-

01 August 2025 | Policy Analysis

Cancer medicines removed from the benefits package -

03 February 2025 | Country Update

Changes in the basic benefits package in the Netherlands in 2025 -

02 February 2024 | Country Update

Changes in health insurance in the Netherlands in 2024 -

01 January 2023 | Country Update

Developments and changes in health care financing in 2023 -

01 October 2022 | Country Update

Changes in the basic benefits package as of 1 January 2023 -

01 January 2022 | Country Update

Changes in the basic benefits package in 2022 -

18 July 2021 | Country Update

Changes in the basic benefits package in 2021 -

18 April 2019 | Country Update

New expensive medicines that are used in hospitals will be placed ‘in transit’ before acceptance in the basic benefits package -

18 April 2019 | Country Update

Changes in the basic benefits package in 2019 -

26 September 2017 | Policy Analysis

The role of citizens in the health insurance market -

12 September 2017 | Country Update

Basic benefits package in 2018

3.3. Overview of the statutory financing system

References

Wat verandert er in het basispakket van de zorgverzekering in 2025? | Rijksoverheid.nl https://www.rijksoverheid.nl/onderwerpen/zorgverzekering/vraag-en-antwoord/veranderingen-basispakket

Authors

References

Rijksoverheid. What is changing in the basic benefits package [Wat verandert er in het basispakket van de zorgverzekering in 2024, accessed 1 February 2024. https://www.rijksoverheid.nl/onderwerpen/zorgverzekering/vraag-en-antwoord/veranderingen-basispakket

In 2022, there are two changes to the basic package: Patients discharged from the hospital two weeks after a CAR-T cell therapy should stay within one hour travel from the expert hospital for an additional two weeks after the discharge because of the possible occurrence of severe complications. Patients living further away from the expert hospital will be reimbursed for stay at a hotel or holiday home up to a certain maximum as they need to be in the hospital within one hour. The second change is the reimbursement for electricity costs for patients who are at mechanical respiratory support at home. They can claim the electricity costs directly from their health insurer.

Authors

The Netherlands has added coverage for paramedical care for patients recovering from COVID-19 (as of 18 July 2021), by adding several new drugs for different types of cancer and group day care for people with acquired brain injury to the benefits package.

Authors

New medicines that are used in hospitals are currently admitted to the basic benefits package without specific price negotiations. Since 2018, a General Order in Council regulates that these medicines are placed ‘in transit’, which implies that the medicines can be used in hospitals, but formally are not admitted to the basic benefits package yet. In the meantime the Dutch Healthcare Institute can do research in order issue an advice on whether the medicine can be included in the package and the Minister can negotiate with the pharmaceutical company on price. The regulation applies to medicines that cost more than 50,000 euro per treatment per year and in total more than 10 million per year; or that cost in total more than 40 million per year, regardless of the price per treatment.

Authors

The following treatments were added the package in 2019: Lifestyle intervention for people with moderate health risks due to overweight. The intervention is directed towards a sustainable change towards healthier food and more activity; Patients that need taxi transportation to go to their treatment now can get reimbursement for travel costs for consultation, tests and check-ups that are related to the treatment. Formerly, only the travel costs for the actual treatment could be reimbursed. Remedial therapy for COPD patients is now reimbursed from the first treatment (formerly, the first 20 treatments had to be paid out-of-pocket). Paracetamol (1000 mg per pill), Vitamin D and calcium are no longer reimbursed. They can be bought over the counter at pharmacies or drugstore.

Authors

Introduction

Since 2006, all Dutch citizens are compulsory insured under the Health Insurance Act. The Health Insurance Act defines three markets: the health insurance market, the healthcare purchasing market and the healthcare provision market. The envisaged role of citizens in the health insurance market is to purchase an insurance policy that provides good quality healthcare, purchased by their health insurer at a competitive premium. To enable this role, all citizens can switch insurance policy at the first of January of each year.

How many people make use of their right to switch health insurers?

In 2017, 8% of the insured population switched from health insurers. The lowest percentage of switchers was registered in the years after the introduction of the Health Insurance Act, with approximately 5%. Since 2011 yearly about 8 to 10% of the insured population switches insurers. The younger population (18-39 years of age) switches most often, in 2017 12% changed insurer. This is lower compared to 2016, when 17% switched. The lowest numbers of switchers are found in the elderly (aged 65 and over), where 3% switched in 2017. The differences between the age groups are stable over time. Collectives are organizations (such as employers, associations representing certain groups of the population) that negotiate a collective contract for their members with a health insurer. Collectives are allowed to negotiate a 10% discount on the premium.

Why do people (not) switch from health insurer

The price of the health insurance policy, including the voluntary insurance, is the most mentioned reason to switch. About 30% mentioned this as main reason to switch in 2017. The second mentioned reason was the expectation that the personal healthcare use would change in the next year (19%). About 16% changed because they were unsatisfied because of the price of the mandatory insurance package. 12% changed because they were unsatisfied about the coverage of their voluntary insurance and another 12% because they decided to enter a collective insurance.

From those who did not switch, 42% indicates that they are satisfied by the services provided by their health insurer. About one third does not switch because they are satisfied with the coverage of their total insurance package (mandatory and voluntary insurance). About 30% does not switch because of loyalty. They state that they do not switch because they have their insurance with their insurer already for a long time. Some people experience barriers to switch and stay with their current health insurer. About 3% does not change because they worry about questions concerning their health status. Among those with a self reported mediocre or bad health status, 9% mentioned this as a reason.

How are people insured?

About 90% of the insured have voluntary insurance as well. The premium of a voluntary insurance is on average 310 euro per year (in 2015). Virtually all insured have the mandatory and the voluntary insurance with the same health insurer (99.6%). About 70% has dental care included in their voluntary insurance. People who do not have voluntary insurance say that they expect not to use the care covered by this insurance (80%) or cannot afford the insurance (28%). About 66% of the population is insured via a collectivity. They save on average 38 euro on their yearly premium compared to individually insured persons.

Does the system work?

The insured seem to increasingly incorporate other considerations than price in their decision to switch, for instance, they switch because they expect their healthcare use to change. However, they do not mention quality issues as a reason to switch. Satisfaction with services is however an important reason to stay with the current insurer. This may be because of little differences between the quality of services of health insurers or because people do not have information on the quality. The fact that people mention health status as a reason not to switch is worrisome, because this may indicate the (perceived) existence of risk selection. In the Health Insurance Act, measures have been built in to prevent risk selection. Health insurers are obliged to accept all applicants for the basic insurance package, regardless of their risk status. In return they receive a risk-adjustment compensation for insured with predictable health care expenditure. However this does not apply to the voluntary complementary insurance.

Authors

References

W. van der Schors, A.E.M. Brabers, & J.D. de Jong. Deel verzekerden lijkt steeds vaker inhoudelijke overwegingen mee te nemen bij keuze zorgverzekering. [8% switches insurers. Share op people that take substantive considerations into account seems to increase] Utrecht: NIVEL, 2017

Vektis. Verzekerden in beeld 2017 [Portrait of the insured], Zeist, 2017

The basic benefits package will be expanded. Currently existing treatments remain in the package. In addition physical therapy for patients with arthrosis of the hip or knee joint will be covered for the first twelve treatments. Furthermore, cancer patients that receive immune therapy will have their transportation to and from the hospital reimbursed. After the establishment of the package for 2017, some new treatments have been incorporated in the package during the year. This concerns for instance new medicines for the treatment of hepatitis C and conditionally a new treatment of inheritable breast cancer and neurological stimulation for severe constipation.

Authors

3.3.1. Coverage

Who is covered

Basic health insurance is obligatory for all Dutch residents. Those working in the Netherlands and paying income tax to the Tax Office (Belastingdienst) but living abroad are also compulsorily insured. For two groups of persons an exception is made. There are special regulations for persons who refuse to insure themselves on grounds of religious beliefs or their philosophy of life (gemoedsbezwaarden) and for undocumented migrants (see section 3.6.1). The Ministry of Defence finances and organizes health care for military personnel (see section 3.6.1).

Children under the age of 18 are insured free of charge but have to be included in one of the parents’ plans. Most insurers also offer free complementary VHI for children together with the parents’ complementary VHI policy (Roos & Schut, 2008). Children are covered by a government contribution in the health insurance fund.

All Dutch residents are compulsorily insured for long-term care under the Wlz. The same exemptions apply as with the Zvw.

Uninsured and defaulters under the Health Insurance Act (Zvw)

Although basic health insurance is compulsory, not every citizen is insured. In 2013, 28 000 persons were uninsured and 316 000 persons were defaulters with a payment delay of at least six months (Ministry of Health, Welfare and Sport, 2014c). The number of uninsured individuals has been on the decline after years of gradual growth, since the government started in 2011 to track down the uninsured. Every month the ZiNL receives a report from the SVB. If it finds that a person has failed to purchase insurance, it will send a letter requesting that they do so. From that moment they have three months to purchase a health plan. If after three months the person still does not have an insurance policy, a penalty of €352 will be charged. After another three months, another €352 penalty will be charged. If the person nevertheless fails to purchase insurance, the ZiNL will purchase a plan on behalf of the uninsured for the duration of 12 months. A legally established premium (€122.33 per month in 2016; the standard (estimated) premium for a normal insurance policy is €99 in 2015) has to be deducted from the uninsured’s income either directly by the employer or by the social security agency (National Health Care Institute, 2015a).

The problem with defaulters has been harder to rein in, as evidenced by the approximately 2% of the population that is failing to pay their premiums (2013). There is a special protocol that should protect individuals from losing coverage. After six months of non-payment, defaulters are registered with the ZiNL. The ZiNL charges a so-called “administrative premium” of approximately €153 (130% of the standard premium). This premium has to be deducted directly from income by the employer or by the social security agency. It is charged monthly until the defaulter settles all debts with the insurer. In the meantime, the defaulter remains insured, but cannot switch to another insurer until the debt is settled (National Health Care Institute, 2015b). The level of the administrative premium has frequently been criticized for putting already vulnerable individuals in further financial trouble. There are plans to lower this premium in 2016.

3.3.2. What is covered

The benefit package of the basic health insurance under the Zvw 2015 consisted of:

- medical care, including care provided by GPs, hospitals, medical specialists and midwives;

- hospital care;

- home nursing care and personal care (assistance with eating, dressing, etc.);

- dental care for children until the age of 18; for older people only, specialist dental care and a set of false teeth are covered;

- medical aids and devices;

- pharmaceutical care;

- maternity care (midwifery care and maternity care assistance);

- transportation of sick people by ambulance or taxi;

- professions additional to medicine (allied health care): physiotherapy for persons with a chronic medical condition (the first 20 sessions relating to the condition are excluded; there is a limiting list of conditions) and for children below the age of 18; occupational therapy; exercise therapy and dietary advice to a limited extent; speech therapy;

- smoking cessation programmes;

- geriatric rehabilitation care;

- care for people with sensory disabilities; and

- mental care: ambulatory mental care and inpatient mental care for the first three years (after three years inpatient mental care is considered long-term care and is financed by the Wlz).

For some treatments, there are exclusions from the basic insurance package.

- For allied health care, generally, a maximum number of sessions are reimbursed.

- Some elective procedures, for instance cosmetic plastic surgery without a medical indication, are excluded.

- For in vitro fertilization, only the first three attempts are included.

The central government takes decisions on the content of the basic health insurance package, on cost-sharing, on tariffs for health services if not negotiable (based on advice from the NZa) and on services that are not subject to free negotiations. The ZiNL advises the Minister on what services should be included in the package. The main criteria refer to whether services are essential, effective, cost-effective and unaffordable for individuals. “Essential” refers to a service’s capacity to prevent loss of quality of life or to treat life-threatening conditions. The affordability criteria state that no services need to be included that are affordable for individual citizens and for which they can take responsibility (Brouwer & Rutten, 2004).

These criteria form the subsequent steps to be made before a decision is taken on inclusion or exclusion of services in basic health insurance and although they were formulated in 1991, they are still applicable today. In practice, the criteria are not always easy to apply. For instance, what constitutes “essential care” is arguable, and decisions can be hampered by a lack of information on the efficiency of a service. Other problems may arise with regard to treatments of diseases resulting from unhealthy behaviour, or when pharmaceuticals covered by basic health insurance are used by other than the intended patient groups (Brouwer & Rutten, 2004).

The Wlz provides institutional care (which can also be provided at home) for all citizens who need supervision 24 hours per day. Whether a person qualifies for this type of care is assessed in a needs assessment. The care can be provided in a residential long-term care facility or at home by a professional organization. Eligible people who nevertheless would prefer to stay at home and organize their own care can apply for a personal budget. Since January 2015 a government body, the SVB, manages the budget on behalf of the budget holder after reports about budget fraud. Previously, budget holders could manage their own budget.

Citizens who need care for less than 24 hours per day can receive nursing care and personal care at home via the Zvw. The needs assessment is performed by district nurses. When people need help with domestic care or social support, they may receive care under the Wmo. The objective of the Wmo is that municipalities support citizens to participate in society. This includes, for instance, home help, transport facilities and house adjustments. Municipalities first explore the opportunities of applicants to take care of themselves, with the help of their social network. If these resources are considered insufficient, publicly funded support will become available. Interestingly, municipalities are free to organize tailor-made support for their citizens, which may lead to different solutions among municipalities (see section 6.1 for some preliminary evaluations of the effects of the reform).

For long-term care provided under the Wmo the rights-based approach of the former AWBZ has been replaced with a provision-based approach. For example, municipalities may choose to substitute professional care with other care solutions, such as care provided by neighbours or volunteers, although the Act does not provide means to oblige the social network to help. All citizens can apply for support from their municipality. The municipality will decide whether help is necessary and what kind of help. Youth care under the Youth Act is available for all children under the age of 18 and their parents in the case of parenting problems and mental problems.

Social protection

Social protection in the Netherlands is not a part of the health care system and thus is regulated differently under different acts. To compensate for undesired income effects for lower-income groups, a “health care allowance” funded from general tax was created under the Wzt. The allowance is based on a “standard premium”. This is the estimated average of the premiums offered by health insurers plus the compulsory deductible and is set by the Minister of Health (Ministry of Health, Welfare and Sport, 2005). As a result, insured persons who choose an insurer with a lower premium are not “punished” with a lower health care allowance. The allowance is an advance payment per month and is based on the final tax assessment. Any difference between the total advance payment and the final entitlement will be settled with the individual. In 2013, 57% of Dutch households received a health care allowance. On average 41% of the premium was compensated for (Statistics Netherlands, 2015b). The total expenditure on health care allowance doubled from 2006 to €5.1 billion in 2013, whereas the number of households eligible for the allowance decreased because of stricter eligibility rules. The increase in expenditure is mainly due to the increase in health care allowance for the lowest income groups as compensation for the increase in the mandatory deductible. The maximum monthly health care allowance was €78 for singles and €149 for families in 2015.

Financial compensation for medical expenditure for chronically ill and disabled persons was abolished in 2014. In some cases exceptional medical costs can be deducted from income tax. Excluded from tax deductions are, inter alia, expenditure that can be reimbursed by health insurers or the municipality, cost-sharing for long-term care, glasses and walking aids such as walkers. Included are, inter alia, physical therapy, costs of transportation to a hospital, and some dietary costs. The costs should exceed a predefined income-dependent minimum.

Maternity leave is a right and allows for a leave of (at least) 16 weeks. Maternity leave may start six to four weeks before the expected date of birth. For employees on maternity leave, 100% of the salary is paid, with a maximum of approximately €200 per day in 2015. The employer is compensated by the Social Security Implementation Body (Uitvoeringsorgaan Werknemers Verzekeringen, UWV). Since 2008 self-employed women are also entitled to receive an allowance depending on the income of the previous year, with a maximum level of the legal minimum wage (UWV, 2015).

After two years of illness, employees receive a disability pension based on the percentage of income loss they experience due to their disability. The disability can be either mental or physical. Entitlement for a disability allowance and settlement of the percentage of disability are established by the UWV. The disability allowance is up to 70% of the last income for those who are partly disabled (between 35% and 80%). These individuals receive an allowance only for the percentage to which they are considered to be disabled. The allowance is up to 75% of the last income for those who are fully disabled (over 80%), under the Act on Income and Labour (Wet inkomen en arbeid, WIA). Under this Act, the employer and employee both have to work on reintegration into the labour process during the two-year waiting period. People who are less than 35% disabled do not receive any financial compensation.

Persons who were disabled before reaching 17 years of age or who became disabled during their formal education and who are expected to be unable to work for the rest of their lives are entitled to an allowance of a maximum of 75% of the legal minimum wage (Wet arbeidsongeschiktheidsvoorziening voor jonggehandicapten, Wajong).

How much of the benefit cost is covered?

The Netherlands operates a complex cost-sharing system but until now has upheld the principle that primary care is free at the point of delivery. All users of health care aged 18 and over have to pay a mandatory deductible per year, which does not apply to GP care, maternity care and care for children under the age of 18. Pharmaceuticals and tests prescribed by GPs and care provided by medical specialists after referral by a GP are also subject to the deductible. The mandatory deductible has increased substantially over the years, from €150 in 2008 to €385 in 2016. This deductible replaced the no-claim regulation that was in place in 2006 and 2007. The no-claim was an amount of money that was paid back when no or only little health care was used (Schäfer et al., 2010).

Reimbursement for pharmaceutical care is based on a reference pricing system called the Medicine Reimbursement System (Geneesmiddelen Vergoedings Systeem, GVS). This system categorizes pharmaceuticals in groups of therapeutic equivalents. Health insurers may list preferred medicines (see section 3.7.2), which means that patients who use other medicines with similar therapeutic properties may have to pay the difference in costs or the total amount. Some insurers do not charge the deductible when the patient uses the preferred medicine.

For residential long-term care income-dependent cost-sharing is applicable, ranging from €159 to €2285 euro per month.

More detailed information can be found in section 3.4.

Context

The Netherlands are facing a large increase in expenditure for medicines, of which cancer medicines make up a large share. In 2021, the Netherlands spent EUR 2.6 billion on medicines, 59% of which were for cancer treatments, urging for measures to contain costs. Stakeholders have agreed to review and evaluate the effectiveness of medicines in the Cross-sectoral Care Agreement (Integraal Zorgakkoord, IZA) (containing agreements for the organization and funding of care in the Netherlands) as new data become available.

Impetus

Following new studies into the effectiveness of cancer treatments, the Dutch Healthcare Institute has re-evaluated PARP inhibitors (a class of anticancer agents). The Dutch Healthcare Institute is tasked with providing advice to the government over the content of the basic benefits package. In practice, the Minister of Health follows this advice. Patients, healthcare professionals and health insurers have a say in this decision-making process. They can indicate which questions are important to consider in the assessments. In addition, they can comment on the outcome of assessments before their publication. Assessments are also reviewed by the Scientific Advisory Board of the Dutch Healthcare Institute, which consists of independent scientists, physicians, pharmacists, methodologists and health economists.

Main purpose of the reform

The main purpose of this revision is to contain costs and to slow expenditure increases on costly cancer medicines in order to keep the current health care system sustainable. Cancer medicines are among the most expensive medicines, and their share in the healthcare budget is rapidly increasing: Healthcare expenditure for cancer increased from EUR 0.8 billion in 2003 to EUR 3.7 billion in 2019. The growth in spending is primarily linked to the reimbursement of new treatments and early detection.

Content

Following recommendations of the Dutch Healthcare Institute, PARP inhibitors are no longer reimbursed for patients with those types of cancer that did not show improvement in either life expectancy or quality of life. For patient groups, in which effectiveness was proven, the medicines remain reimbursed.

Implementation steps taken and outcomes to date

The measure has been implemented as of June 2025. Patients no longer eligible for reimbursement but who started treatment before this decision came into force will be allowed to continue their treatment.

There are some critical voices questioning this decision. The Dutch Federation of Cancer Patients believes too much emphasis has been put on the average gain in survival for the whole group of patients and insufficiently takes quality of life into account. Similarly, the Dutch association of Medical Oncology supports re-assessments, but is critical of this one due to the methodology used by the studies on which the re-assessment is based, which, in their opinion, fall short from a qualitative perspective.

Authors

References

Zorginstituut Nederland. Herbeoordeling PARP remmers [Re-assessment of PARP inhibitors], Diemen, June 2025

NOS nieuws. Zorginstituut schrapt dure kandermedicijnen uit pakket, “ze zijn niet effectief” [Dutch Healthcare Institute removes expensive cancer medicines from basic benefits package, “they are not effective”. https://nos.nl/artikel/2571550-zorginstituut-schrapt-dure-kankermedicijnen-uit-pakket-ze-zijn-niet-effectief, accessed 26 June 2025

IKNL. Zorguitgaven kanker stijgen vooral door nieuwe behandelingen [Healthcare expenditures increase mainly because of new treatments] https://iknl.nl/nieuws/2025/zorguitgaven-kanker-nieuwe-behandelingen

3.3.3. Collection

Health care in the Netherlands is mainly financed through insurance premiums and contributions under the Zvw and the Wlz (72%), and to a limited extent by general taxes (13%, figures for 2013). In 2015 the share of tax-financed care increased significantly compared to the previous years, as part of long-term care and youth care were transferred to the municipalities.

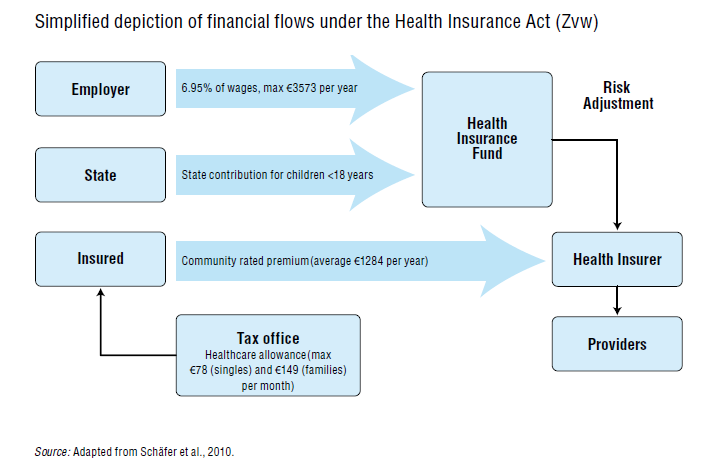

Income-dependent employer contributions under the Zvw are collected by the Tax Office, which levies the contribution from a person’s salary together with payroll taxes. The contributions and taxes are paid directly to the Tax Office by the employer. In 2015 the income-dependent contribution amounted to 6.95% of income (with a ceiling of €3573 per year) for employees and social security recipients. For self-employed persons, the income-dependent contribution is based on the tax assessment of their income. For self-employed persons the contribution in 2015 was 4.85% of income (with a ceiling of €2494 per year). The different rates for employees and self-employed persons reflect the fact that employers and social security institutions pay the income-dependent contribution, thus lowering the taxable income of the employee, whereas self-employed persons have to pay this contribution themselves. The lower rate and ceiling therefore seek to alleviate the financial burden on self-employed persons (Ministry of Social Affairs and Employment, 2012). After collecting all the contributions, the Tax Office transfers the collected funds to the Health Insurance Fund (Zorgverzekeringsfonds), from which the money is allocated after risk adjustment to the health insurers.

The premiums are collected directly by the health insurer where the health plan is purchased. Health insurers are free to set the community-rated premium level. The average premium was estimated by the Ministry of Health to be around €1211 per year in 2015, approximately 5% of a net “modal income” (defined by the Netherlands Bureau for Economic Policy Analysis (Centraal Planbureau, CPB) as gross €33 000 per year) for 2014 in the Netherlands. In 2015 the premium varied from €990 to €1300. For children below the age of 18, the government covers the premium through a contribution from general revenue into the Health Insurance Fund.

Insurers are not allowed to vary the premium of one specific health plan for different groups of people. There is one exemption: insurers may offer collective contracts. Collective contracts are established between groups of insured (for example, employees of the same employer) and the health insurer. Insured people are free to join a collective health plan or buy an individual plan. Health insurers are allowed to offer a maximum of 10% reduction on the individual premium. Collective arrangements can be made by several legal bodies such as employers and patient organizations. This system is established to give the insured more influence (“voice”) with the health insurers. The threat of the loss of a large number of insured persons may persuade insurers to satisfy the members of the collective contract and compete on price and quality of care. In addition, successful negotiations may lead to more demand-driven care and care that is tailored to the needs of the target group of the collective (Groenewegen & de Jong, 2007). In 2015, 69% of insured persons participated in a collective insurance policy (Vektis, 2015).

To cover expenses arising from the Wlz, a contribution of 9.65% is levied on the salary of citizens, with a maximum of €3241 per year (2016). This contribution is collected by the Tax Office. The revenues are transferred to the Long-term Care Fund, administered by the ZiNL.

Direct taxes are mainly levied from income tax, while indirect taxes mainly consist of VAT. Income tax is progressive. For VAT, there is a high tariff (21% in 2015) and a low tariff (6% in 2015, mainly for food, books and some services). All taxes are collected by the National Tax Office and are not earmarked for health care. From general revenue, the government (1) contributes to the Health Insurance Fund to provide children under 18 with coverage under the Zvw; (2) pays the health care allowance to households that are eligible and have filed an application (through the Tax Office); and (3) transfers funds to the municipality fund. The latter is used to cover the cost of decentralized long-term care under the Wmo 2015 and Youth Acts.

3.3.4. Pooling of funds

The Ministry of Health decides upon the national budget for health care. The Health Care Budget (Budgetair Kader Zorg, BKZ) indicates the maximum allowed health care expenditure. If providers and insurers spend more, the Minister may decide to charge insurers or providers to repay the excess, for instance by tariff cuts or repayment of part of the overspending.

The Minister also decides upon the budget for both municipality-based decentralized health care and home nursing care. The municipality budget is paid into the municipality fund (which is broader than decentralized health care and covers about 90% of all expenditure by the municipalities). The budget of this fund is allocated over the municipalities, based upon certain indicators, such as the number of citizens, the physical size of the municipality and the number of people entitled to social security.

Basic health insurance under the Health Insurance Act (Zvw)

In the Netherlands administering and providing basic health insurance are delegated to private health insurers. These insurers are funded by the premium directly received from the insured and a contribution from the Health Insurance Fund, which pools the income-dependent employer contributions (collected by the Tax Office) and the state contribution (for example, to cover children under 18) (see Fig3.7). The allocation of funds among health insurers is based on the health risks profile of their insured population. The Health Insurance Fund and risk adjustment are administered by the ZiNL. The government sets the level of the income-dependent contribution, with the notion that, at national level, the total income-dependent contributions for adults should amount to approximately 50% of the total funding of basic health insurance, while the premiums should account for the other 50%.

Fig3.7

Risk adjustment is a tool the government uses to prevent risk selection in the provision of basic health insurance and to promote fair competition. Health insurers are not allowed to vary their premium because of health risks and are obliged to accept each person who applies for an insurance plan. Risk adjustment implies that health insurers receive financial compensation for insured persons with unfavourable risk profiles, for example the elderly, chronically ill and people who are incapacitated and have higher health costs. The idea is that it should make individuals with unfavourable risk profiles equally profitable customers as those in good health. Differences in the premium between insurers should reflect differences in efficiency rather than differences in the risk profiles of their respective insured population. Furthermore, more efficiently operating health insurers could lower their premiums and attract insured persons from less efficient insurance plans. The expected result is lower overall costs.

Ex ante risk adjustment

Each year all health insurers receive from the Health Insurance Fund a risk-adjusted contribution, in the form of risk-adjusted (weighted) capitation payments. The risk-adjusted contribution from the Health Insurance Fund is calculated as the insurer’s total estimated health expenditure based on the risk profiles of their insured population minus the estimated income from their premium based on the calculation premium (rekenpremie) and the estimated income from the mandatory deductible. The calculation premium is a virtual premium used in the calculation for the national budget for health, welfare and sport (Rijksbegroting Volksgezondheid). If the individual premium levels were to be used for the calculation instead of the calculation premium, it could be an incentive for insurers to set a lower premium in order to receive a higher contribution from the Health Insurance Fund. Furthermore, even though only 50% of the funds are pooled, the risk adjustment is thus calculated on the basis of 100% of funds.

The risk-adjustment contribution is an ex ante system that is based not on real expenditure but on expected expenditure. It is calculated by means of risk-adjustment factors (see Box3.1).

Box3.1

The risk-adjustment factors described above are based on statistical estimates of the health risks and the related costs under the Zvw of these individuals.

Ex post compensation

For curative somatic care, health insurers have been fully risk-bearing since January 2015. The previous compensation mechanism for cost variations has now been abolished, since the system of ex ante risk adjustment is considered to be sufficient and insurers have sufficient means to efficiently purchase care (Ministry of Health, Welfare and Sport, 2014b).

For outpatient curative mental care, the ex ante risk-adjustment system is still considered inadequate, therefore a bandwidth arrangement (bandbreedteregeling) limits the risk for health insurers. If the costs for mental care per insured person after applying the ex ante compensation mechanisms are more than €15 above the national average, any additional amount is compensated up to 90%. If these costs are more than €15 below the national average, the insurer has to pay back 90% of the difference up to that figure (amounts are valid for the year 2015). For long-term mental care, the ex ante mechanism is not functioning well. Therefore insurers will be compensated for 100% of the incurred costs. The Minister of Health intends to abolish these compensation mechanisms in 2017 (Ministry of Health, Welfare and Sport, 2014b).

For nursing care and personal care, the ex ante mechanism has proven even more problematic. Insurers do not have a good notion of the costs as they only became responsible for purchasing this care in 2015. The Minister introduced a bandwidth arrangement of ±€5 of the average costs while costs outside this range are compensated for to 95%. This mechanism is also scheduled to be abolished in 2017 (Ministry of Health, Welfare and Sport, 2014b).

Long-term care (Wlz)

The Wlz is funded from income-dependent contributions collected by the Tax Office from Dutch residents via employers. In addition, those individuals who receive long-term care are required to share in the costs. The total amount of cost-sharing depends on the individual’s income and is levied by the Central Administration Office (CAK). Both sources of funding are pooled in the Long-term Care Fund, which is administered by the ZiNL. The CAK then acts upon the payment order of the care offices. These regional offices have the statutory responsibility to purchase care for eligible patients, based on the intensity of care that is needed for their clients as assessed by the Centre for Needs Assessment (CIZ). Care offices are organized by the dominant health insurer in a given region, but this activity does not contribute to the profit or loss of a health insurer. This is discussed in more detail in section 3.7.1.

Social support and youth care

Care provided by municipalities under the Wmo and Youth Act is financed from general tax revenue pooled in the Municipality Fund. The government decides upon the amount allocated to this fund. The distribution over the municipalities is based on a number of characteristics of the municipality, such as the number of inhabitants, geographic size, and the number of persons entitled to social security. Municipalities are free to spend the budget according to their own insights. For social support (including domestic care) and youth care, at national level, an amount of €7.1 billion has been made available (Tweede Kamer der Staten-Generaal, 2014), which is about 10% of the total health care budget. Municipalities purchase care for their citizens who are eligible for youth care, social care and domestic care. Some municipalities cooperate with neighbouring municipalities to increase purchasing power. The municipalities receive their budget mainly from the national government via the Municipality Fund (36% in 2014) and targeted contributions (19%), while the remainder comes from local taxes (17%) and other sources of income (Association of Netherlands Municipalities, 2015). However, the contribution from the Municipality Fund is not earmarked; municipalities are free to spend their allocated budget as they see fit. This construction was chosen to maximize the freedom that municipalities have to set their own policies and to minimize red tape and administrative burden. Apart from the obligation for municipalities to provide care, central government does not impose any restrictions. As a consequence, municipalities differ in their needs assessments, which may lead to inequalities in access to care among citizens of different municipalities. Accountability for policy and implementation of the Wmo takes place primarily at municipal level.

3.3.5. Purchasing and purchaser–provider relations

The organizational relationship between purchasers and providers in the Netherlands is based on contracting. Health care providers are independent and are contracted by the health insurers. With regard to the purchasing of curative care (Zvw), health insurers have two major negotiation tools at their disposal when contracting with providers. These are (1) negotiating services with providers on the basis of volume, quality and prices; and (2) selective contracting. The use of these tools should result in the efficient purchasing of care. Selective contracting may only be used by health insurers if they comply with their duty of care: they have to purchase sufficient care for their insured. At least theoretically, these mechanisms would lead to the disappearance of low-quality care providers. Selective contracting started in 2009 with one insurance policy (de Zekur polis) that explicitly used selective contracting. Selective contracting only relates to medical specialist care. For regular GP care selective contracting hardly occurs. GPs agree on a contract with one health insurer (the preferred insurer) and ask the other insurers to use the same contract. Only for pay-for-performance and sometimes for integrated care activities the following insurers may decide not to agree with the preferred contract. Nowadays there are several budget policies that employ selective contracting. Insured people who visit non-contracted providers may have to pay about 20 – 50% of the hospital bill out of pocket. These budget policies, however, were anticipating the abolishing of the free choice of provider (Article 13 of the Zvw). Jurisprudence has ruled that reimbursement should be at least 75% of the bill to ensure that the free choice of provider is not hampered by financial considerations. Late in 2015 the Minister of Health encouraged insurers to give a reduction on the mandatory deductible if contracted care is used.

Since 2013, contracting of hospital care is functioning as originally envisaged. There are two segments. The fixed segment relates to care that is considered not feasible or undesirable to be funded by free pricing (Hasaart, 2011). This is mostly complex care that is delivered by a low number of providers, such as transplantation care, or care that is difficult to plan, such as trauma care. Patients always get the care provided under the regulated segment reimbursed from their health insurer (except for the mandatory deductible). Care in the other segment (about 70% of hospital care since 2013) is freely negotiable. The percentage of freely negotiable hospital care was only 10% in 2006 and has increased gradually since. This was done to give insurers and hospitals time to adapt to their new roles in the negotiation process.

Each insurer negotiates with each hospital. Some insurers negotiate a lump-sum budget, others negotiate on price and/or volume for individual treatments. Individual treatment episodes are expressed in DBCs, which are also called care products. The DBC system is a variation on the DRG system. The NZa defines the DBCs. Since 2013, there are about 4400 DBCs. The free segment comprises care products for which negotiations are allowed. The care products for which the NZa establishes the prices are called the fixed segment. Before 2015, insurers negotiated separately with medical specialists and hospitals. Since 2015 hospitals negotiate with insurers on tariffs for the free segment while hospitals and medical specialists negotiate on the prices of care provided by medical specialists. Since there are hardly any reliable and mutually agreed quality indicators available, quality still plays only a minor role in negotiations.

The hospital has to publish a “walk-in tariff” for all DBCs in the free segment. These tariffs apply if patients receive care for which their insurer has no contract. If this walk-in tariff is higher than the tariff that the insurer of the patient has negotiated with their contracted hospitals, the insurer may charge the patient for the difference. The above applies only for patients with a health plan that provides health care in-kind. For patients with a health plan where they receive restitution of their care expenditure, all provided care is reimbursed (see section 3.4).

Although GPs prefer to negotiate in groups to increase their leverage with insurers, the ACM hitherto had not allowed this, arguing that GPs should compete with each other. However, since late 2015 the ACM allows cooperation that is in the interest of the patient (Consumers and Markets Authority, 2015). Since 2015, the standard contract for GPs also contains pay-for-performance elements but remunerating care innovations is still in its infancy (Dutch Healthcare Authority, 2015e). Furthermore, in 2015 GPs, health insurers, patient organizations and the Minister of Health agreed to decrease the administrative burden for GPs by reducing the number of quality indicators that should be reported to health insurers, as well as the number of authorizations for special medication and medical aids. Examples include: a prescription for a branded pharmaceutical instead of its generic equivalent now only needs the text “medically necessary”, whereas previously it required a written motivation and consent of the health insurer; contracts with insurers will become more uniform, and have longer duration (but with a yearly evaluation); and health insurers will no longer determine the type of medicine that should be used for a certain condition (Croonen, 2015).

For nursing care and personal care, the majority of the health insurers negotiate a budget ceiling with the providers. For most integrated dementia care, specific agreements exist on delivery, budget, tariffs and the way this care can be declared (Dutch Healthcare Authority, 2015c).

For long-term residential care, care offices negotiate with providers about the price and quality of care. The budgets for the management of care offices are set by the NZa and approved by the Minister of Health. There is no budget ceiling for provided care. For ambulatory long-term care, there is no contract obligation but care is granted to providers based on tenders organized by the municipalities. Criteria for granting care are quality indicators and the extent to which the price of care is under the maximum tariff for this type of care. For inpatient long-term care, the care offices are obliged to contract with the provider the patient has chosen. When patients receive a personal budget instead of care in-kind, they are free to purchase their own care (although payments are administered by the SVB). There are no formal quality requirements for care purchased via a personal budget.

In the Netherlands, health care consumers aged 18 and older must pay an annual mandatory deductible for all services and goods except GP-care, maternity care, and care for children under the age of 18. For the seventh consecutive year, since 2016, this deductible has been stable at €385 per year. Additionally, the personal contribution for prescribed medicines not fully reimbursed continues to be €250 maximum. The maximum annual health care allowance, which compensates for undesired income effects from health care costs in lower-income groups, has seen increases for both for single-person and family households, from €1336 to €1850 and from €2553 to €3166, respectively. These increases are more than the estimated average increase in insurance premiums and are considered a compensation for purchasing power. The income limit for health care allowances has also been raised, expanding eligibility. The maximum yearly income to be charged is €66,952. Meanwhile, the income-dependent contribution for health insurance under the Health Insurance Act has decreased from 6.75% to 6.68% for employees and those on social support. For entrepreneurs and pensioners, this contribution decreased from 5.50% to 5.43%.

Other important developments include that the average annual estimated community-rated premium for 2023 is €1649 and that the income-dependent premium for long-term care remains the same as the previous three years, at 9.65%. Lastly, insurers may no longer offer a discount (maximum 5.0%) on the basic insurance premiums for collective contracts, though collective discount on the voluntary insurance is still permitted.

There have been some changes to the basic benefits package so far in 2023.These include vitamin D being no longer included in the benefits package for vitamin D deficiency. Low-dosed vitamin D was already excluded in 2019 but now all types of vitamin D supplementation are to be paid out of pocket. In addition, pre-natal screening will no longer be performed via the combination blood test and neck skin fold measurement (nuchal translucency scan), but rather with a non-invasive Prenatal Test (NIPT). This test, as of 1 April 2023, will be covered fully with or without a medical referral, with no consequences for the mandatory deductible, though follow-up treatments may incur costs depending on the deductible. Previously, this test cost €175. Finally, the special regulation for paramedical care for long COVID patients was extended to 1 August 2023, on the condition that patients must be willing to participate in a study on the effect of this recovery care.

Authors

References

De NIPT | Prenatale en neonatale screeningen: https://www.pns.nl/nipt

Paramedische herstelzorg bij long covid tot augustus 2023 in basispakket: https://www.nationalezorggids.nl/zorgverzekering/nieuws/64429-paramedische-herstelzorg-bij-long-covid-tot-augustus-2023-in-basispakket.html