-

15 September 2023 | Policy Analysis

Complementary health insurance abolished -

05 December 2022 | Policy Analysis

Recent advances in financing of PHC services in Slovenia, 2017–2022

3.3. Overview of the statutory financing system

A central health policy of more than two decades was addressed this summer with the adoption of amendments to the Health Care and Health Insurance Act on 6 July 2023, which abolished the complementary health insurance (CoHI).

CoHI had been contested for various reasons by a large part of the political spectrum; however, many on the right and several experts remained unconvinced, stating that the CoHI was an important source of stable additional financing of health services. CoHI indeed bridged the gap in funding of compulsory health insurance during the austerity measures due to the financial crisis of 2009–2014.

The government has now decided to introduce a fixed compulsory contribution – currently €35 a month – that will be raised on all incomes by the Financial Administration (that is, IRS), starting 1 January 2024. The mechanism of potential future increases in this contribution seems more complicated than for the previous CoHI, and consequently, the Ministry of Finance will cover for potential “losses” on this insurance up to a total amount of €240 million. This limit was set according to EU regulations on containing public deficits.

What will happen with the insurance companies?

There are three CoHI companies. In real terms, only one, Vzajemna, is independent and covers almost exclusively CoHI. The others are subsidiaries or departments of larger insurance companies and represent one of the several items in their portfolios, including different types of supplementary insurances, mostly for queue skipping in outpatient specialist services and diagnostics. Vzajemna now faces a restructuring into a limited company. It is expected that the capital will be turned into shares and all the insured as well as the Health Insurance Institute of Slovenia, the single purchaser of public services, which has some funds invested, will become shareholders.

Challenges and issues?

One main concern about this new proposal is a gap in the offer of health services in the public sector, which is insufficient to meet the demand. This is coupled with poor incentives for (salaried) health professionals in the public sector, leading many to work either extra time or full-time with providers that mostly provide their services to the insured of the supplementary health insurance schemes. Further enhancement of these schemes could potentially challenge the equity of access, both in physical and economic terms.

References

Despite good health outcomes, a PHC model characterized by multidisciplinary teamwork, strong links to public health and universal financial coverage for health services, Slovenia’s PHC faces myriad challenges.

Demographic and epidemiological transitions, technological advances, and adjustments to service delivery have changed patient expectations and increased the demand for (longer) clinical visits at PHC for more complex patients. Meanwhile, personnel challenges hamper the PHC system’s ability to meet population needs and ensure quality and safety of care.

There is a shortage of PHC physicians: around 120,000 adults are not registered with a PHC team due to lack of capacity. This shortage is getting worse due to an ageing PHC physician population (about 30% to retire in the next 5-10 years) and difficulty in attracting/ retaining physicians because of, e.g., dissatisfaction with salaries, working conditions, and inadequate professional development and support. Consequently, existing PHC physicians face high workloads but are still expected to increase the services they provide.

Meanwhile, there isa twofold spillover effect. First, those without a primary provider use emergency care, which both overburdens the emergency care—itself lacking adequate staffing levels—and raises healthcare costs. Second, saturated PHC teams refer patients to secondary ambulatory care for treatment that could be managed at PHC given more capacity. This generates long waiting times for non-urgent hospital ambulatory care services.

Between

2017 and 2022, Slovenia introduced several piecemeal financial

interventions to immediate effect to address workforce challenges and

other tenacious issues plaguing PHC.

Project to shorten waiting times in hospital ambulatory healthcare and improve medical service quality at primary level (2017; €36 million)

- Publicly employed PHC providers can be remunerated additionally based on performance up to 25% of base salaries in family medicine and primary pediatric practice

- Dedicated funds are provided from the national budget, not from the health insurance institute (HIIS)

- Requires use of the newly introduced eHealth services

Decision for special programs on PHC (2019; approx. €9 million provided from the national budget of the RS)

- Introduces a scale awarding certain percentages of additional remuneration for exceeding the 1,895-capitation quotient in family medicine and primary pediatric practice

- Extends office hours by minimum 1 hour to ensure enough time for patients

Special government project on family medicine and primary pediatric practice (2021)

- Introduces shift of funding from national budget to HIIS and fee-for-service purchasing for all services provided that exceed the monthly plan

Measures to ensure healthcare system resilience (2022)

- Supplements

for healthcare employees at all levels introduced and financed from

state budget, e.g., for increased workload, and for working in

less-developed geographic areas and municipalities with a lower degree

of economic development

Together the measures established a new precedent for increased funding of healthcare services from the state budget. Evaluations have yet to be performed, but anecdotally family physicians seem better satisfied with their incomes since implementation. However, PHC performance isn’t improved and over 100,000 patients are still not registered with a PHC physician. Thus, the impact on waiting times and emergency care persist. Additionally, interest for PHC jobs among young physicians has not improved either.

Authors

References

Albreht T, Polin K, Pribaković Brinovec R, Kuhar M, Poldrugovac M,

Ogrin Rehberger P, Prevolnik Rupel V, Vracko P. Slovenia: Health system

review. Health Systems in Transition, 2021; 23(1): pp. i–188.

Act on emergency measures in the field of healthcare: Official Gazette of the Republic of Slovenia, no. 112/21 (http://www.uradni-list.si/1/objava.jsp?sop=2021-01-2452), 189/21 (http://www.uradni-list.si/1/objava.jsp?sop=2021-01-3726), 206/21 (http://www.uradni-list.si/1/objava.jsp?sop=2021-01-4283) – ZDUPŠOP and 132/22 (http://www.uradni-list.si/1/objava.jsp?sop=2022-01-3114). http://www.pisrs.si/Pis.web/pregledPredpisa?id=ZAKO8360.

Innovations

brought by the Act on emergency measures to ensure the stability of the

health care system. Slovene Medical Chamber. 21 July 2022. https://www.zdravniskazbornica.si/informacije-publikacije-in-analize/obvestila/2022/07/21/novosti-ki-jih-prina%C5%A1a-zakon-o-nujnih-ukrepih-za-zagotovitev-stabilnosti-zdravstvenega-sistema.

3.3.1. Coverage

Breadth: who is covered?

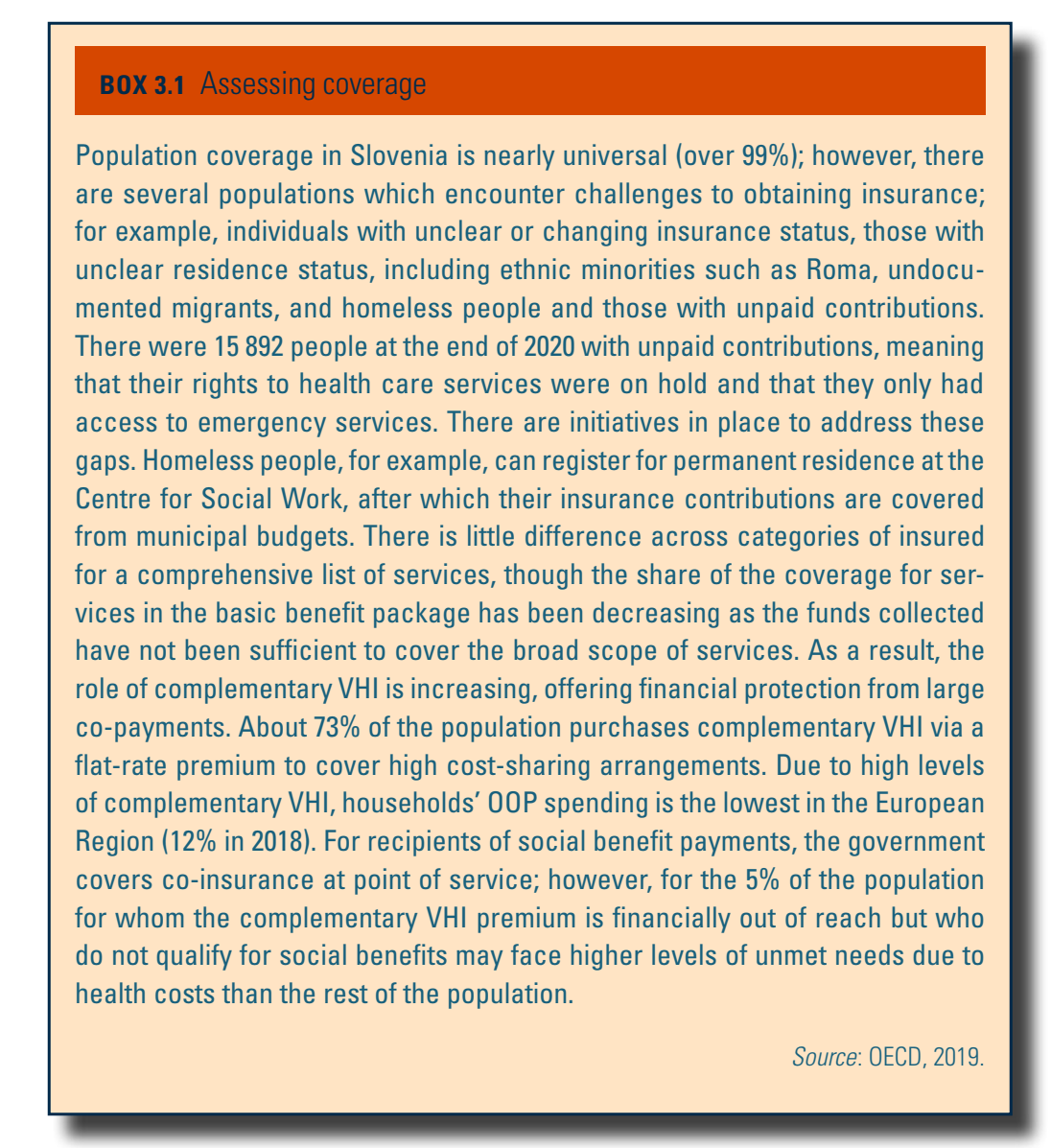

The centralized SHI system, administered by the ZZZS, is defined in the Health Care and Health Insurance Act (1992). Nearly every permanent resident in Slovenia is entitled to the health benefits covered under this scheme, as contributing members or as their dependants. Opting out is not permitted. Permanent residency is one of the main factors for entitlement to health services, but Articles 15–18 of the Act define additional conditions under which a person is compulsorily insured. Consequently, coverage is near universal, with 2 116 739 compulsorily insured individuals in 2019, representing more than 99% of the population and a slight decrease of 0.8% from 2018 (ZZZS, 2019). About 0.14% (3345) individuals were uninsured at the end of 2020. Most of these were temporarily uninsured; for example, awaiting recognition of the right to a pension or to unemployment benefits; the remaining were primarily individuals who cannot meet the formal residency requirements (e.g. undocumented migrants, ethnic minorities such as the Roma population and the homeless). In addition, 15 892 people at the end of 2020 are covered by SHI, but with unpaid contributions, meaning that their rights to health care services were on hold and that they only had access to emergency services (Box3.1).

Box3.1

There are 25 categories of insured people, divided into two main groups. Each category has a different contribution rate, but contributions are mostly income-based. The first group is employees (and their dependants) and the second group comprises the unemployed, others without fixed income but not registered as unemployed, pensioners, farmers and the self-employed. The National Institute for Employment covers contributions for the unemployed; the state and/or municipalities for individuals without income, prisoners and war veterans. For more information on the collection and pooling of compulsory health insurance contributions, see section 3.3.2.

SHI coverage is also provided to citizens of almost all EU countries through European regulation and bilateral agreements (see section 2.8.4). Specific provisions apply for certain vulnerable groups.

Scope: what is covered?

The Health Care and Health Insurance Act (1992) broadly defines the health services to be covered for the insured population. The benefits package comprises primary, secondary and tertiary services; pharmaceuticals; medical devices; sick leave exceeding 30 days; and costs of travel to health facilities. There are almost no differences in benefits between the categories of insured people; however, some specific benefits do not apply to all categories of insured people (e.g. retired people are not entitled to sick leave benefits and certain self-employed groups and farmers are not entitled to reimbursement for travel expenses).

Article 23, point 1 of the Act, delineates the following services to be fully covered by compulsory health insurance:

- all health services for children, and students up to age 26, including: diagnosis, treatment and rehabilitation of diseases and injuries suffered by children, schoolchildren, minors with developmental impairments and students for as long as they attend school;

- counselling in family planning, contraception, antenatal care and childbirth for women;

- services as part of the prevention, diagnosis and treatment of infectious diseases, including HIV infection;

- treatment and rehabilitation of occupational diseases or injuries, muscular or muscular nerve diseases, mental diseases, epilepsy, haemophilia, paraplegia, quadriplegia and cerebral palsy, as well as advanced diabetes, multiple sclerosis and psoriasis;

- medical services related to the donation and transplantation of tissues and organs;

- emergency health care services including ambulance transportation;

- mandatory vaccination, immuno- and chemoprophylaxis (programme-based);

- treatment and rehabilitation of malignant diseases; and

- long-term nursing care, including home visits and treatment in nursing homes and other social care institutions.

All other health care services involve cost-sharing through co-payments (see below for depth of coverage). For most areas of care, the Act does not provide a detailed list of services but mandates that co-payment levels for services be determined by the ZZZS in agreement with the government. To this end, the ZZZS issues the “Regulation of compulsory health insurance”, which must be accepted by the ZZZS Assembly and approved by the Minister of Health. Practically, this means that, although no services are explicitly excluded from public coverage by law, certain services, such as cosmetic surgery, can be eliminated in the “Regulation of compulsory health insurance”.

Depth: how much is covered?

For services not fully covered, compulsory health insurance will take on 10–90% of the cost, depending on the specific type of treatment or activity. Since the adoption of the Fiscal Balance Act in 2013, these shares are as follows.

A minimum of:

- 90% of the cost of services related to organ transplantation and urgent surgery, treatment abroad, intensive therapy, radiotherapy, dialysis and other urgent interventions included in the basic benefits package;

- 80% of the cost of treatment for reduced fertility, artificial insemination, sterilization and abortion; specialist surgery; nonmedical care and spa treatment in continuation of hospital treatment with the exception of non-occupational injuries; dental care and orthodontics; orthopaedics; hearing and other aids and appliances; and

- 70% of the cost of medications from the positive list (see sections 2.7.4 and 5.6); and for specialist, hospital and spa treatment of injuries that are not work related.

A maximum of:

- 60% of non-emergency ambulance transportation for paralysed people, and medical and spa treatment that is not in continuation of hospital treatment;

- 50% of the cost of ophthalmology devices and orthodontic treatment for adults; and

- 25% of the cost of pharmaceuticals from the intermediate list determined by the ZZZS.

As mentioned, most compulsorily insured individuals purchase complementary VHI to cover co-insurance (see sections 3.4.1 and 3.5).

3.3.2. Collection

General government budget

In Slovenia, SHI contributions are the largest source of revenue for health system financing (see section 3.2). They are regulated in the Health Care and Health Insurance Act (1992) and have remained unchanged since 2002. Contribution rates, which are employment-based and levied on gross income, vary by category and group of insured individuals (see section 3.3.1). Employees pay 6.36% of their gross income, while employers pay 6.56% for illness and injury out of work, plus 0.53% for injuries at work and occupational diseases (in total, 13.45% of gross income is collected per insured person). The contribution rates are the same for self-employed, though their contribution base is equal to the gross pension base but cannot be lower than 60% of the last-known average annual wage (ZZZS, 2019; 2020). The National Institute for Employment covers contributions for the unemployed and the state and/or local budgets cover contributions for individuals without income, prisoners and war veterans. The Pension and Disability Insurance Institute pays contributions for pensioners (at a 5.96% contribution rate from pensions) via a monthly transfer (90% financed from salary contributions and 10% from the general budget) to the ZZZS.

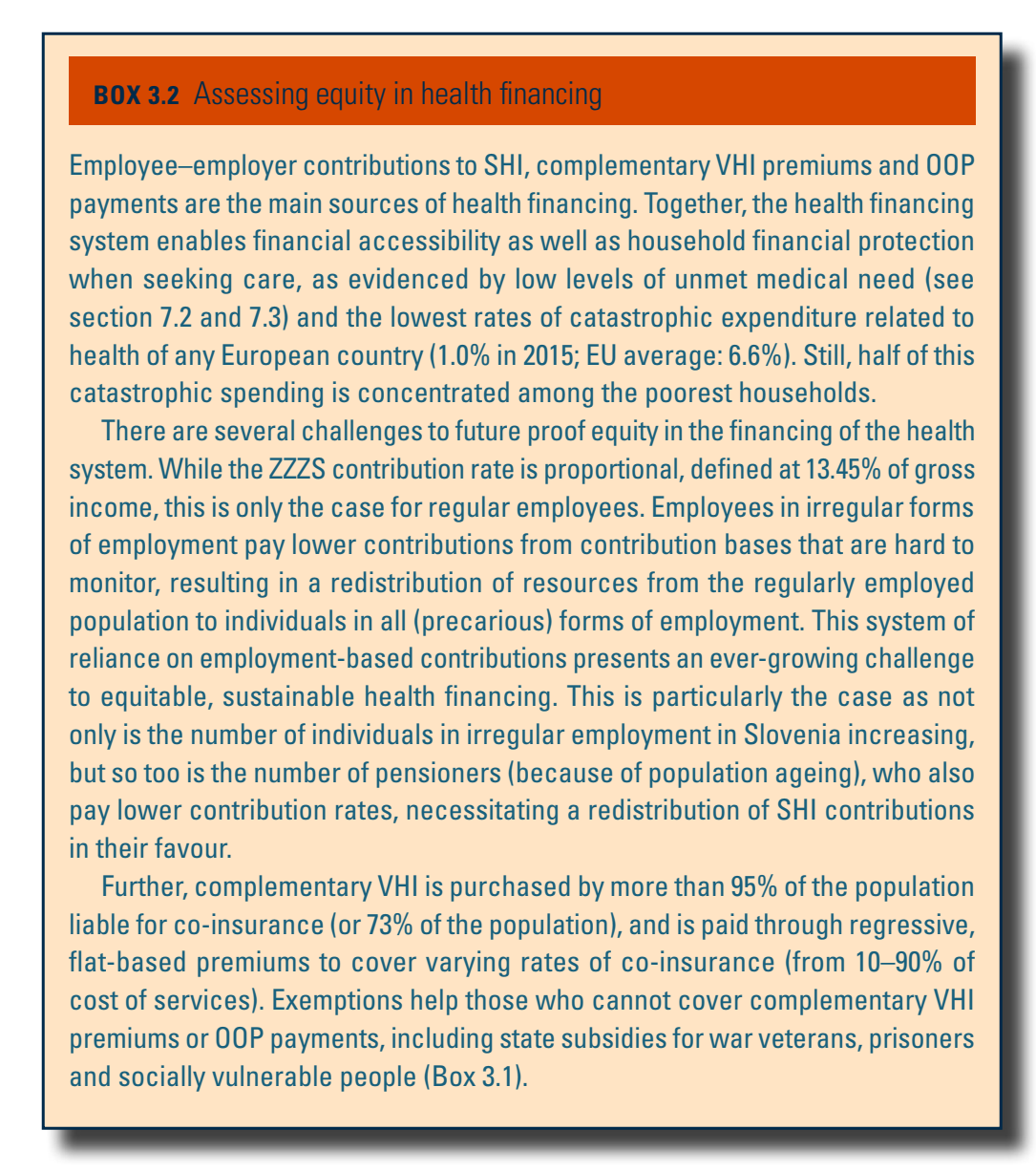

The ZZZS receives these contributions after initial collection by the Financial Administration of the Republic of Slovenia, which monitors these payments. Between 2014 and 2018, the total revenue generated by ZZZS increased by 18.7%, to €2.7 billion from €2.2 billion (ZZZS 2017; 2020) due to employment and wage growth post-2013. Nevertheless, ZZZS operations are increasingly under pressure because of the contraction of the working-age population (UMAR, 2020b) (Box3.2).

Box3.2

In addition to SHI contributions, ZZZS receives other allocated funds such as non-tax revenues, capital revenues and grants. ZZZS revenue from SHI contributions and transfers represented 95.0% of total ZZZS revenue in 2018 (80.8% from contributions and 14.2% from social security transfers) – down from 98% in 2014. Most (>85%) of social security transfers are from the Pension and Disability Insurance Institute (ZZZS, 2019).

General taxation is non-earmarked revenue flowing from central revenue sources to the MoH budget or local tax revenues to municipal budget(s). Central budget tax revenue collected by the Tax Office of Slovenia includes revenue from income, corporate, value-added and excise tax. Municipal budget tax revenue from local taxes is collected by the municipalities. The amount of tax revenue nationally and locally allocated for health is not fixed but is estimated annually. In 2018, together, national and local government expenditure to health amounted to 3.4% of CHE excluding investments (Zver, 2021; UMAR, 2020b).

3.3.3. Pooling and allocation of funds

As per the Health Care and Health Insurance Act (1992), ZZZS is the sole provider of SHI. It collects and pools the contributions (see section 3.3.2). For each annual financial plan, it defines a maximum amount of collected contributions to be spent on health services for the upcoming year, informed by current and future macroeconomic conditions that influence the sum of contributions and other revenues of the ZZZS. This includes expected growth in GDP, rate of inflation, growth of wages and pensions and unemployment rates.

The national health budget is determined centrally by ZZZS in cooperation with the MoH and the Ministry of Finance. Once developed, it is presented to the ZZZS Board and Parliament and, after their confirmation, approved by the Government. The budget allocates resources based on historical data to different care areas, but there is no further allocation of health budget on a geographical basis, aside from local tax revenue flowing to municipal budgets. Annually, in parallel to the planning of the national budget, ZZZS and the Ministry of Finance establish a cap for total public expenditure on compulsory health insurance, which is then implemented into the contracts between ZZZS and health care providers (see sections 3.3.4 and 3.7).

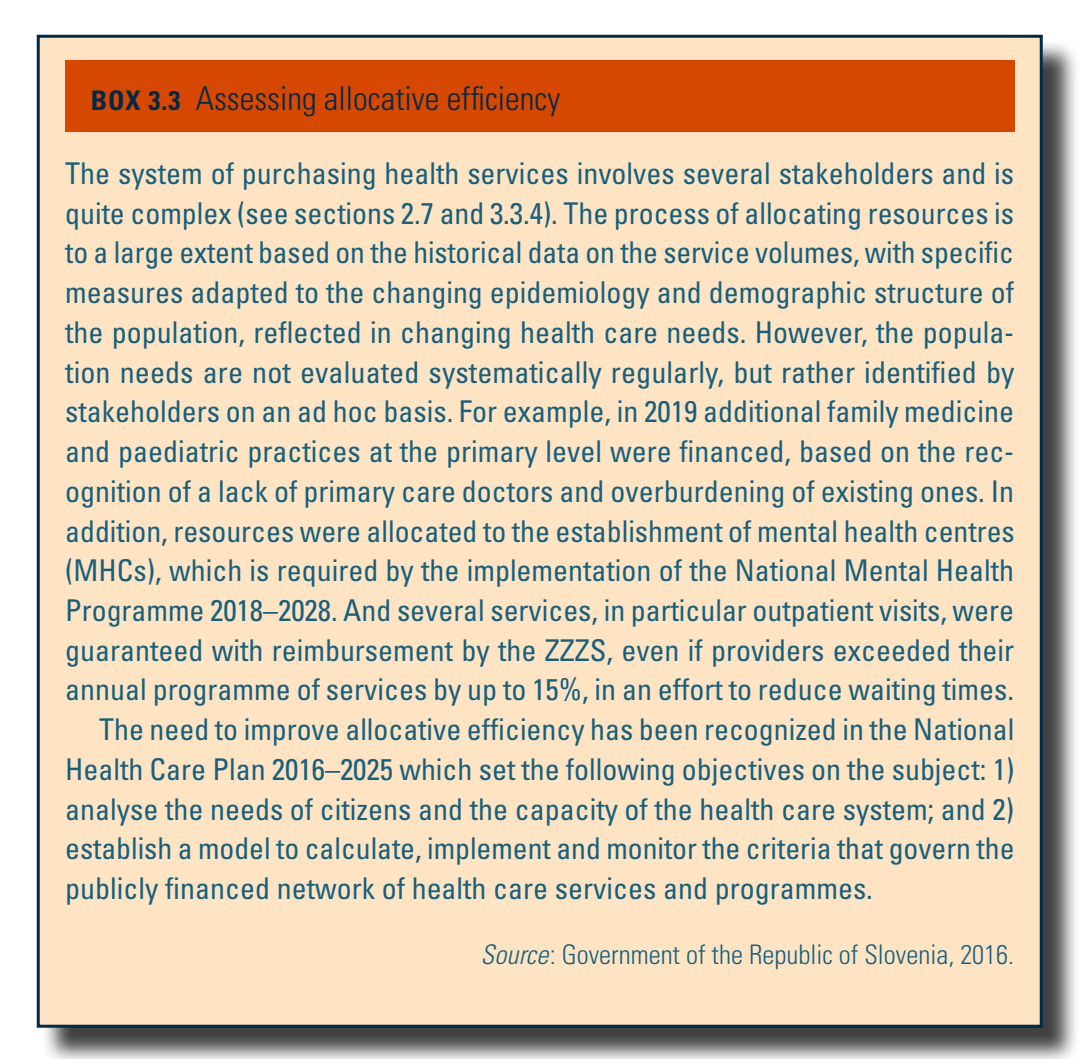

See Box3.3 for the assessment of allocative efficiency.

Box3.3

3.3.4. Purchasing and purchaser–provider relations

Health services in the statutory system are purchased by ZZZS. Purchasing occurs through a multi-step, stakeholder negotiation process (see section 2.7), through which the services to be reimbursed by ZZZS and the volume of services to be provided are defined in annual agreements. The MoH, ZZZS, the Association of Health Institutions of Slovenia, the Medical Chamber of Slovenia, the Slovene Chamber of Pharmacy, the Association of Social Institutions of Slovenia, the Association of Slovenian Training Organizations for Persons with Special Needs and the Association of Slovenian Natural Spas all participate in formulating this General Agreement, which clearly sets budgets for the services to be covered by public resources in compulsory health insurance.

The two-stage procedure for negotiating the General Agreement has not changed since it was first introduced in the Health Care and Insurance Act (1992). First, partners negotiate amendments to the existing General Agreement; only recommendations with 100% agreement among partners are adopted. Second, an arbitration phase begins, where controversial issues are negotiated. The quorum remains the same: changes are only adopted following full agreement of all participants. Most issues are about the level of funding and prices paid. For any remaining points, the government decides. The whole procedure of negotiations is not efficient, as partners can submit an unlimited number of recommendations or controversial issues and stall the process.

Based on the General Agreement, ZZZS and individual providers in the public network then develop a contract specifying the type and volume of services to be provided (see section 2.7.2), as well as tariffs, methods of payment, quality requirements and supervision criteria. ZZZS issues public tenders open to all public providers and concessionaires. Selective contracting is not possible and there is no true competition for contracts. However, ZZZS has tendered certain programmes to address specific, priority issues (e.g. increasing the volume of services in sectors with lower accessibility/longer waiting times). Although the General Agreement and subsequent individual provider contracts contain provisions on monitoring quality, these are insufficiently implemented and evidence-based clinical pathways and treatment protocols are not in place. Generally, contracts are unspecific and providers have considerable latitude regarding their activities.