-

05 February 2025 | Country Update

A newly created institution joins the National Health Insurance Fund in managing named-patient reimbursement -

01 January 2019 | Country Update

Public health product tax increases by 20 percent -

01 January 2019 | Country Update

Outlook on the public financing of the Hungarian health system in 2019 -

22 August 2018 | Country Update

Taxation instead of contribution -

18 December 2017 | Country Update

More billion HUF for Offices of Health Development -

27 September 2016 | Country Update

Sub-budget “sweeping” in publicly funded health care – health care providers receive 7 billion HUF -

08 March 2013 | Policy Analysis

Taxation on high-risk products used to boost health system revenue and improve health status -

14 October 2012 | Country Update

Paradigm shift in health care financing in Hungary: increasing reliance on consumption taxes levied on products with significant health risk? -

31 December 2011 | Country Update

A symbolic move towards tax financing of health care in Hungary

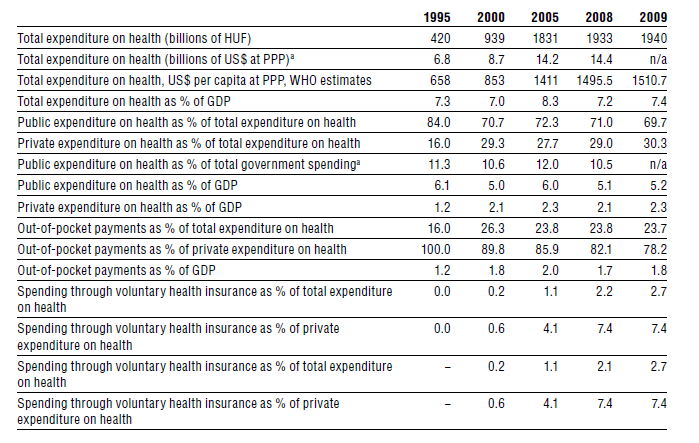

3.2. Sources of revenue and financial flows

Public expenditure on health in Hungary is financed mainly through a combination of SHI contributions and general tax revenue transfers to the SHI scheme. In addition, revenue from general and local taxation plays a significant role in financing capital costs, public health services and some expensive health technologies. Private sources of revenue include charities, NGOs and corporations, voluntary health insurance as well as a considerable share of OOP payments (see Fig3.4). In 2009, 58.8% of total expenditure on health was covered by the HIF (OECD, 2011). The revenue of the HIF is derived mainly from (a) SHI contributions, which, for employees, take the form of a proportional payroll tax that is split with employers; (b) general tax revenue transfers from the central budget; (c) direct payments from pharmaceutical companies (see sections 2.8.4 and 6.1.2); and (d) the hypothecated health care tax. This hypothecated health care tax was introduced in 1997 and consisted of two components: a lump-sum tax and a proportional tax. The proportional tax is levied only on income that is not subject to the SHI contribution (see also section 3.3.2). The lump-sum tax was eliminated at the beginning of 2010.

Fig3.4

The share of total health expenditure financed through central and local governments in 2009 was 10.9% (Fig3.5), but this does not capture (a) the tax revenue transferred from the central budget to counter HIF imbalance (see section 3.3.3) and (b) the hypothecated health care tax, which is also transferred to the HIF. If, however, we consider the real sources of revenue and not the agents through which the spending is administered, then the share of total health expenditure financed through general and local taxes in 2009 rises to 35%, while the share financed through SHI contributions would be 32.5% (Fig. 3.5). Interestingly if this latter approach is used when looking at earlier expenditure data, the share of total health expenditure financed from general and local taxes in 2002 and 2003 turns out to be even higher than that financed from SHI contributions. Although this might seem a rather peculiar way to pool resources in an SHI system, it is very much in line with recent trends in Europe – that is, to move away from exclusive reliance on labour-related social insurance contributions and use a mix of revenue sources for financing the health insurance system. This development, however, did not follow an explicit taxation policy strategy in Hungary until the recent financial crisis, when the government decided to radically reduce the SHI contributions and compensated this loss of revenue by increased general tax revenue transfers to the HIF (see section 3.3.2).

Fig3.5

Whereas recurrent expenditure is financed by the HIF, nearly all capital investment related to outpatient and inpatient care is financed by the central and local governments. Nonetheless, the central government still pays for recurrent expenditure related to certain services (for example, high-cost high-technology treatments and public health) and covers co-payments for residents with very low incomes. Since the mid-1990s, governments in Hungary have used cuts in the SHI contribution rate as one of their main tools for boosting employment, but have failed to compensate the HIF adequately for the resulting shortfall in revenue, leading to a prolonged financial imbalance (see section 3.3.3). Private health insurance plays a fairly limited role in health care financing, with a share of 2.7% of the total health expenditure in 2009 (Table3.1). Most of the expenditure under the private health insurance heading is actually not insurance, but individual medical savings accounts (MSAs) without any pooling across individuals beyond the family. The MSA scheme has benefited from tax subsidies, but in recent years these subsidies have been reduced and the scope of services that the MSA scheme can cover was also restricted. Overall, OOP expenditure continues to be the dominant form of private expenditure in Hungary (see section 3.4).

Table3.1

An omnibus legislation adopted in June 2024 (see the policy analysis “Omnibus legislation and need for more system approach” from 16 August 2024) amended Act LXXXIII of 1997 on Compulsory Health Insurance Benefits, mandating the government to establish a foundation (“Batthyány-Strattmann László Alapítvány a Gyógyításért”). This foundation will assess named-patient reimbursement requests and decide on reimbursements for “medically accepted” medicines and medical aids not covered by the compulsory social insurance scheme [1].

Formally registered in January 2025, the foundation already began its responsibilities in February 2025 [2]. The foundation is funded through the state budget [1]. As an organization for public benefits, the foundation may also receive additional financing through donations, including the 1% of personal income tax that Hungarians can offer to support non-profit organizations [3]. Further details on operations may emerge later.

Authors

From 1 January 2019, the Public Health Product Tax (NEAT) will generally increase by 20 percent for foods and beverages causing health risk. In addition, as announced by the Ministry of Finance, other drinks will be subject to the tax, including fruit spirits, fruit brandies and herbal drinks containing alcohol. In the central budget of Hungary for 2019, the Ministry expects 57 billion HUF (181 million EUR) in revenues from NEAT compared to 30,4 billion HUF (97 million EUR) in the previous year. The Public Health Product Tax was the source of salary increases and scholarship programs in the health sector.

Authors

The share of spending on the health sector from the central budget will rise from 8.4 in 2018 to 8.6 percent in 2019, an increase of 101 billion HUF and totalling 1711 billion HUF (5.4 billion EUR) in 2019.

The biggest budget increase will flow to the Health Insurance Fund for consolidated healthcare services. The budgets for healing-preventive care, sickness benefits, pharmaceutical subsidies and pharmaceutical support will also increase. Despite of the important role of public health intervention programs, the field will receive exactly the same budget (1.7 billion HUF or 5.4 million EUR) in 2019 as 2018. The budget for development and extraordinary support of healthcare institutions available under the Ministry of Human Capacities will also remain the same as the previous year.

The 2019 budget does not contain evidence of funding for the necessary modernization of hospitals, which suggests that the runaway debt spiral of hospitals will continue as one of the biggest problems in the health sector.

Authors

References

This summer “tax package” of the government proposes to merge the employer social contribution tax and the hypothecated health care tax. According to the bill, the latter would be abolished on 1 January 2019, and the social contribution tax has to be paid on those types income, which were previously subject to the hypothecated health care tax.

Experts expressed their concerns, as under this new tax regime the government has no obligation to spend these revenues on health care.

Authors

In the following months new Offices of Health Development will be established -announced the Parliamentary State Secretary of the Ministry of Human Capacities. The first Offices of Health Development were funded as an EU project and later on were operated from the central budget. The offices are essential in health development, to promote the importance of prevention and health awareness among the population. During the last years 200.000 people had been reached by the 61 existing offices.

Bence Rétvári declared that 50-60 new offices will be opened from 4,5 billion HUF, while in Buda and Pest county 15-30 more offices will be established with 1,7 billion HUF. Moreover 2,5 billion HUF will be delegated for special support for those who suffer from mental illnesses.

Dr. Tamás Szentes, Deputy Secretary for Public Health explained, with the new offices a more centralized system will be developed, where thematic programs will reach the population changing by every month.

Authors

Sub-budget “sweeping” is the process in the Hungarian social health insurance system, whereby the end year residuals of the sub-budgets of the HIF are distributed among contracted health care providers by the National Health Insurance Fund Administration (NHIFA).

At the end of 2015, HUF 7 billion from the Health Insurance Fund (HIF) was paid out to publicly funded health care providers. Providers of outpatient specialist care received HUF 4.7 billion, while HUF 1 billion went towards decreasing waiting lists, and HUF 500 million towards promoting one-day surgery. Hospitals providing additional oncological diagnostic services received HUF 800 million, in line with earlier regulation incentivizing service providers to complete diagnostic tests of suspected cases of malignancies within 6 weeks.

Authors

The Hungarian Parliament approved the Act on a new earmarked excise tax, the so-called “public health product-tax” in July 2011. The tax aimed both to collect additional revenues for the health system (especially to finance public health programs) and to decrease the consumption of unhealthy foods, such as soft drinks above a certain sugar content and under a certain fruit content; energy drinks; packaged sweet biscuits, candy and ice-cream above a certain sugar content; and crackers and food flavorings above a certain salt content. The new tax is flat, based on the ex-factory price of the product. Taxation of trans fat was also strongly recommended, but it was instead agreed that the use of this ingredient would be completely banned. Regarding the scale and composition of the potential revenue from these sources, the NHIFA estimated a total of 20 billion HUF, which amounts to approximately 1.5% of the public expenditure on health. A sizable part of this amount will come from energy drink taxation. This development seems to be a landmark in financing health services in Hungary, as the Ministry of Finance had consistently blocked this policy option in the last 20 years. Moreover, this regulation opens the way for further innovative refinement of health financing.

In addition, the Hungarian Parliament is going to modify several acts connected to the financing and revenue collection functions of the health system with the aim of raising additional funds. Government representatives recently informed Members of Parliament at the Health Committee meeting that the government expects an additional 50-55 billion HUF (4% of public expenditure on health in 2010) in revenue from the taxation of energy drinks, the increased taxation of alcohol and tobacco as well as tax on LPG (Liquefied Petroleum Gas, a type of motor fuel). Furthermore, the Ministry for National Economy indicated that the increase in the taxation of tobacco and alcohol will also have a significant impact on consumption, therefore on population health status. In February, the government raised the excise tax on tobacco by 10%, and increased it again by 4% in July. Two further steps are planned in 2013: the tax will grow a further 15% as of January and a further 13% as of May. In sum, between January 2012 and May 2013 the rate of taxation on tobacco would be up by 47%. Also, the tax on several types of alcoholic beverages will be raised (by 10-15% for beer, spirits and champagne).

The Members of Parliament in the Health Committee welcomed these plans, but some of them expressed their doubts whether the government would indeed use the additional revenues for the health system or use them to replace part of the current central budget transfers to the Health Insurance Fund (HIF), making the actual purpose of these measures decreasing the deficit of the central government budget. In 2011, the government introduced a new public health tax, levied on energy drinks and products with high sugar and salt content, such as fizzy drinks and salty snacks. Although the Act explicitly states that income from these sources belongs to the HIF (Act CLVI of 2011, Article 192), only about half of the revenues was used to actually increase health spending in 2012. The other half was used to compensate for a decrease in central government budget transfers to the HIF. This was also the case with the so-called “road vehicle accident tax”, introduced in November 2011, which is levied on the compulsory third party motor vehicle liability insurance to compensate the health sector for the costs of treating injuries caused by road accidents. While these revenues are also transferred to the HIF, central government budget transfers were decreased by the same amount.

Authors

The Hungarian Parliament is going to modify several acts connected to the financing and revenue collection functions of the health system with the aim of raising additional funds. Government representatives recently informed Members of Parliament at the Health Committee meeting that the government expects an additional 50-55 billion HUF (4% of public expenditure on health in 2010) in revenue from the taxation of energy drinks, the increased taxation of alcohol and tobacco as well as tax on LPG (Liquefied Petroleum Gas, a type of motor fuel). Furthermore, the Ministry for National Economy indicated that the increase in the taxation of tobacco and alcohol will also have a significant impact on consumption, therefore on population health status.

In February, the government raised the excise tax on tobacco by 10%, and increased it again by 4% in July. Two further steps are planned in 2013: the tax will grow a further 15% as of January and a further 13% as of May. In sum, between January 2012 and May 2013 the rate of taxation on tobacco would be up by 47%. Also, the tax on several types of alcoholic beverages will be raised (by 10-15% for beer, spirits and champagne). The Members of Parliament in the Health Committee welcomed these plans, but some of them expressed their doubts whether the government would indeed use the additional revenues for the health system or use them to replace part of the current central budget transfers to the Health Insurance Fund (HIF), making the actual purpose of these measures decreasing the deficit of the central government budget.

In 2011, the government introduced a new public health tax, levied on energy drinks and products with high sugar and salt content, such as fizzy drinks and salty snacks.Although the Act explicitly states that income from these sources belongs to the HIF (Act CLVI of 2011, Article 192), only about half of the revenues was used to actually increase health spending in 2012. The other half was used to compensate for a decrease in central government budget transfers to the HIF. This was also the case with the so-called “road vehicle accident tax”, introduced in November 2011, which is levied on the compulsory third party motor vehicle liability insurance to compensate the health sector for the costs of treating injuries caused by road accidents. While these revenues are also transferred to the HIF, central government budget transfers were decreased by the same amount.

Authors

By renaming the employee social health insurance contribution “social contribution tax”, the Parliament made an additional move in strengthening direct governmental control over financing, revenue collection and financial resource allocation in the health system. The new tax will not only fund health but also pensions and other social policy public expenditures. The prevailing budget law will decide on the actual distribution between the different social policies and budget funds.