-

23 January 2019 | Country Update

Expansion of tax benefits for patients

7.2. Financial protection and equity in financing

The government will expand tax benefits to additional patient groups, as announced by Ildikó Horváth, the Secretary of State for Health. From 2019, tax deductions are claimable for patients suffering from breast, ovarian and cervical cancer, endometriosis, or testicular and prostate cancer. The tax-benefit is 5 percent of the current minimum wage, at 7450 HUF (23.70 EUR) per month. Overall, this will result in 90,000 HUF (286 EUR) more income per year, as reported by Norbert Izer, the Secretary of State for Tax Affairs from the Ministry of Finance. The tax benefit can be written off from the personal income tax with a special certificate from the associated medical doctor.

Authors

References

335/2009. (XII. 29.) Government Decree

Hungarian News Agency

http://medicalonline.hu/eu_gazdasag/cikk/horvath_ildiko_az_adokedvezmenyekrol?utm_source=newsletter&utm_medium=medicalonline_hirlevel&utm_campaign=24061

7.2.1. Financial protection

The magnitude of private expenditure on health in Hungary – most of which is attributable to OOP spending – is still unclear, not least because of divergent estimates on the extent of informal payments (see section 3.4.3 as well as section 3.1). OECD data indicate that after an increase from about 11% in 1991 to a peak of 31% in 2001, private expenditure as a share of total expenditure on health has hovered between 27% and 30%. The figure for 2008 was 29%, which puts Hungary in second place within the EU – just below the Slovak Republic (30%), slightly above Poland (28%), and considerably higher than the Czech Republic (18%) (OECD, 2010). A breakdown of OOP spending in Hungary can be found in section 3.4.

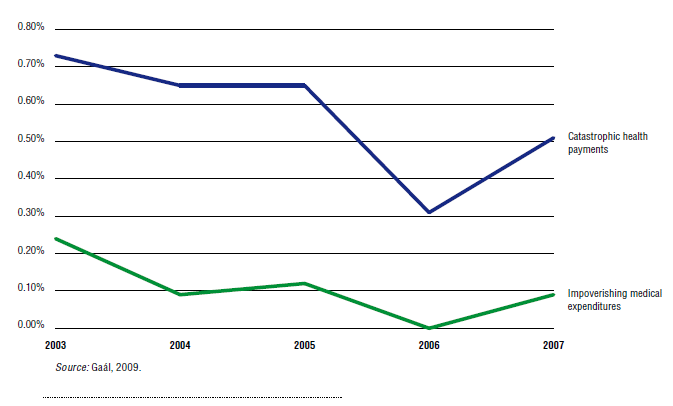

Despite these numbers, according to a recent WHO study on financial protection, less than 1% of Hungarian households experienced catastrophic[24] (0.31–0.73%) or impoverishing (0.003–0.24%) health expenditure between 2003 and 2007, and the poverty gap was small. This means that some 11 000–28 000 households in Hungary experienced catastrophic expenditure, and 3400–9000 households experienced impoverishing health expenditure during this period, with a poverty gap of HUF 1–2 billion (€3.95–7.9 million) (Gaál, 2009).

Looking at these indicators over time shows that between 2003 and 2006, there was a decrease in the percentage of catastrophic and impoverishing health expenditure, followed by a notable increase in 2007 (Fig7.1). This increase coincides temporally with the introduction of several health policy measures, including user fees in ambulatory and inpatient care (see section 3.4) and an increase in and restructuring of cost-sharing for pharmaceuticals (2006/8).

Fig7.1

An important disadvantage of indicators such as catastrophic and impoverishing health expenditure is that they cannot capture the whole impact OOP spending has on the poor. For example, low-income households might not experience catastrophic health expenditure during a particular study period because they delay or forgo health care precisely due to the deterrent effect of high OOP payments.

Even though user charges introduced in February 2007 (and eliminated in April 2008) involved the seemingly negligible amount of HUF 300 (or about €1.20) per outpatient visit and per hospital day, their deterrent effect on the poor was indeed unexpectedly large. According to a survey carried out in April 2007, 15% of respondents said that had not visited a physician because of the co-payments. Among people who had completed only their primary education, this figure was as high as 25%, whereas it was 10% among those with a higher degree of educational attainment. Similar differences were observed among different income groups (GfK Hungaria, 2007).

These user charges were also expected to tackle the issue of informal payments (see section 3.4). However, according to another survey, 30% of participating physicians reported that the introduction of co-payments diminished informal payments by an average of 14%, whereas 47% did not notice any change and 1% observed an increase. Only 6.6% of patients said that they had not made any informal payments, or paid less since the introduction of user charges (Szinapszis Kft, 2007). A different study estimated a decrease of 25% in informal payments overall (Medián, 2008). Finally, expenditure on informal payments and the newly introduced co-payments combined increased by over 20% in nominal terms in 2007. This suggests that the overall burden on patients increased, compromising financial protection, equity in financing and access to care.

- 24. In this study, household expenditure on health was considered catastrophic when it exceeded 40% of the household’s disposable income. ↰

7.2.2. Equity in financing

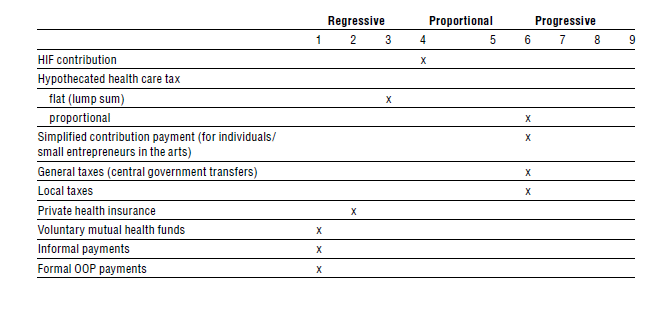

When evaluating equity in financing in the Hungarian health care system, it is essential to distinguish between theory and practice. By design, the sources of health care financing in Hungary are predominantly public and thus theoretically closer to the middle of the regressivity–progressivity spectrum. Although no longer subject to a ceiling, HIF contributions remain mildly regressive because (a) they are levied only on gross wages (and not on capital income) and (b) there is a minimum contribution base. The hypothecated health care tax, however, is more difficult to place on the regressivity–progressivity spectrum. Whereas the lump-sum component, in place until January 2010, was clearly regressive, the proportional component is levied on income types that are typically derived by individuals with higher incomes, such as dividends and in-kind allowances. Accordingly, the new hybrid tax/contribution (2005/6), called the “simplified contribution payment”, alone can be described as progressive, as it can only be used by artists and media workers who are usually on the wealthier side of the population. However, they end up paying much less in total than others if all taxes and contributions are taken into account, suggesting rather regressivity (revenue from this source represents only a negligible share of total HIF revenue anyway – see section 3.3.2 and subsection Revenue collection in section 6.1.2).

Unlike these earmarked sources of revenue, central government transfers to the HIF can be classified as progressive, as they are financed through general taxation. Since 2006 there has been a strong shift towards funding the health system through general taxation, a phenomenon very much in line with recent trends in Europe, which move away from exclusive reliance on labour-related social insurance contributions and use a mix of revenue sources for financing the health insurance system (see section 3.2).

At the same time, a large share of health system financing in Hungary is private, consisting mainly of OOP payments, which by definition are strongly regressive. Table7.1 gives an overview of the progressivity of the main sources of health care financing in Hungary.

Table7.1

In practice, it is essential to take into account the ability and willingness of members of society to pay taxes and contributions. Avoidance and evasion have been a persistent problem in Hungary, especially in the health care system. Combined, unpaid health and pension insurance contributions peaked at 4.3% of GDP in 1994, but still amounted to almost 1% of GDP in 2008, out of which 40% was HIF-related payment arrears and claims (NHIFA, 2008, 2009b). In the past, the high rate of social insurance contributions in Hungary likely contributed to late payments, non-payment and under-reporting of income. Arguing that high contribution rates also have an adverse impact on (formal) employment and the competitiveness of the Hungarian economy, successive governments have attempted to address the problem by cross-checking patients’ insurance status (see section 3.3.1),lowering contribution rates, widening the contribution base and introducing other forms of revenue that are less prone to evasion (see section 3.3.2). According to government estimates, the first measure identified 150 000 free-riders, increasing revenues from this source by almost 70% between 2007 and 2008 (i.e. an additional HUF 1.75 billion or €6.9 million). The reduction of the employer contribution rate, on the other hand, decreased HIF revenues without successfully boosting employment (see section 3.3.2) (NHIFA 2009b).

Changes have also been implemented to shift some of the burden from the public to the private purse, whether through increased OOP payments (see also section 3.1) or by encouraging voluntary complementary health insurance. Initially, the voluntary health insurance scheme introduced in 1993 was non-profit, with community rating and no risk-adjustment prior to participation (1993/10). The risk-sharing component was decreased to 40% of the insurance premium in 1996 and was eventually eliminated in 2003, whereupon the entire scheme was transformed to a system of MSAs, which is a more regressive form of private financing (see also section 3.5.1).

The overall impact of related reforms over the past 20 years is difficult to assess, as the success of different measures varies greatly. A study published in 2002 used the Kakwani index,[25] a summary indicator of equity in financing widely used in international literature, and estimated the total financing burden of the Hungarian health care system as mildly regressive (-0.0211), with overall public sources being mildly progressive (0.0260) and private sources regressive (-0.2745) (Szende et al., 2002). Unfortunately, there is no recent evidence on this issue, except for private expenditure, which was found to be slightly less regressive in 2007 (-0.2726) than in 1999 (Csaba, 2007).

- 25. The Kakwani index combines population income distribution with concentration of the burden of various health financing revenue sources. It does not take into account the potential level of tax and contribution evasion. ↰