, an end to pre-existing conditions limitations in insurance policies, and the elimination of lifetime maximum pay-outs on insurance claims (Reuters, 2010).

A second goal of the ACA was to reduce the overall cost and/or the rate of increase in health care costs, and to decrease the already large US fiscal deficit (Oberlander, 2011).

Finally, improving quality of health care was a focus of the ACA (Schoenbaum et al., 2011; Nolte & McKee, 2012). Geographical variations in health care costs and practice differences across the United States raised the question of what is “best practice” and what is appropriate health care (Schoenbaum et al., 2011). The belief that as much as 30% of health care did not improve patient health fuelled calls for both cost savings and quality improvement (IOM, 2010; Gabow, Halvorson & Kaplan, 2012).

6.1.2. Background and underlying issues in health policy reform

This section examines the context of US health reform legislation: its history, the culture, the divided policy environment, and institutional structures (including federalism).

The political culture of the United States influenced the content of President Obama’s ACA and President Trump’s health policies. In the United States, as is the case in many other countries, there is reliance on market competition and on entrepreneurship (Page & Jacobs, 2009). Individual rights and personal responsibility play an important role in US political values. This meant that many of the ACA’s goals had to be accomplished with a “limited increase in federal governing authority” (Morgan & Campbell, 2011, p. 387). And for many in the Trump Administration, even the pro-competition, private sector aspects of the ACA were not reassuring. They remained suspicious of the role assigned by the ACA to government regulation (Eilperin, 2017).

Health care reform over the last decade occurred at a time when political partisanship was at historic highs (Galston, 2010; Murray & O’Connor, 2013). Policy differences between the Republicans and the Democrats elected to Congress were greater than at any other time since the 1880s (McCarty, Poole & Rosenthal, 2008). Substantial political differences also existed within each political party (Marsh et al., 2012a, 2012b). Thus, constant negotiation and renegotiation on the content of the ACA legislation was required within the majority party, at that time the Democrats, before it was adopted.

While the Democratic Party was the majority party in both houses of Congress, its margin of control in the Senate was narrow because of the need to have a “super majority” of 60 out of 100 seats to ensure the passage of contentious legislation in that chamber (Morgan & Campbell, 2011). By the end of 2009, both the House of Representatives and the Senate had adopted health care reform bills, albeit different versions. In January 2010, however, the Democratic Party lost a special election held in Massachusetts for a Senate seat, leaving Obama’s party in the Senate one vote short of the 60 needed to finalize the bill by a straightforward vote. In the end, the Democratic leadership in Congress employed a legislative mechanism called “reconciliation”, generally reserved for budget legislation and requiring only 51 votes, to pass the final bill (Goodnough & Sack, 2011).

Counterbalancing this was that President Obama had a great deal of political capital due to his margin of victory in the 2008 election.

During President Trump’s first years in office, beginning in January 2016, the Republican Party held a clear majority in Congress in both the Senate and the House of Representatives. This should have facilitated the implementation of his health policies. But reforming the health system proved difficult because of political divisions within the Republican Party and the failure of the congressional Republicans to formulate a convincing replacement of their own.

The Trump Administration’s attempts to repeal the ACA failed because it was unable to mobilize adequate congressional support. In response, it then turned to approaches to modify the ACA and reduce its scope that are available only to a president and do not require congressional approval. These include executive orders, which have the force of law in many cases, presidential proclamations, presidential memoranda, presidential decision directives, and “statements” that accompany legislation when it is signed into law. In addition, these methods had the advantage of preserving the revenue accruing from the taxes that were embedded in the ACA. If the ACA had been completely repealed, the federal government would have lost this revenue.

Finally, US political structures posed an obstacle for health care reform legislation for both the Obama and Trump Administrations. In the US political system, with its separation of powers, it is very difficult to adopt comprehensive, cohesively formulated policy programmes such as those more commonly observed in parliamentary systems of government (Rice & Unruh 2016, Chapter 12). Historically in the United States each elected legislator could be independent of their party on any given issue and the system tended to be more open to stakeholder influence than in a parliamentary system (Rosenau, 1994). But over the years and by 2008 parties had evolved to become more centralized and cohesive.

Researchers point to constraints on health care reform legislation and the ACA bears out the findings (Volden & Wiseman, 2011). As an institution, Congress is subject to enormous outside influence because it is complex, and made up of two chambers, many committees and even more subcommittees. Evidence also suggests that health policy legislation needs the strong support of the majority party and its congressional leadership to be adopted. It is not the case that moderate and bipartisan approaches to health policy in Congress are more successful. The ACA did not have a single Republican vote, but it was still enacted. Similarly, efforts to repeal it subsequently did not garner a single Democratic vote in the Senate. Historically, health policy legislation is more likely than policy proposals in other issue sectors to end up in Congressional gridlock (Volden & Wiseman, 2011).

6.1.3. The policy process

How the content of the ACA was developed

The ACA is an enormous piece of legislation and it has transformed the US health system. This section considers how the content of the legislation was developed by key actors in the policy-making process: the president, Congress, the Supreme Court, stakeholders and the states. It outlines President Trump’s process to amend the ACA. In the United States the president and Congress can both formulate legislation. They shared significant roles in the development of the ACA, as did the two main political parties. Stakeholders also played an important role in the development of the bill, including health care providers, pharmaceutical manufacturers, insurers, businesses and the states.

Key actors: the president, Congress and the parties

A president’s role is critical in the United States, but presidents vary as to the success with which they use their authority and influence. In matters of domestic legislation, such as health care, the president’s influence is more limited than in foreign policy (Neustadt, 1991). The president is not like a prime minister who can order the governing coalition in parliament to vote for legislation. A winning coalition in the US Senate or House of Representatives must be negotiated for each piece of legislation. Each party is a diverse collection of interests with substantial internal diversity (Marsh et al., 2012a, 2012b). This means that support of the Congressional leadership of the majority party in the Senate and House of Representatives is critical, though not sufficient, in gathering enough members partly to achieve a winning coalition on any piece of legislation (Volden & Wiseman, 2011; Stolberg & Pear, 2019).

President Obama’s strategy in moving forward with health reform after his election in 2008 was influenced by former President Clinton’s failed attempt at health care reform in 1993, which many believe was unsuccessful because the Clinton White House did not involve Congress in drafting the legislation until late in the process (Brown, 2011). Learning from that experience, President Obama encouraged Congress to take the lead in 2009 and simultaneously ensured that stakeholders with vested interests in health care reform did not sabotage the effort. This meant allowing Congress to formulate the legislation at the same time as he offered stakeholders incentives to stay committed. The Democrats attempted to secure a few Republican votes for the legislation so that it could be designated as bipartisan, but their efforts failed.

As mentioned in section 6.1.2, in early January 2010 there were two different health reform bills before Congress but with the Democrats being one vote short in the Senate to pass their bill, the House had to adopt the Senate version and use the special legislative mechanism of “reconciliation” to pass the ACA.

The Supreme Court

The Supreme Court is the “referee” in the US political system. One of its main roles is to judge the constitutionality of final legislation once it is adopted. In November 2011 the Supreme Court announced that it would hear challenges to the ACA brought by a majority of the states (Bravin, 2011; Liptak, 2011). The court agreed to rule on the constitutionality of some aspects of the legislation, including the individual mandate and the Medicaid expansion (Baker, 2011b). The Attorneys General of the suing states argued that Congress exceeded its power by requiring that states respect the more comprehensive federal eligibility standards, or they would lose federal government matching funds for their entire Medicaid programme. The states argued that this violated their sovereignty under the Constitution (Abelson, Harris & Pear, 2011).

In June 2012 the Supreme Court held that the ACA was largely constitutional. The individual mandate requiring most individuals to possess public or private health insurance coverage or pay a penalty was upheld, the reasoning being that Congress has the authority to implement taxes. However, the court argued that in the case of Medicaid expansion, “Congress could not constitutionally force the states to implement a new program under the threat of losing existing program funding” (Jost & Rosenbaum, 2012; Supreme Court of the United States, 2012). Technically the decision did not strike down the Medicaid expansion but instead prevented the HHS from requiring that states participate in it. This left the participation in Medicaid expansion effectively optional for each state. However, many incentives remained for states to expand Medicaid as explained in subsection ACA Implementation in section 6.1.4, including federal subsidies of 90% of the costs. Failure to expand Medicaid could negatively affect state budgets and increase the cost of uncompensated care for states. It would reduce the multiplier effect of federal funds flowing into a state’s economy (Musumeci, 2012). Nevertheless, at the end of 2020, 14 states had not expanded Medicaid.

In addition, the Supreme Court’s two major decisions about the law had the effect of making it virtually impossible for many people with incomes below 100% of the poverty level who live in states that don’t fully participate in the Medicaid expansion to obtain health insurance at a price they could afford.

The Supreme Court took on the abortion issue in 2018–2019.[12] It prohibited insurers from using funds from federal agencies to pay for abortion except in cases of rape, incest or when the mother’s life is in danger. But it ruled that customers could purchase separate abortion coverage and that funds for such coverage must be held separate from other insurance company funds (Cornell Law School, 2020; Sobel, Salganicoff & Ramaswamy, 2020).

The Supreme Court sided (8–1) with insurers, ruling that risk corridor payments were constitutional. Risk corridor payments, which were in effect from 2014 to 2016, limited losses and gains by insurers beyond an allowable range. They were included in the ACA legislation but Congress had not funded them. The decision in the case of Maine Community Health Options v. United States awarded US$ 12 billion to be given to the insurers and stated that the government had to make the promised payments indicated in the ACA legislation. Even the liberal judges on the Supreme Court agreed that “the government should honor its obligations” (Keith, 2020).

The Supreme Court will continue to influence the development of the ACA. Currently pending is a case, California v. Texas, that questions the constitutionality of the ACA again. Those states supporting Texas seek to have the whole of the ACA struck down. The Supreme Court has agreed to review three legal questions in the case: (a) whether Texas and the individual plaintiffs have standing to bring the lawsuit to challenge the individual mandate; (b) whether [recent tax legislation] rendered the individual mandate unconstitutional; and (c) if the mandate is unconstitutional, whether the rest of the ACA can survive. A decision by the Supreme Court is not expected until after the November 2020 presidential and congressional elections (Musumeci, 2020).

Stakeholders and their input

The US health care system accounts for nearly 18% of the economy and the amount of money involved in stakeholder lobbying of Congress is not trivial. In 2016 alone, half a billion dollars was spent on lobbying by pharmaceutical companies, hospitals and health providers making the largest contributions (Khullar, 2017). Not surprisingly then, many nongovernmental stakeholders affected by the ACA were involved in its development. Health care providers were “at the table” negotiating the content of the ACA (Hacker, 2011). Physician groups were split, which handicapped them (Quadagno, 2011). Conservative state physician associations such as the Texas Medical Association and the left-of-centre Physicians for a National Health Program opposed the ACA for different reasons. But the influential AMA provided limited support at first, later opposing some points, but in the end endorsed both the Senate and the House bills (Hacker, 2011). Physician groups hoped for relief from a restrictive provision on Medicare physician fee schedule prices and sought other revenue-enhancing provisions.

The AHA, the Federation of American Hospitals and the Catholic Health Association agreed to accept US$ 155 billion less in Medicare payments for a period of 10 years. In exchange they expected an increase in revenues of around US$ 171 billion because many more Americans would have insurance and charity care would be reduced (Jacobs & Skocpol, 2010, pp. 70–1). Hospitals agreed to a gradual reduction of US$ 50 billion in government payments for treating the uninsured. They also agreed to changes that would reduce federal payments for avoidable and inappropriate hospital patient readmissions by about US$ 2 billion. Finally, a lower Medicare payment update to hospitals and other payment cuts were projected to yield US$ 103 billion in savings to the government (Terry, 2009).

Pharmaceutical manufacturers received the assurance that they would not be closely regulated by the government. There would be no price controls on drugs, such as those in effect in most other high-income countries. As requested by the pharmaceutical manufacturing sector, the ACA also prohibited US residents from buying and importing medication from other countries where drugs are less expensive. The volume of drugs sold was expected to increase among the working age population because of the insurance expansions of the ACA, and among seniors due to more complete coverage under Part D of Medicare. To obtain these benefits the pharmaceutical manufacturers gave up roughly US$ 85 billion in revenue. In return they could look forward to “tens of billions of dollars in additional revenue as more people with insurance visit doctors and fill prescriptions” (Abelson, 2010). In the end the pharmaceutical sector accepted the ACA and put around US$ 100 million into advertising to support its passage (Jacobs & Skocpol, 2010, pp. 70–1).

Insurers, represented by America’s Health Insurance Plans, vacillated, but they did not actively oppose the health care reform legislation as they had in 1993. In exchange for accepting greater government regulation, they received an assurance that nearly everyone would be required to purchase insurance as a protection against adverse selection. They were also guaranteed that there would be no competition from a public-sector insurance plan. When the Trump Administration proposed to eliminate the individual mandate, with the cooperation of Republicans in Congress, it was strongly opposed by many within the health insurance industry, where it was viewed as reneging on the agreement they had negotiated with the Obama Administration at the time the ACA was adopted.

The new regulations that the insurance companies had agreed to were significant in the US context: some price controls, guaranteed issue (selling insurance to all who sought to buy it even if the individual had pre-existing conditions), modified community rating, and the requirement that insurers generally spend 80–85% of premiums on patient care (called a medical loss ratio (MLR)) (Quadagno, 2011).

The business community was divided. Small business interests were united in their opposition to the ACA. Large employers that self-insured were exempted from many of the ACA regulations (Pecquet & Baker, 2011; Linehan, 2010). These and other employers received “grandfathering” status for their health plans if they did not make important changes to what was in place in their plans at the time the ACA was adopted. But starting in 2015 the ACA imposed a penalty of US$ 2260 per employee on employers with more than 50 employees if they did not provide adequate health insurance for 95% of their employees. The Trump Administration attempted to remove this obligation, called the Employer Shared Responsibility Provision (ESRP), and the penalty through executive orders, but in 2017 the IRS announced that it would continue to be enforced, as only Congress can modify laws, including the ACA (Cowley, 2017). As a result, this employer mandate was still in effect as of the end of 2020.

States as stakeholders

States are also stakeholders and they too participated in the formulation of the health reform legislation. But the interests of the 50 states are diverse. Some were led by Republican governors while others were led by Democrats. Some states such as Massachusetts and Vermont already had high-performing health systems (as defined by dozens of empirical indicators), while others did not (Commonwealth Fund, 2007; Radley McCarthy & Hayes, 2018; Silow-Carroll & Moody, 2011). The states did not all agree on the goals that the ACA sought to achieve, such as increased access to insurance. Some states took their cases against the ACA to the Supreme Court and won when Medicaid expansion was made optional.

Public involvement in developing the ACA

The role of the public in determining the content of the ACA was less decisive than that of other stakeholders (Cook, 2011). Public interest in health care legislation was high while it was under consideration and the media focused on it (Jacobs & Skocpol, 2010). Overall support for the ACA remained below 50% in 2012 with 41% of Americans favourable to it and 41% unfavourable (Kaiser Health Tracking Poll, 2012). Over the years public support only occasionally reached 50% or higher. But by May 2020, 51% were favourable and 41% were unfavourable according to the Kaiser Family Foundation’s Health Tracking Poll. It was supported by 80% of Democrats, 55% of independents, but only 19% of Republicans (Kaiser Family Foundation, 2020b).

From the beginning public approval of a few specific elements in the ACA was quite high – for example requiring insurance companies to sell insurance to everyone, including those with pre-existing medical conditions. Much of the public was, however, set against the idea of the individual mandate (Kaiser Family Foundation, 2011c).

- 12. President Trump has named two new justices to the Supreme Court since his election, Neil Gorsuch and Brett Kavanaugh. Future legal cases regarding the ACA that are taken to the Supreme Court will be assessed by a Supreme Court with a more conservative bent. ↰

6.1.4. The Affordable Care Act

The adoption of the Patient Protection and Affordable Care Act (ACA) in the United States in 2010 was a major accomplishment after decades of failed attempts. The scope of those accomplishments is outlined below and notable limitations of the ACA are also discussed. In short, access to insurance for many has improved since the ACA became law, especially those already ill and those for whom costs are prohibitive. Increased consumer protection, through regulation of the health insurance industry, was one of the most important accomplishments of the ACA, though in 2017–2018, the Trump Administration weakened or eliminated some of these regulations.

The ACA did not accomplish all that many of its proponents wished: implementation was delayed and many were left uninsured (some of those with low income, many undocumented immigrants, those who are eligible but did not enrol, those who preferred to pay a penalty rather than buy insurance, those who would have to pay more than 8% of their income to purchase insurance, and some individuals with religious objections). In states that did not choose to expand Medicaid, many very poor people remained without health insurance. Administrators were not empowered to enforce some important elements of the law, as explained below. The absence of a public insurer precluded competition between the public sector and for-profit and private (mostly for-profit) sectors in the individual insurance market. A long-term care benefit failed to be implemented even though it was included in the legislation. Many potential mechanisms to control costs were not included.

Major characteristics of the ACA

This section examines how the ACA achieved increased access. It did so through two primary mechanisms, a combination of new and already existing insurance arrangements: (1) a mandate to possess insurance or to purchase it through ACA marketplaces; and (2) Medicaid expansion in many states. Low-income Americans benefited most because starting in 2014 they received Medicaid coverage if they lived in a state where Medicaid expansion went forward. Others in this group received subsidies for purchasing private insurance. The poor living in states that did not expand Medicaid did not benefit from either of these two mechanisms, however.

The section also examines claims by proponents that the ACA was designed to control rising health care costs and reduce the national deficit. These measures included greater regulation of insurance pricing, increased competition to lower the price of insurance through the ACA marketplaces, reform of payments to Medicare, bundled payment systems and the potential for future implementation of the results of several pilot projects. Also reviewed are the policy strategies in the ACA expected to pay for health system reform.

The ACA included quality improvement measures that are discussed below. Improved medical care may result from the ACA’s emphasis on primary care and ACOs (CMS, 2019a). The use of comparative effectiveness (although not cost-effectiveness) information was encouraged. Incentive systems in some programmes and pilot research projects attempted to link quality to outcomes. More information on the best medical care available has been made public and transparency has been encouraged.

In addition, the ACA’s potential impact outside the health sector is reviewed here. This includes the reduction of job-lock, reduction of bankruptcy due to health care bills, reviews of insurance company proposals to increase premiums, and consumer protections.

ACA implementation

Implementation

While most major provisions of the ACA went into effect in 2014, several began earlier. One provision enabled 3.1 million young adults to be insured by permitting them to remain on their parents’ health insurance until the age of 26. Insurance companies could no longer refuse health insurance to those with pre-existing conditions and minimum loss ratio limits restricted the amount that insurers spent on administration, marketing and profits. The Medicare and commercial populations received free preventive benefits without co-payments, and gaps in their medication insurance for Medicare beneficiaries were to be gradually closed. There were tax credits available to many small employers and small businesses with lower-income employees to encourage them to offer insurance for their employees (Tolbert, 2010). Comparative effectiveness research was funded and grants for research on innovations on the topics of payments, delivery and organization of health care were distributed. Many consumer protections were put in place, including the external review of appeals of health insurance company decisions about coverage. A centralized website to provide consumer information was established. Some states received federal funds to offer consumer assistance in choosing an insurance plan (Kaiser Family Foundation, 2011a).

More recently, the Trump Administration’s health policies removed or modified several of these health reform elements. These are discussed below. Funds for assisting consumers to select a health policy have been sharply reduced. The time period for enrolling in a health plan in the marketplaces was reduced from 92 days to 45 days (Investopedia, 2018).

Access

The ACA requires health insurers to sell policies to all those seeking to purchase them (guaranteed issue) at a fixed rate for each age category, tobacco use status, within a specific family size and within a regional area (community rating). The most significant of these is the one regarding age, where the legislation required that premiums charged to older adults be no more than three times those of younger adults. Discrimination based on gender or health status (an individual’s health history) is not allowed for plans sold on the ACA insurance markets. An annual ceiling of approximately US$ 7900 for OOP costs (deductibles, co-payments and coinsurance) for individuals and US$ 15 800 for families was also required by the ACA in 2019. In 2014 minimum standards as to what must be included in all health insurance plans went into effect, addressing the problem of the “underinsured” – those with less than adequate coverage (Commonwealth Fund, 2010a). States had an important role in setting up and implementing these standards.

President Trump’s 2018 executive orders allowing the sale of “short-term” insurance lasting up to three years without any restrictions on what must be covered will circumvent some of these rules. These short-term policies are expected to attract mainly healthy individuals, thus increasing the cost of health insurance for those continuing to purchase plans on the ACA marketplaces. These are discussed more below.

The ACA included a mandate that every resident must have health insurance starting in 2014. There were exemptions for those with moral or religious objections, for American Indians, for undocumented immigrants, for those in prison, for those who can prove that the lowest cost plan option exceeds 8% of their income, for those whose income is so low that they are not required to file a tax return, and for the very poor residing in states that do not expand Medicaid (Kaiser Family Foundation, 2011a).

Removal of the penalty by Congress in 2017 could undermine the risk pool of the health care marketplaces where individual policies are sold. Most of those choosing, legally and without penalty, to forgo health insurance are expected to be healthy and younger than the general population. Therefore, the cost of insurance for those remaining in the purchasing pool will be higher as they are likely to be sicker and older than those who opt out for whatever reason.

The Supreme Court’s decision in 2012 made Medicaid expansion optional and some states have opted out of the Medicaid expansion, arguing that they could not afford it. A range of options were available to states. There was no deadline for states to make choices about Medicaid expansion and some did so at a later date, though they did not receive the full array of financial incentives offered to states that expanded Medicaid early on. To date, 37 states (including Washington, DC) have adopted the Medicaid expansion and 14 states have not adopted the expansion (Kaiser Family Foundation, 2019a).

Because the funding for expansion was largely the responsibility of the federal government, states had an incentive to participate. “Specifically, for people who become newly eligible for Medicaid under the expansion, the federal government will cover 100% of those costs from 2014 through 2016 and a share declining to 90% of the costs in 2020 and thereafter” (CBO, 2012b, p. 9).

It is not entirely certain how much the Supreme Court’s 2012 decision to not require states to expand Medicaid is reducing access to health insurance for the poor (CBO, 2012a). While many of the poorest individuals live in states that have not expanded Medicaid, many of those with incomes below 100% of the FPL remained uninsured and cannot receive federal subsidies when purchasing coverage in the ACA’s insurance marketplaces. However, those with incomes above 100% of the FPL met the requirements for purchasing insurance on the ACA markets with substantial federal subsidies (CBO, 2012b, p. 11). Individuals were also exempt from purchasing insurance for other reasons, as outlined above.

Most people in the United States obtain health insurance through their employer and this continued after the ACA was adopted. Employers with 50 or more full-time employees who did not offer insurance were obliged to pay a penalty. The same was true if coverage did not meet state standards, if it was too expensive for employees to afford or if employers asked new employees to wait more than 60 days for coverage to begin (Tolbert, 2010). Some employers with fewer than 50 employees received special tax deductions for offering health insurance, but even if they did not offer it, they were exempt from penalties.

The ACA included the mandatory creation of state health insurance marketplaces – online markets where insurers compete to sell state and/or federally compliant policies to individuals and small businesses. If states chose not to implement an ACA marketplace, the federal government was mandated to step in and make a federal ACA marketplace available to the residents of these states. Up to half the states allowed the federal government to administer these ACA marketplaces for them. Several states worked out a partnership with the federal government to organize and implement an ACA marketplace (Mercer, 2013). States were permitted to alter these decisions and to take over the responsibility at any time in the future.

The ACA included sliding scale premium subsidies for individuals and families with incomes between 138% and 400% of the FPL to help them purchase insurance through these marketplaces. Most individuals making between US$ 14 856 and US$ 44 680 in 2012, and families with incomes between US$ 30 657 and US$ 92 200 were eligible for subsidized premiums. The dollar amount differed depending on the family size because the FPL is family-size dependent.

The ACA expanded access to primary care by increasing funds for local clinics and Federally Qualified Health Centers (FQHCs) (Abrams et al., 2011). Close to US$ 11 billion was originally anticipated for these programmes but this was reduced by Congress. In early 2018 Congress adopted the Bipartisan Budget Act of 2018 and President Trump signed this law. It reduced funding for the FQHCs to a total of US$ 7.8 billion for fiscal years 2018 and 2019 (Waters & Little, 2018).

Cost controls and deficit reduction mechanisms

The financial impact of the ACA was fiercely disputed from the beginning. Opponents argued it would cost too much and cause many employers to drop employee insurance coverage, preferring to pay the penalty. Proponents contended it would be revenue neutral or the rate of increase in national health expenditures would slow (Cutler, Davis & Stremikis, 2009). The CBO estimated that an overall reduction in the US deficit would result from the passage of the ACA (CBO, 2010a, 2010b).

One of the major concerns regarding the financial impact was that it would increase the price of premiums. There are various ways to measure this. A common way is to examine changes in premiums in the average “benchmark” plan, which is defined below as the second-lowest Silver plan in each county (weighted by enrolment). While average premium increases vary year to year, overall marketplace premiums increased considerably, by 75%, between 2014 and 2019 (Kaiser Family Foundation, 2019d).

There were, however, wide variations across the states because pricing decisions are made by insurers, for the most part, at the state level. In 2019, for example, premiums dropped 26% in Tennessee but went up 16% in Delaware. The full effect of President Trump’s executive orders on health insurance, as well as repeal of the individual penalty for not purchasing insurance, will not be known for some time.

Items in the ACA intended to protect against increases in the national deficit include productivity improvement incentives, reductions in subsidies to Medicare Advantage programmes (described in Chapter 3) (Biles, Arnold & Guterman, 2011), and penalties paid by hospitals for poor performance (e.g. inappropriate readmissions) and by large employers who fail to provide workers with adequate insurance. To reduce costs, the law also includes bundled hospital payment systems (explained below), and revenue from a surtax imposed on unearned investment income on wealthy taxpayers. Finally, other financing mechanisms in the law include a 40% excise tax (the “Cadillac tax”) on high-premium insurance plans typically characterized by low or no deductibles and co-payments (now repealed); health industry fees; rate reviews; and increased Medicare payroll taxes for the wealthy (CBO, 2010b).

The bundled payments for care improvement initiative in the ACA are another policy intended to control costs. It is voluntary and offers physicians, hospitals and other providers a single payment to cover all medical services required to care for a patient for a specific episode of illness (a specific medical condition or problem of expected limited duration). Traditionally, providers have been paid separately for each service received by a patient, a practice that some believe increases costs (US Department of Health and Human Services, 2011c). The Trump Administration modified this programme in ways that resulted in some providers declining to continue to be compensated for Medicare patients this way because they fear an overall reduction in payments (Dickson, 2018).

Another cost-control measure in the ACA is rate reviews. The ACA provides the means for states and the HHS to undertake rate reviews of insurance companies’ proposed premium increases and to publicize those deemed unfair. The bar was set at increases of more than 10% in the individual or small group market (Adamy, 2011), but was raised to 15% in 2018 (US PIRG, 2018).

An ACA provision requires insurers generally to spend a minimum of 80% (for individuals in the small group markets) and 85% (for those in the large group market) of sales revenue from premiums on medical care for policyholders, HIT and quality improvements. This, the MLR, is a term referring to the fact that money spent on medical care, rather than administration, represents a “loss” to insurers (Harrington, Mukamel & Rosenau, 2012). The MLR encourages health insurance companies to “eliminate wasteful administrative spending and increase the value consumers receive for their premium dollars” (Davis, Schoen & Stremikis, 2010; Baker, 2011a). In 2012 insurers that did not keep MLRs below the ACA target refunded US$ 1.1 billion to policyholders (Goodnough, 2012). Between 2012 and 2018 rebates have totalled US$ 4 billion (Norris, 2018).

Some administrative provisions of the ACA – requirements building on existing legislation such as the HIPAA of 1996 – include measures designed to reduce administrative costs, encourage accurate accounting and promote careful and efficient record-keeping. They establish compliance and certification rules that reduce fraud. Penalties for violations of administrative record-keeping are included (CMS, nd, b).

Improving quality

The ACA contains measures that its proponents expected to improve the quality of care at both the individual patient level and for the population in general by encouraging primary care, prevention, new models of integrated care (such as medical homes), the use of comparative effectiveness information by providers, quality measurement, the reporting of information about quality to consumers and improved medical care (Commonwealth Fund, 2010b; Kaiser Family Foundation, 2011a). It also discouraged the overuse of medical care (Jacobs & Skocpol, 2010, pp. 140–4) and set forth a national strategy for quality improvement. Increased payments to providers for primary care were included and it was hoped that this would encourage medical students to choose these specialties.

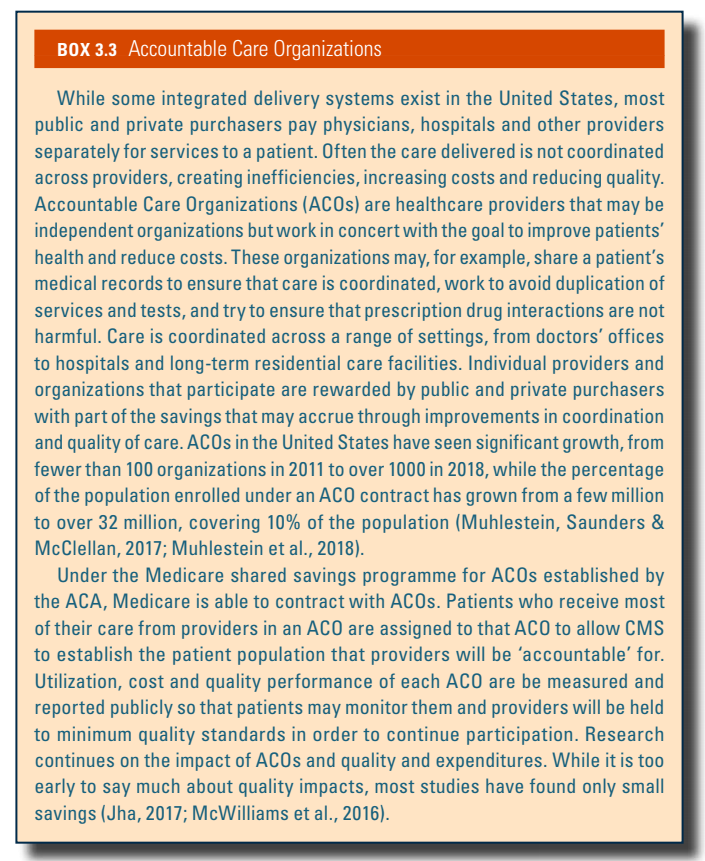

ACOs aim to improve quality and reduce costs in the Medicare programme and in the private sector by promoting integrated health care and including various methods of linking payment to outcomes. As noted in Box3.3, ACOs in the United States have seen significant growth, from fewer than 100 organizations in 2011 to over 1000 in 2018, while the proportion of the population enrolled under an ACO contract has grown from a few million to over 32 million, covering 10% of the population (Muhlestein, Saunders & McClellan, 2017; Muhlestein et al., 2018).

Box3.3

A 2018 MedPAC review of ACO model performance in Medicare has found that “some models— predominantly those at risk for both savings and losses (two-sided risk)—have produced small savings relative to their benchmarks set by CMS, and all have maintained or improved quality”, affording these ACOs “shared savings” bonuses (MedPAC, 2018a).

The Trump administration wanted to shift ACO programmes towards two-sided risk such that more providers would bear a financial risk if they did not reduce their costs of providing care (Minemyer, 2019). In 2018 there were about 50 ACOs that employed this financial risk model but 10 times as many chose payment models that did not include two-sided risk (NPC, 2018).

The ACA funds comparative effectiveness research. In 2011 the National Health Care Quality Strategy and Plan was prepared, and the resulting recommendations were reported to Congress for action (AHRQ, 2011). The ACA authorizes the collection of data on health care disparities including race, ethnicity, gender, linguistic minorities, the disabled and those who are underserved because of geographical location (rural and frontier populations). It sets up and funds the PCORI, a non-profit research organization tasked with providing the information patients and the public need to make informed decisions about their health.

Both positive and negative financial incentives were put in place. Beginning in 2011, a Center for Medicare and Medicaid Innovation Program was set up to undertake pilot programmes and demonstration projects that reward doctors and hospitals for quality health care (Zezza, Abrams & Guterman, 2011). Starting in 2015, the ACA began denying federal payments for Medicare services that are associated with some hospital-acquired infections. For hospitals with excessive preventable hospital readmissions Medicare reimbursements are reduced. Value-based Medicare payments link payment with results for physicians, hospitals, skilled nursing facilities, home health agencies and ambulatory surgical centres. The goal was for Medicare to become an active purchaser of higher quality health services, which could both reduce costs and improve quality of care (CMS, nd c). Bonus payments to Medicare Advantage plans that provide high quality were implemented, though the Trump Administration proposed changes to these.

The ACA includes nursing home transparency regulations designed to improve protective services for elderly residents through closer oversight, which could result in better quality nursing home care if consumers and their representatives are vigilant and monitor the information made available to them. Many health plans do not do a sufficient job of monitoring quality of the nursing homes in their network (Graham et al., 2018). The ACA gave nursing home patients broader rights to internal and external appeal of decisions by insurers, including coverage denials. In addition, Medicare obtained the right to collect and distribute data about nursing home staffing levels. The success of these measures depends in part on the appropriation of adequate funds; such funds are not assured. In addition, it is not clear how recent deregulation orders will affect these ACA nursing home reporting regulations.

Other ACA provisions inside and outside the health sector

The ACA contains several programmes outside the formal health sector. They include opportunities and benefits for consumers, increased transparency, improved public health, an amplified role for the FDA, support for education of medical staff, increased research funding, a reduction of job-lock, redistribution of wealth and reduced fraud.

For example, consumer bankruptcy rates could be reduced as a result of ACA-related coverage expansions. It has been reported that 62% of those who plead personal bankruptcy in the United States do so because of medical bills they cannot pay, and that 75% of those who go bankrupt have health insurance (Himmelstein et al., 2009; Abelson, 2009). But other scholars dispute these numbers and the results of research appear to depend on how medical bankruptcy is defined and measured (Dobkin et al., 2018). Because the ACA originally required almost everyone to purchase insurance and because it set standards for insurance policies sold in the marketplaces, the number of people who go bankrupt because of medical expenses was expected to fall. But the high co-payments, premiums and deductibles appear to be fuelling continued bankruptcy for medical bills (Sanger-Katz, 2018).

The ACA was expected to simplify choices of health insurance for those individuals and small businesses that purchase it on the open market. Each insurance plan’s co-payments and deductibles were to be explained in understandable language and the differences between insurance options was to be made clear. There were four levels of insurance on the individual market (and for small businesses) through the marketplaces. Each has a different level of protection (actuarial value) with the highest level being the Platinum Plan, which covers 90% of a purchaser’s health bills. The Gold Plan covers 80% and the Silver Plan 70%. The Bronze Plan, the cheapest, covers 60% of the insured individual’s expenses (RAND Corporation, 2010). There is also a catastrophic plan, with a high deductible, for those under 30, with the intent to provide them with a less expensive option.

Premiums for each of the different ACA insurance plans are set by the insurers who will compete on the package and the price at each actuarial level. This means that insurers have an incentive to bargain with providers for discounts and to limit the services provided where possible. To discourage insurers from picking and choosing the markets in which they compete, all insurers are required to offer at least one Silver Plan and one Gold Plan within each ACA marketplace in which they participate. Insurers are not, however, required to offer plans at all four levels in every exchange in which they participate.

Beginning October 2018, the Trump Administration made new, short-term, insurance plans available to consumers. These policies were cheaper than ACA policies, but they generally provided fewer comprehensive benefits or were not available to those with certain illnesses. These policies could be renewed so they could be in effect for up to three years subject to state laws. Insurers selling these policies can deny coverage to those with pre-existing conditions. In short, they do not have to abide by the ACA’s regulations regarding covered services. The results are not yet known. One concern is that if younger and healthier people enrol in them, which is likely, premiums will rise in the ACA marketplaces as their risk pool deteriorates. Another is that consumers, attracted to lower premiums, will purchase them without realizing the policies’ restrictions – which already appears to be happening (Levey, 2019).

The ACA requires that all health plans sold in ACA marketplaces offer basic health benefits, but how this was achieved varied from state to state. There was no “single uniform set of ‘essential health benefits’ that must be provided by insurers. Instead, the ACA allows each state to specify the benefits within broad categories” (Pear, 2011). Once established at the state level, this basic minimum of services must be covered by all plans (Bronze, Silver, Gold and Platinum). Due to differing cost-sharing requirements, the value of the benefits will vary for the Bronze, Silver, Gold and Platinum plans. Under the ACA, insurance plans must be “equal to the scope of benefits provided under a typical employer plan”. Each state has the flexibility to define the 10 “categories of ‘essential health benefits’ that must be provided by insurance offered in the individual and small group markets …” (Pear, 2011). Basic health benefits and services are required in the following categories: ambulatory patient services; emergency services; hospitalization; maternity and newborn care; mental health and substance use disorder services, including behavioural health treatment; prescription drugs; rehabilitative and habilitative services and devices; laboratory services; preventive and wellness services and chronic disease management; and paediatric services, including oral and vision care. Many of the new short-term health insurance policies that the Trump Administration allowed to be sold are expected to exclude many of these services.

When the ACA first went into effect, its website was established by the federal government to provide consumer information. It offers multi-dimensional comparative quality ratings for many insurers (CMS, 2019b). It was intended to interface with the ACA’s marketplaces at the state level and to assist individuals in determining whether they are exempt from the requirement to purchase insurance as well as whether their health insurance plan meets ACA requirements. The goal was to increase comparability when shopping across coverage options as well by providing price information to individuals and small businesses (US Department of Health and Human Services, 2011d).

To increase transparency and reduce conflicts of interest among providers, the ACA requires full disclosure of financial relationships between doctors, specialists, hospitals, pharmacists and pharmaceutical manufacturers and distributors of drugs, devices, biological products and medical supplies.

The ACA law included about US$ 7 billion over five years for prevention and public health programmes such as smoking cessation and efforts to combat obesity. Also important to public health is the requirement that chain restaurants in the United States and vending machines display calories for their food products. The ACA assigned new responsibilities to the FDA to regulate and improve food labelling, and to assess and approve generic versions of biological medications. Most of these policy measures were well along in their implementation before the election of President Trump in 2016 (Evich, 2018).

The ACA also included provisions for health education and research. It provided medical students with financial incentives to pursue a career in primary care. Training programmes and loan cancellation were offered to those in primary care who agreed to work in underserved areas. It provided a range of health professionals with scholarships and loans to further their education and also increased Medicare payments for primary care residency programmes in FQHCs.

The Trump Administration did not rescind these programmes, but its immigration policies made it more difficult for foreign medical providers to enter the United States and practise. Many of these doctors choose to work in primary care, a field less attractive to many US graduates, and agree to practise in underserved areas.

In October 2017 Congress failed to reauthorize funding for the Community Health Centers Fund, an important source of support for these clinics where 27 million Americans obtained care (Cohen, 2017). In some cases, these funds were used by CHCs to hire immigrant doctors. In 2018 some of this funding was restored by the bipartisan opioids package entitled H.R. 6, SUPPORT for Patients and Communities Act.

Many analysts believe that the ACA reduced the problem of job-lock. Job-lock means that people fear changing jobs because someone on their policy has a pre-existing condition and they would not be able to buy or afford health insurance if they left their present employment that provided coverage (Quittner, 2017). There was little research on this topic available to evaluate it under the Trump Administration.

The ACA is redistributive, and this may lead to improved population health (Wilkinson, 1996). First, it implicitly redistributes financing of health services from the healthy to the sick through community rating and guaranteed issue. Second, it redistributes wealth through the taxes imposed under the law (Rice, 2011). To be deficit neutral, the ACA included fiscal policies that produced revenue to support increases in access through insurance expansion. The redistribution mechanisms in the ACA provide subsidies to the poor, financed by taxes on the wealthy, corporations and medical device manufacturers who will subsidize the less fortunate. The wealthy (defined as individuals with incomes of more than US$ 200 000 per year and families with more than US$ 250 000 per year) have paid more of their wages to Medicare since the ACA was adopted. Wealthier people also pay a tax on unearned income (stock market gains, real estate sales, dividends, annuities, etc.) (Tax Policy Center, 2010). A “Cadillac tax” was scheduled to begin in 2018 but was postponed and then repealed in 2019 before it went into effect. It would have required that employers pay a 40% tax on health insurance policies that are extremely generous (costing above US$ 10 200 per individual and US$ 27 500 for families).

The ACA included measures to reduce fraud in health care, a serious problem in the United States. Better screening for patient eligibility and monitoring providers halted many abuses in the Medicare and Medicaid programmes. Auditing has also lowered fraud. Penalties and sentences for criminal activity were also implemented immediately and the HHS was authorized to employ the same technology as credit card companies to fight fraud. The Health Care Fraud and Abuse Control Program (HCFAC), in existence prior to the ACA, registered US$ 4 billion in recoveries in 2010. Indictments increased dramatically. Predicted reductions in costs from the elimination of fraud in the future are approximately US$ 1.8 billion per year for 2015 (US Department of Health and Human Services, 2011e). The ACA attempts to further strengthen these efforts.

The Trump Administration’s record on fraud in health care was mixed. It has pursued pharmaceutical companies for fraud on several fronts. Congress approved removing a “gag order” that prohibited pharmacists from telling customers about cheaper drugs and President Trump signed this law in 2018 (Jaffe, 2018; Clark & Breslauer, 2018). But it was also reported that there had been agreements between pharmacies and insurance companies that had kept some pharmacists from disclosing cheaper drug options to consumers. The Trump Administration declined to enforce instances of corporate health care fraud (Radick, 2018), but it did retain health care fraud enforcement as a priority. The Trump Administration proposed US$ 751 million for the HCFAC for fiscal year 2018, a 10% increase over the 2017 budget (O’Quinn, Bronson & Greenfield, 2018).

The ACA included elements designed to maintain and strengthen the support of various stakeholders. For insurance companies the promise of more business in the form of many more customers who were required to purchase their product was an important incentive (Grogan, 2011). The fact that Congress abolished the penalty for the individual mandate was a disincentive for insurers because of the potential for adverse selection if healthier people opted out of insurance coverage. On the other hand, insurers benefit from a risk pool that was designed to guarantee that insurers receiving more than their fair share of enrollees with large claims would be compensated for this adverse selection. This is an important protection for insurers because in the United States about 5% of the population consumes half of health care expenditures (Hall, 2011).

In 2014 the ACA provided tax credits of up to 50% to small businesses (defined as those with fewer than 25 employees with an average wage of less than US$ 50 000) that provided health insurance (Internal Revenue Service, 2020).

Limitations of the ACA legislation

Uninsured and underinsured groups

Overall the ACA did increase the number of people with health insurance. But it did not provide an adequate remedy for all the uninsured in the United States. Still the number of uninsured went from 44 million in 2013 to less than 28 million in early 2017, largely as a result of the ACA’s expansion of Medicaid and its subsidies for purchasing individual health insurance on the ACA marketplaces. Most of the remaining uninsured after the ACA was fully implemented were low-income individuals (Oberlander, 2012).

Some elements of the ACA went into effect several years after the full implementation and this meant the uninsured rate remained higher, for longer. This deliberate delay resulted in part from budgetary reasons, but it was also because of negotiations with stakeholders and legislators.

Before the Supreme Court ruling that made the ACA’s Medicaid expansion optional for the states, about 33 million non-elderly people were predicted to gain health insurance because of the ACA’s Medicaid expansion programme. In total, 94% of the US population would have been insured, up from 83% prior to the ACA (CBO, 2010b; Schoen et al., 2011). In fact, the ACA increased the number with Medicaid coverage by about 16 million people from September 2013 to November 2017 (in the 49 states that reported data), many fewer than would have been the case if the ACA’s Medicaid expansion had not been ruled unconstitutional by the Supreme Court. Still, in 2018, 73 million individuals were enrolled in Medicaid or CHIP. Those obtaining Medicaid after the 2018 mid-term elections, as mentioned above, will add to the numbers covered under the public insurance programme.

An estimated 12 million undocumented immigrants remain uninsured in the United States. Under the terms of the ACA they are not permitted to buy insurance on the ACA marketplaces (CBO, 2010b; Parmet, 2018). If employers work with ACA marketplaces to insure their employees, then by definition, their undocumented workers are excluded. Individuals eligible for health insurance that fail to enrol in a health insurance plan, which includes Medicaid, will continue to be uninsured.

Another anomaly that results from the Supreme Court’s ruling allowing states to opt out of Medicaid expansion is that some of those below 100% of the FPL may not be eligible for subsidies. In 2019, 100% of the FPL was US$ 12 490 for individuals and US$ 25 750 for a family of four. Nationally, 61% of those with incomes below the FPL are enrolled in Medicaid (Kaiser Family Foundation, 2019e).

Until 2019 the ACA required those who chose not to purchase health insurance to pay a penalty. Some preferred to pay the penalty as in many cases it cost less than an insurance policy. Also exempt from the requirement to purchase health insurance were those for whom it would be unaffordable (costing more than 8% of income). This determination was based on the price of insurance available on the marketplaces. Insurance policies purchased on the marketplaces are expensive for the poor and for the middle classes and often have very high cost-sharing requirements.

Finally, Congress and President Trump proposed allowing states to file for waivers that contain a work requirement for those on Medicaid. States with approved waivers can require beneficiaries to be engaged in one of the following: work a minimum number of hours per month; be enrolled in school or other educational programme; participate in job, vocational, or job search training; or be searching for a job. In March 2019 seven states had their waiver proposals approved and eight had waivers pending approval (Haught, Dobson & Luu, 2019).