-

29 May 2025 | Country Update

Expanded programme for human papilloma virus–related cancer prevention -

09 July 2024 | Country Update

HIV pre-exposure prophylaxis now covered by compulsory health insurance -

18 November 2021 | Country Update

Amendment of the Federal Law on Health Insurance to allow data exchange with cantonal authorities

3.3. Overview of the statutory financing system

The MHI system as outlined by KVG/LAMal is – at least to a certain extent – based on the concept of regulated competition (Enthoven, 1988). MHI companies compete in a highly regulated market by offering different MHI policies for a standard benefits package (section 3.3.1), which all residents have to purchase. MHI companies are not allowed to turn down applications from persons who want to purchase insurance and they may not make profits (or losses) from providing MHI. Excess earnings have to be reinvested in the company and must benefit the insured.

Resources are raised not only through MHI premiums but also through federal and cantonal taxes (see section 3.3.2). The Confederation plays a strong regulatory role (see section 2.8.1) in monitoring MHI activities and premium levels, in setting the framework for cantonal premium subsidies to low-income households (see section 3.3.3), and in determining the risk-adjustment mechanism (see section 3.3.3). Interactions between purchasers and providers (see section 3.3.4) are shaped by the corporatist tradition of collective contracts, and all providers that have been authorized by cantons (see section 2.8.2) are allowed to provide services reimbursable by MHI.

Pre-exposure prophylaxis (PrEP) is a preventive medication that reduces the risk of contracting HIV from sex by about 99% when taken as prescribed. It is recommended for individuals at substantial risk of HIV, such as men who have sex with men. As of 1 July 2024, PrEP is included in the compulsory health insurance coverage in Switzerland. This new policy aims to enhance the accessibility of PrEP as part of the National AIDS Program Strategy (NAPS), which targets the elimination of HIV and hepatitis B and C transmissions by 2030.

The Federal Department of Home Affairs (FDHA) will assess whether covering PrEP costs under compulsory health insurance is effective, appropriate, and economically viable. The evaluation, running until December 2026, will determine if PrEP should be permanently included in the list of treatments covered by health insurance.

During this evaluation period, only providers affiliated with the SwissPrEPared network and authorized as service providers under the compulsory health insurance system will be able to bill PrEP costs through health insurance. This ensures that the implementation and impact of the policy can be closely monitored and analyzed. Individuals are still able to pay for PrEP themselves.

Authors

References

1. Medical Guidance – SwissPrEPared. Accessed 8 July 2024. https://www.swissprepared.ch/en/medical-guidance-2

2. HIV-PrEP|Swiss AIDS Federation. Accessed 8 July 2024. https://aids.ch/en/safer-sex/protection/hiv-prep

3. FOPH FO of PH. National programme (NAPS): Stop HIV, hepatitis B and C viruses and sexually transmitted infections. Accessed 8 July 2024. https://www.bag.admin.ch/bag/en/home/strategie-und-politik/nationale-gesundheitsstrategien/nationales-programm-hiv-hep-sti-naps.html

4. PrEP: cost coverage by health insurance|Swiss AIDS Federation. Accessed 8 July 2024. https://aids.ch/en/knowledge/topics/prep-cost-coverage

On 17 November 2021, the Federal Council designated the Federal Department of Home Affairs (FDHA) to conduct a consultation on the amendment of the Federal Law on Health Insurance (KVG) on data exchange and risk compensation. The amendment aims to facilitate the electronic data exchange between cantons and health insurers (for example, place of residence) to allow cantons to monitor compliance with compulsory insurance. Under current law, insurers can only obtain information from the cantonal authorities under restrictive conditions. This exchange of data will make it possible to determine the cantonal share of hospital services and avoid cases of double insurance. Moreover, persons residing outside the country but subject to compulsory health insurance in Switzerland are also to be included in the risk equalization, and persons with whom the insurers have not been able to make contact for some time should be excluded.

The amendment of the KVG is not yet definitively decided. The draft was revised and adapted based on comments from the consultation. The Federal Council’s decision for vote in Parliament will be taken in spring 2023 at the earliest.

Authors

References

Federal Office of Public Health. (2021). Änderung des KVG: Datenaustausch, Risikoausgleich [Modification of the KVG: Data exchange, risk compensation]. https://www.bag.admin.ch/bag/de/home/versicherungen/krankenversicherung/krankenversicherung-revisionsprojekte/modification-lamal-donnees-cdr.html (last accessed: 18.11.2021).

Federal Office of Public Health. (2021). Bundesrat will elektronischen Datenaustausch zwischen Kantonen und Krankenversicherern vereinfachen [Federal Council wants to simplify electronic data exchange between cantons and health insurers]. https://www.bag.admin.ch/bag/de/home/das-bag/aktuell/medienmitteilungen.msg-id-85923.html (last accessed: 18.11.2021).

Federal Office of Public Health. (2021). Änderung des Bundesgesetzes über die Krankenversicherung (Datenaustausch, Risikoausgleich). Erläuternder Bericht zur Eröffnung des Vernehmlassungsverfahrens. Bern. https://www.bag.admin.ch/bag/de/home/versicherungen/krankenversicherung/krankenversicherung-revisionsprojekte/modification-lamal-donnees-cdr.html

3.3.1. Coverage: everybody is covered but there are limitations in scope and depth

Breadth: Who is covered?

All permanent residents are legally obliged to obtain coverage by purchasing an MHI policy. Cantons are responsible for the enforcement of the law and they have to subsidize insurance premiums for persons who would otherwise be unable to pay their premiums. Individuals who refuse to take out MHI are assigned to an MHI company by the cantonal authority.

Since 2012, if individuals fail to pay their premiums, MHI companies can request cantons to pay 85% of the unpaid premiums and other debts (as identified by MHI companies) on behalf of the insured. This change was introduced to ensure that all residents have valid insurance coverage and can receive care. However, cantons can make lists of individuals with arrears, which are sent to public (cantonal) providers, and MHI companies will reimburse only emergency care provided to blacklisted patients. According to data of the FOPH (2014k), more than 100 000 people had arrears on their premiums in 2013, a number that had increased by around 10% every year in the past. Once insured defaulters have repaid their debts, full coverage is provided again, and MHI companies have to reimburse 50% of the repaid debts to cantons.

New residents are obliged to obtain insurance within three months of their arrival in Switzerland, which is then applied retroactively to the date of arrival. Since only individuals with valid residence of more than three months can take out MHI policies, the problem of undocumented immigrants remains unresolved (see section 5.14). However, in general, non-Swiss citizens are always treated in an emergency; the issue of who pays for the service only arises afterwards. If a resident of an EU country needs medical care in Switzerland, care is reimbursed according to EU regulations and agreements (see section 2.9.6).

Scope: What is covered?

All members of MHI have access to a standard benefits package. The content of the package is broadly defined by the KVG/LAMal as those services that are necessary for the diagnosis or treatment of a disease and its consequences as well as maternity services, on condition that these services are effective, appropriate and cost-effective (Art. 32 KVG/LAMal). Accidents are also covered under MHI except if individuals opt out because they are already covered under mandatory UV/AA (see section 3.6). The exact content of the benefits package is specified by the federal government in several explicit positive and negative lists (see section 2.8.1).

In practice, MHI covers most GP, chiropractor, midwife and specialist services, as well as inpatient care and an extensive list of pharmaceuticals, medical devices for home use by patients, laboratory tests and physiotherapy, speech therapy, nutritional counselling, diabetes counselling, outpatient care by nurses and occupational therapy (if prescribed by a physician). A contribution for costs of transport or rescue is paid. Psychotherapy services of nonmedical professionals (e.g. psychologists) are covered only if prescribed by a qualified specialist and provided to patients in the specialist’s practice. Long-term care is covered only if it is “medically necessary”. Dental care is covered only if it concerns a serious non-preventable illness of the masticatory system (e.g. maxillofacial cancer) or if it is related to care for other diseases (e.g. leukaemia or AIDS). Some prevention and screening measures are covered on the basis of a positive list, which includes pap smears, HIV tests, colonoscopies, mammography screening, genetic counselling and selected vaccinations.

MHI coverage gives preference to services provided in the canton of residence. However, in case of medical need, MHI also covers outpatient and inpatient services provided in a canton other than that of residence. In 2012, the territorial clause for inpatient services (use hospitals inside the canton) for inpatient acute care services was abolished. Since then, patients are free to choose their preferred hospitals in other cantons as well, but may have to pay the difference between the costs in the canton of treatment and those that would have been reimbursed in their canton of residence (see sections 3.7 and 5.4.2). Therefore, residents continue to purchase VHI for nationwide coverage of inpatient care.

As mentioned above, all goods and services covered by MHI should be effective, appropriate and cost-effective. Pharmaceuticals, medical devices for home use by patients and laboratory investigations are covered only if they are included in one of four explicit “positive lists”, which are determined by the FDHA or the FOPH after consultation with different advisory commissions responsible for the appraisal of new products (see sections 2.8.4 and 2.8.5). However, as positive lists cover only a minority of services, most covered services (i.e. those provided by physicians and chiropractors) are not formally assessed. Consequently, many services included in the benefit basket potentially have little scientifically proven value.

A particularity of the Swiss system is that, due to a popular referendum, since 2012 certain forms of CAM have been included in the standard benefits package if they are offered by medical doctors. This includes anthroposophic medicine, homeopathy, phytotherapy and pharmacotherapy of traditional Chinese medicine, which are provisionally covered until the end of 2017, when an evaluation will have to determine whether these methods are effective, appropriate and cost-effective, and warrant permanent inclusion in the MHI benefits package (see section 5.13).

The KVG/LAMal also explicitly or implicitly excludes a number of services from the standard MHI benefits package, some of which are covered in other countries, such as Germany and France. The most important categories of excluded services are:

- routine dental care: dental check-ups (except those provided for children in schools), fillings and extraction, dentures not related to congenital malformation or special diseases;

- monetary sick leave benefits (sick pay), which is not included in the standard benefits package although all MHI companies are mandated to offer complementary insurance for sick pay;

- long-term care costs going beyond a list of defined services;

- psychotherapy provided by nonmedically qualified practitioners;

- vision aids were excluded from the benefits package in January 2011 except for children and for adults with severe impairment of eyesight;

- in-vitro fertilization; and

- plastic surgery not related to accidents, disease or congenital malformation.

In addition, some services and goods are only partially financed by MHI. These include:

- medical aids;

- transportation and emergency rescue services; and

- therapies in thermal baths.

Complementary coverage for all excluded services can be purchased either from MHI companies or from other VHI companies (see section 3.5). However, a large part of the population pays for these services out of pocket.

Depth: How much of benefit cost is covered?

All health care services in Switzerland, such as GP visits, specialist visits, prescription drugs and stays in hospital, require cost-sharing in the form of user charges (see section 3.4.1 for details). Most importantly, all MHI contracts require a minimum annual deductible of Sw.fr.300 (about €280) per adult (and insured may opt for higher deductibles in exchange for lower premiums). In addition, a 10% co-insurance rate applies to all health care services and patients have to pay Sw.fr.15 (about €14) per day during inpatient stays on top. However, exemptions for children exist and co-insurance is capped for adults at Sw.fr.700 (about €654).

3.3.2. Collection: taxes and premiums vary across cantons and MHI companies

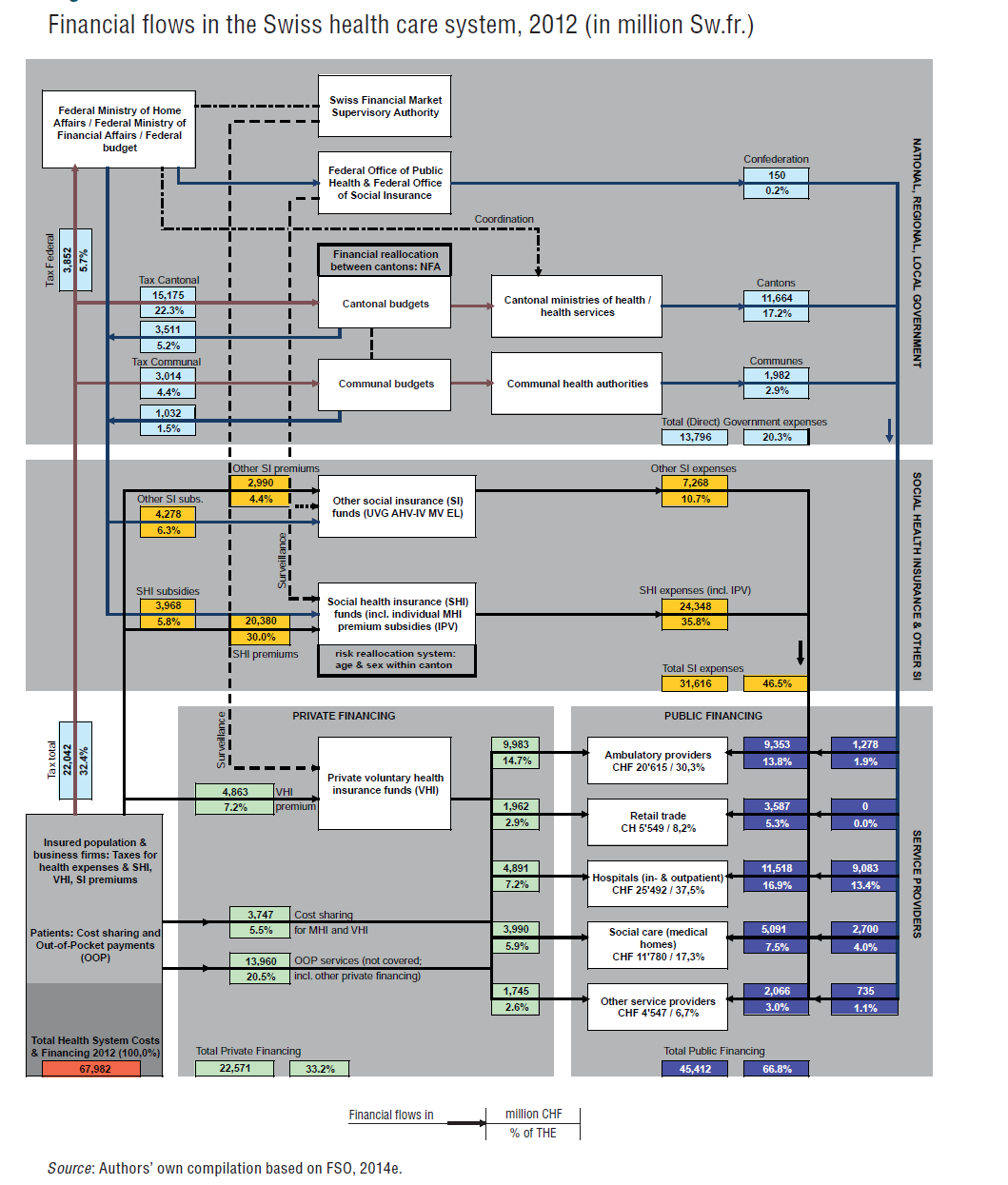

Public expenditure on health stems from two main sources in Switzerland (see left-hand side of Fig3.5):

Fig3.5

- General taxes raised by federal, cantonal or municipal governments (32.4% of THE); and

- Premiums paid either by MHI policyholders (30.0% of THE) or by holders of other social health-related insurance (6.2% of THE, see section 3.6).

Federal, cantonal and municipal taxes

According to the Federal Constitution, each level of government, i.e. the Confederation, the canton and the municipality, is entitled to levy taxes on individuals and corporations living or operating in their territory. In addition, each level is free to set the rate of tax and to decide on its use, which implies that tax rates and spending differ considerably across Switzerland. For the federal level, VAT and the direct federal tax (a combination of income and corporate tax) are the two most important sources of revenue. For the cantons and municipalities, income tax and property tax on individuals and corporations make up the largest share of their revenues. The direct federal tax as well as income and property tax in most cantons are progressive, implying that a higher tax rate applies to individuals with higher income or more property. However, large differences exist concerning the level of progressivity in each canton.

MHI premiums

MHI companies collect the bulk of their resources through community-rated premiums from their insured individuals. Community rating implies that premiums have to be the same for each person taking out insurance with a particular MHI company within a canton or subregion[2] of a canton independent of gender or health status of the insured person. Premiums are allowed to vary only by three age categories, with progressively higher premiums, for children (0–18 years), young adults (19–25 years) and adults (26 years and above). In addition, premiums are allowed to vary depending on the size of the deductible and for special managed care insurance models. Finally, individuals covered by mandatory UV/AA (see section 3.6) can receive a premium reduction. Premiums can be up to 50% lower in higher deductible plans, 50% being the legally defined upper limit for all deductible levels since 2010.

For 2015, the FOPH has estimated that the median monthly premium in Switzerland for adults with minimum deductible (Sw.fr.300), standard insurance model, and accident coverage, was Sw.fr.406, with 5% of adults paying more than Sw.fr.529 and 5% paying less than Sw.fr.328 per month (FOPH, 2014k). Premiums often vary significantly between different MHI companies within one premium region. Insured persons may change MHI companies and policies in order to pay lower premiums or to obtain better conditions (more choice, better coordination, lower deductibles, etc.).

MHI companies calculate their premiums based on estimates of effective (i.e. after correction of risk adjustment payments) average health care expenditure of people insured with a particular MHI policy in a particular canton or subregion of a canton. This means that cross-subsidization (or pooling) across cantons and across MHI policies is prevented. Premiums proposed by MHI companies are monitored by the FOPH and companies may have to change their premiums if they are found to be either too high or too low (see section 2.8.1).

- 2. The federal authorities define within every canton a maximum of three different premium regions. However, 15 cantons have only one premium region (AG, AI, AR, BS, GE, GL, JU, NE, NW, OW, SO, SZ, TG, UR, ZG); six cantons have two premium regions (BL, FR, SH, TI, VD, VS); and five cantons have three premium regions (BE, GR, LU, SG, ZH). ↰

3.3.3. Pooling of funds: the MHI market, premium subsidies and risk adjustment

MHI companies pool resources that they receive either from their insured (premiums) or from cantons on behalf of insured with low incomes (premium subsidies). As health care financing decisions are made by multiple different actors, i.e. the Confederation, cantons, municipalities, MHI companies and other SI, as well as by residents purchasing MHI and VHI or buying health goods and services, an overall budget for the health care system does not exist. Instead, the total national health care budget is the result of individual decisions and not the result of national (e.g. federal government) planning priorities. The only budgets that exist are those set by cantons for direct subsidies to providers – but even these are indicative budgets rather than hard budgets. Consequently, overall budget control is relatively weak.

For the functioning of the MHI system, three characteristic features are particularly important: (1) the MHI market structure, which provides a high level of choice to residents; (2) the subsidization mechanism, which supports low-income households for the purchase of MHI; and (3) the risk-adjustment and redistribution system, which aims to reduce the incentive for MHI companies to select good risks (the healthy and the young).

MHI market structure and developments

Swiss residents have a lot of choice of MHI companies and MHI plans despite a considerable reduction in the number of companies over the past few years. In 2013, there were 61 MHI companies operating in the country with each company offering several plans (FOPH, 2014k). Most MHI companies offer insurance with the statutory minimum (ordinary) deductible of Sw.fr.300 and insurance with a higher (optional) deductible of up to Sw.fr.2500 in exchange for lower premiums. Some MHI companies offer managed care type arrangements, where insured agree to use only designated providers. Finally, a small number of MHI companies offer bonus insurance, where individuals who do not make a claim in a particular year can obtain a premium reduction in the following year. As premiums differ across cantons, this variety led to a total of 287 000 different insurance premiums in Switzerland (FDHA, 2013).

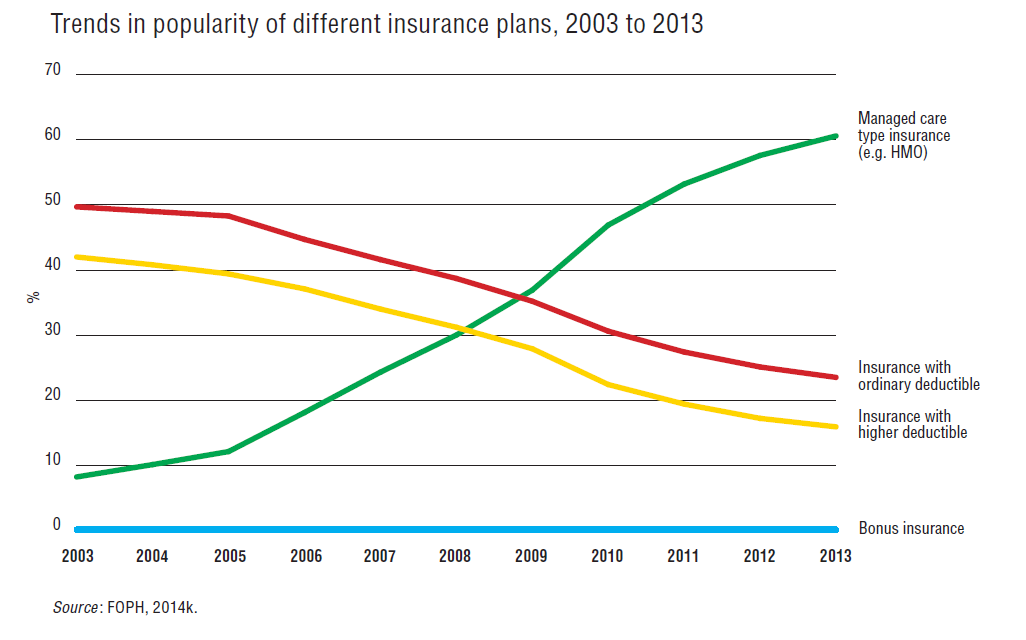

Since 2003, the MHI market has undergone an impressive transformation, with an increasingly large proportion of insured opting for managed care type insurance (see Fig3.8). By 2013, more than 60% of insured had managed care type insurance, while this proportion was below 10% in 2003. However, managed care type insurance plans may in fact be combined with higher (optional) deductibles and 34.3% of insured with managed care type insurance plans had an optional deductible, which is not reflected in the figure.

Fig3.8

Insured are allowed to switch their MHI company and/or their plan either on 1 January or 1 July. After the annual publication of updated MHI premiums at the end of September, insured have to notify their company by 30 November in order to switch by 1 January (FOPH, 2014m). If insured want to switch the MHI company during the summer, they have to inform their MHI company by 31 March (i.e. with three months’ advance notice). However, switching in summer is possible only for insured with ordinary deductible, but not for those with managed care type contracts.

Switching rates in Switzerland are estimated to be around 5–10% (FOPH, 2014k) per year which is comparable to (or slightly above) those in other countries with multiple insurance funds, e.g. the Netherlands and Czech Republic (Paris, Devaux & Wei, 2010).

A downside of the extensive choice of insurance is that the pooling of good and bad risks is relatively limited. With a high number of MHI companies in 26 cantons and even more (42) premium regions for 8.2 million people (2014), the insurance market remains fragmented into small risk pools. Pooling is limited to the cantonal level (or even to the subcantonal premium region) because MHI companies have to calculate premiums based on the insured living within a particular canton (or premium region).

Fragmented risk pools are problematic because they complicate cross-subsidization between the healthy and the sick. Most risk-adjustment systems (including the one in Switzerland, see below) can not at all achieve complete risk equalization across risk pools and, consequently, it remains profitable for MHI companies to select good risks. The persisting large variation in premium levels for similar MHI policies within the same canton is largely related to risk selection and insufficient pooling. In addition, the complexities of designing and offering thousands of different insurance policies within one canton increase administrative costs of the MHI system as well as the search costs for citizens.

Premium subsidies for low-income households

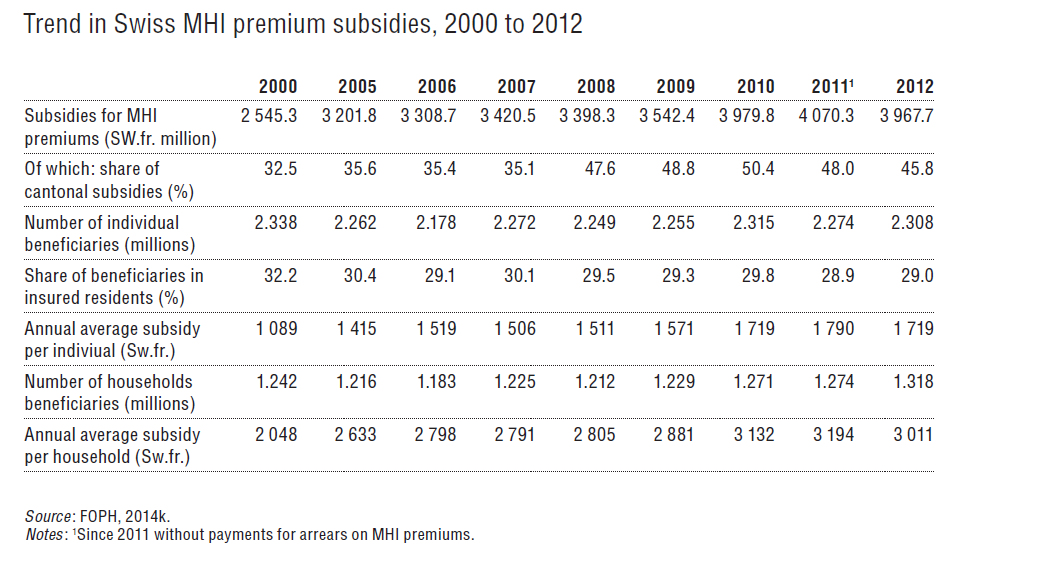

In 2012, a total amount of almost Sw.fr.4 billion was paid by cantons (with co-financing from the Confederation) for premium subsidies. The size of the federal contribution for premium subsidies is fixed at 7.5% of the estimated MHI (gross) costs in a given year, i.e. the sum of total MHI premiums and the cost-sharing payments of the insured. The federal contribution is distributed to individual cantons on the basis of population size. In order to receive federal subsidies, cantons must themselves pay a minimum amount. However, beyond this minimum amount, cantons are relatively free to choose the size of the cantonal budget available for premium subsidies. In 2012, premium subsidies amounted to SW.fr.3968 million (or 16.3% of total MHI revenues, see Table3.4), which were co-financed by the Confederation’s budget (54.2% of total subsidies) and by cantonal budgets (45.8%) but with large variation across cantons.

Table3.4

The number of individuals receiving premium subsidies and paying only a reduced premium or no premium at all has remained relatively stable at around 2.3 million, corresponding to 29.0% of the Swiss population in 2012 (see Table3.4). About 0.5 to 0.6 million people are estimated to pay no premium at all, although the exact number of persons or households is unknown.

Since 2011, premium subsidies are paid by all cantons directly to MHI companies. Eligibility criteria for subsidies can differ substantially between cantons, contributing to horizontal inequities in financing (see section 7.2.2). Some cantons fix the maximum contribution for individuals as a percentage of taxable income (for example, 10%), while other cantons define income classes with different fixed amounts of subsidies. Still other cantons apply a mix of these models or something else (for an overview of the 2012 cantonal systems, see Bieri and Köchli (2013)). For people on very low incomes, the entire premium or a cantonal reference premium, whichever is smaller, is paid directly by the municipal or cantonal authorities.

Only for children (≤18) and young adults (≤25) in training, premium subsidies have been somewhat standardized: cantons are mandated by law to reduce premiums for both groups by 50% for lower- and middle-income households. However, cantons can still determine the thresholds used to define lower- and middle-income. According to an impact evaluation of the subsidy policy, the remaining premiums paid by eligible individuals in 2010 amounted to between 5% and 14% of their income, depending on the canton and its eligibility criteria (Kägi et al., 2012).

Risk adjustment between MHI companies

MHI premiums are community-rated within cantons. However, the old and sick have higher costs than the young and healthy. Therefore, risk adjustment is necessary in order to compensate MHI companies for differences in the costs they face from the varying risk profiles of their insured. In the absence of risk adjustment, strong incentives would exist for MHI companies to engage in risk selection, i.e. to select those individuals for whom costs can be expected to be lower than premiums.

In Switzerland, MHI companies with insured people that are relatively healthier and younger (good risks) must pay into a common pool managed by the Common Institution under the Federal Health Insurance Law. The Common Institution redistributes funds to MHI companies according to the risk structure of their insured.

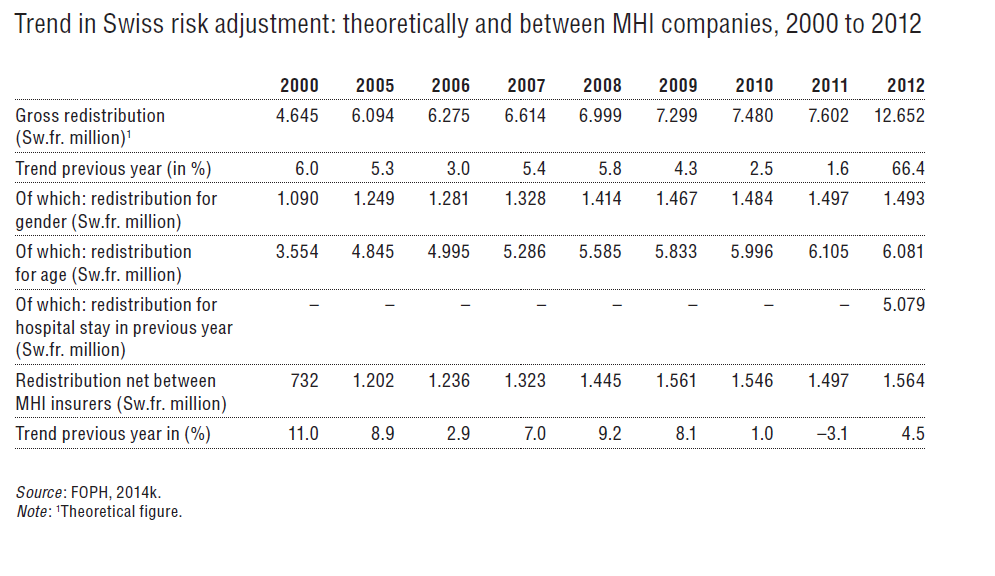

Until the end of 2011, the risk-adjustment formula was based only on age and gender. The formula consisted of 30 age and gender categories (15 age groups and 2 gender categories), and financial flows from the Common Institution to MHI companies ensured that available resources per insured person within one of these categories were the same across MHI companies operating within the same canton. However, it was generally acknowledged that risk selection was widespread under this “old” risk equalization formula (van de Ven et al., 2013).

Since the beginning of 2012, a revised formula also takes into account prior hospitalization (more than three consecutive nights spent in an acute hospital or nursing home in the past year). Table3.5 shows that this has considerably increased the (theoretical) gross redistribution amount. However, the net redistribution across MHI companies has not increased because redistribution takes place mostly within companies, since many companies have insurance plans with high risks and others with low risks. Nevertheless, because of the way in which premiums are calculated, the improved risk-adjustment formula will lead to lower premiums in insurance plans with higher-risk groups. Since 2014, the Federal Council has the right to further define risk-adjustment factors if necessary (see section 6.1.3). Starting in 2017, expenditure for pharmaceuticals exceeding Sw.fr.5000 in the previous year will be used as a fourth factor for risk adjustment.

Table3.5

3.3.4. Purchasing and purchaser–provider relations

MHI companies are by far the most important purchasers of health care services and goods. The second important group of actors on the purchaser side is the cantons, although their spending on health is – in particular since the transition to a DRG-based hospital payment system – mostly linked with MHI transactions. MHI companies and the cantons are rather passive purchasers, mostly reimbursing the bills of health care providers.

Regulatory framework

Collective contracts dominate the relationship between purchasers and providers. In fact, MHI companies are obliged to reimburse bills of all authorized providers (the so-called obligation to contract). Authorized providers are all those that fulfil the basic regulatory requirements for providing MHI-reimbursable services (see section 2.8.2). Consequently, direct competition between providers for contracts from MHI companies is limited. MHI companies can engage in selective contracting with physicians only in the case of managed care arrangements.

Conditions of reimbursement are specified by contracts negotiated between associations of insurers (santésuisse, curafutura, RVK) and providers (e.g. FMH for physicians), and tariffs have to be agreed upon by MHI companies and providers. Contracts become valid after approval by cantonal governments (in the case of cantonal contracts) or by the Federal Council (in the case of national contracts). If insurers and providers do not reach an agreement, tariffs can be fixed by the cantonal or federal authorities.

The tariffs for ambulatory care and, since 2012, also for acute inpatient care, are based on national frameworks (see section 3.7), developed jointly by associations of insurers and providers. For inpatient rehabilitation and inpatient psychiatry, work on developing national tariff frameworks is currently ongoing (Caminada et al., 2015). The actual level of reimbursement can differ between and within cantons, depending on cantonal or local negotiations. In theory, contracts should also include requirements for quality and efficiency in service provision as mandated by the KVG/LAMal (Art. 56 and 58). However, in practice, conditions for efficiency and quality are very rarely specified in detail and control mechanisms are almost non-existent.

A new provider intending to provide services reimbursable by MHI has to register with a subsidiary of santésuisse (SASIS AG), which is responsible for awarding new MHI billing numbers. When applying for such a number, SASIS checks whether new providers comply with the necessary conditions, i.e. if they are authorized by cantons for the provision of MHI-reimbursable services.

Ambulatory care

For physicians, the national fee schedule (TARMED) is developed by the corporatist institution TARMED Suisse (see section 2.3.6). TARMED determines not only the tariff structure but also defines training requirements (specialization, subspecialization, additional training certificates) that physicians have to fulfil in order to be allowed to bill for a particular service.

All physicians who want to provide MHI-reimbursable services have to join the national TARMED framework contract negotiated between FMH and santésuisse. This contract was originally concluded in 2003 and conditions for quality and efficiency were intended to be specified in an annex to the contract. However, by early 2015, an agreement had not yet been reached between insurers and physicians about how efficiency in service provision should be assessed.

The monetary value of a TARMED point is fixed in negotiations between, on the one side, the cantonal association of physicians for ambulatory practices or the H+ for hospital outpatient consultations, and on the other side MHI companies, i.e. tarifsuisse SA (negotiating for the majority of MHI companies) or curafutura. There are separate monetary values of TARMED points for medical practices and for hospitals in every canton. If the negotiating parties do not reach an agreement, the cantonal government can define the point value or base rate.

Cantons have the option to limit the number of new ambulatory providers (including independent practices, hospital outpatient departments and pharmacists) on the basis of a so-called necessity clause (see section 2.8.2). Current reform proposals aim to provide cantons with regulatory mechanisms for better management and planning of ambulatory service provision (see section 6.2.2).

Individual insurers may conclude selective contracts with physician networks or HMOs, which may specify conditions (e.g. quality management, bonuses, shared savings, etc.) that go beyond or are different from those of the collective contract. Nevertheless, if selectively contracted physicians bill FFS, they have to follow the national TARMED fee schedule.

Services from non-medics, e.g. physiotherapists, Spitex services, laboratory services, other paramedical and ambulatory services, are always reimbursed by MHI if prescribed by medical doctors. Again, collective contracts exist between insurers and providers, and point values for the applicable fee schedules are negotiated at the cantonal level or national level (e.g. chiropractors and ergotherapists) between professional associations and the associations of MHI companies. These contracts become valid after approval by cantonal governments (in the case of cantonal contracts) or by the Federal Council (in the case of national contracts). Payments for services not reimbursed by MHI companies are based on market prices.

Inpatient care

For acute inpatient care, which is jointly funded by cantons and MHI companies (see the actual shares of funding in GDK/CDS, 2014b), the national tariff framework (i.e. the DRG system) is developed by the corporatist institution SwissDRG SA (see section 2.3.6). Cantons are important actors for the purchasing of inpatient care as they determine through their hospital planning decisions (see section 2.5.2) which hospitals are allowed to provide which MHI-reimbursable services. Population needs and quality considerations are taken into account during the cantonal planning process. Hospitals have to apply in order to be included in the cantonal hospital lists, and cantons may decide not to include a hospital or to include it only for certain services.

DRG base rates are negotiated between individual hospitals or groups of hospitals and the associations of MHI companies. Subsequently, base rates have to be approved by the cantonal authorities, which can fix the value of the base rate if negotiating parties do not reach an agreement. Furthermore, the national Price Supervisor provides recommendations on appropriate base rates to be used in different cantons. If cantons approve base rates that are higher than those suggested by the Price Supervisor, they will be obliged to make their reasons known.

Efficiency and cost control

Currently, global budgets or volume limits exist neither for ambulatory care nor for inpatient care, although cantons have the legal option to define a global budget for expenditure control (Art. 51 KVG/LAMal). MHI companies have the right (Art. 59 KVG/LAMal) to sanction providers who do not comply with the requirements for cost-efficiency and appropriateness of care. Since 2004, santésuisse has used a method based on an analysis of variance (ANOVA) of practice costs in order to identify outliers. Practices exceeding average costs by more than 20% or 30% (after controlling for location, specialty, and age and gender of patients) are asked to provide additional information explaining their higher expenditure. In very few cases (less than a dozen cases a year), excess earnings have to be paid back and practices can in theory be excluded from future contracts. Because the method was highly controversial, an amendment to the KVG/LAMal in 2011 mandated santésuisse and providers to agree on a common methodology for cost-efficiency and appropriateness analyses. While santésuisse and FMH agreed in 2013 that these analyses should be based on ANOVA, a final decision has not yet been reached on the exact variables to be included.

Also for the inpatient sector, cost and efficiency control mechanisms are weak. Inpatient activity is not systematically monitored by MHI companies or cantons, e.g. to detect unwarranted increases in the number of treated cases. However, upcoding is controlled through a review mechanism, where independent reviewers review the coding of a random sample of patient files at hospitals (SwissDRG, 2009).