-

01 January 2023 | Country Update

Developments and changes in health care financing in 2023

7.2. Financial protection and equity in financing

In the Netherlands, health care consumers aged 18 and older must pay an annual mandatory deductible for all services and goods except GP-care, maternity care, and care for children under the age of 18. For the seventh consecutive year, since 2016, this deductible has been stable at €385 per year. Additionally, the personal contribution for prescribed medicines not fully reimbursed continues to be €250 maximum. The maximum annual health care allowance, which compensates for undesired income effects from health care costs in lower-income groups, has seen increases for both for single-person and family households, from €1336 to €1850 and from €2553 to €3166, respectively. These increases are more than the estimated average increase in insurance premiums and are considered a compensation for purchasing power. The income limit for health care allowances has also been raised, expanding eligibility. The maximum yearly income to be charged is €66,952. Meanwhile, the income-dependent contribution for health insurance under the Health Insurance Act has decreased from 6.75% to 6.68% for employees and those on social support. For entrepreneurs and pensioners, this contribution decreased from 5.50% to 5.43%.

Other important developments include that the average annual estimated community-rated premium for 2023 is €1649 and that the income-dependent premium for long-term care remains the same as the previous three years, at 9.65%. Lastly, insurers may no longer offer a discount (maximum 5.0%) on the basic insurance premiums for collective contracts, though collective discount on the voluntary insurance is still permitted.

7.2.1. Financial protection

The Dutch health care system obliges everyone living in the Netherlands to purchase basic health insurance. Health insurers in turn are obliged to offer basic health insurance at a community-rated premium, set by the health insurer, and cannot refuse any clients. In addition to this premium, Dutch citizens pay an income-dependent contribution (which is compensated by the employer).

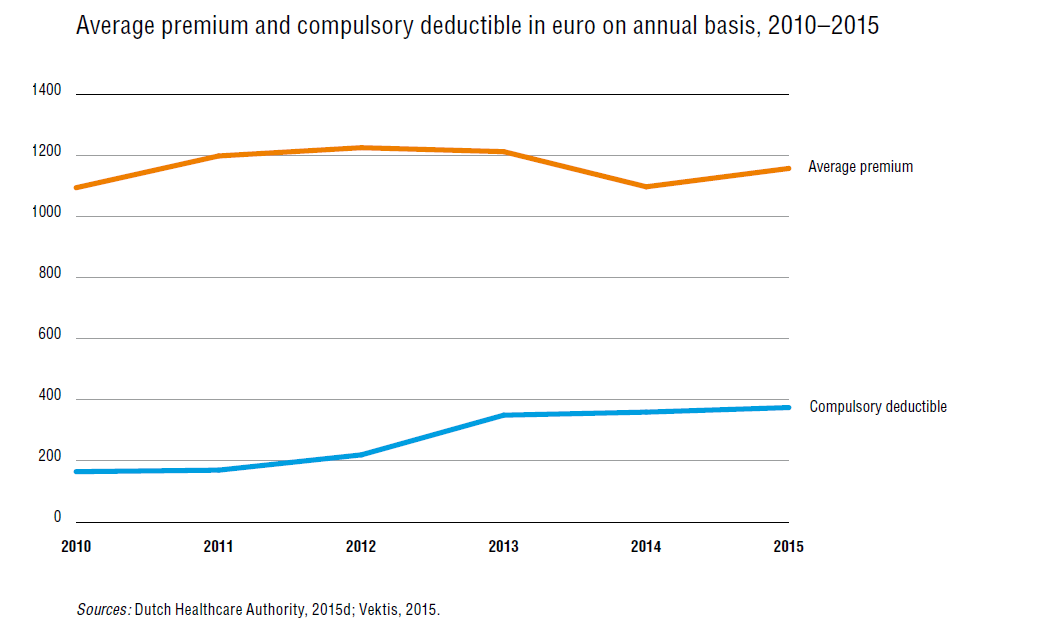

Health insurers offer different health plans, covering the same basic package but with different conditions and services. In most cases more expensive health plans offer greater freedom in choosing health care providers, whereas this choice is, in general, limited with the cheaper health plans. In 2014 the annual premium ranged between €905 and €1249. The difference in premium between the cheapest and the most expensive health plans has increased since 2013, due to an increase in cheaper health plans. On average, policy holders paid €1158 per year in 2015 (Dutch Healthcare Authority, 2015d). As shown in Fig7.1, after a relatively stable period the premium was lower in 2014 than in the preceding years, and increased slightly in 2015. Lower-income groups receive compensation for the premium through a care allowance. The level of the allowance depends on income. In 2015 the maximum allowance amounted to €936 for an individual and €1788 for a multi-person household. Slightly more than one-third (36%) of the population receive some allowance.

Fig7.1

In 2008 a compulsory deductible was introduced for all insured above 18 years of age. This deductible is set by the government and applies to all costs covered by the basic health insurance package, except general practice care, maternity care and home nursing care. This deductible increased over the years up to €385 per year for all individuals in 2016 (Fig7.1, figures until 2015). Chronically ill and disabled people are high users of care and services and are likely to have to pay the full deductible every year. Up to 2014, these groups were partly compensated for these costs. The level of the compensation was the difference between the average deductible paid by the chronically ill and the average deductible paid by non-chronically ill insured persons. This compensation was abandoned in 2014. Since 2014 people can apply for compensation and support at their municipality, based on the Wmo or the special support act. Municipalities have different policies towards the acknowledgements of such applications.

Since 2015, long-term care expenditure has been covered by the Wlz; previously they were covered by the AWBZ. People who receive residential or community-based long-term care have to make monthly co-payments. These co-payments vary between €195 and €620 per month for residential care and €19 per month for community-based care (Dutch Healthcare Authority, 2013). These co-payments have increased slightly through the years.

7.2.2. Equity in financing

From an international perspective, Dutch citizens have relatively low OOP expenses for health care services. According to an international comparison by the OECD, OOP health care expenses in the Netherlands were the lowest of all the countries studied, claiming 1.5% of total household consumption expenditure. However, this figure does not include the Dutch compulsory deductible, which is also an OOP expenditure. In 2010 this totalled about €1.4 billion (van Ewijk, van der Horst & Besseling, 2013), which would translate into an additional one-half percentage point. That would put the Dutch OOP expenses at around 2% of total household consumption expenditure, ranking the Netherlands between Germany and Japan, although still substantially below the OECD average, which is close to 2.9%.

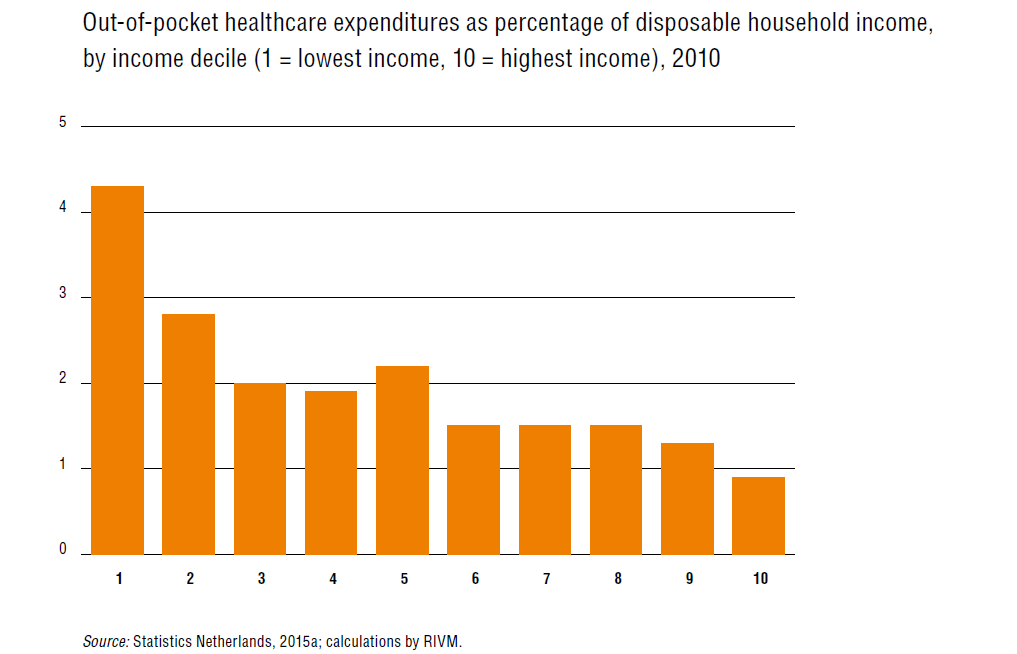

Higher income groups also have higher OOP expenditure in absolute terms, but lower in relative terms. Fig7.2 shows the percentage of financial burden on 10 disposable-income classes. Each class contains 10% of Dutch households, the first representing those with the lowest disposable incomes and the tenth those with the highest. In absolute terms, the tenth class has the highest average OOP expenditure (just under €1350 per household per year), whereas the first group has the lowest expenditure (just under €450). This amounts to respectively 4.3% and 0.9% of the disposable household income. From 2006 to 2010 a slight increase in the percentage of the burden is observable in the lower income classes but not in the higher ones (van den Berg et al., 2014a).

Fig7.2

Those in the lowest income groups with OOP expenses include many old people in residential and nursing homes and people with disabilities living in institutions. These individuals may spend a substantial part of their income on OOP payments but they do not have any housing expenses, which makes up a substantial share of expenses in other groups. People living in residential homes with a partner at home pay lower OOP expenses. According to the International Health Policy Surveys held in 2010 and 2013, the percentage of Dutch adults that decided to forgo health care services (consultations, tests or treatments) one or more times because of the costs involved increased from 6% to 22% over this period (Faber, van Loenen & Westert, 2013; Schoen et al., 2013). In 2013 some 18% had skipped dental care. A recent study showed an increase in the percentage of people not following up a referral from their GP from 18% in 2010 to 27% in 2013 (van Esch et al., 2015).