-

08 December 2025 | Country Update

Medicines pricing and tariff agreement between USA and United Kingdom

2.7. Regulation

Regulatory bodies set standards, monitor organizations to ensure compliance with those standards and enforce consequences for providers that fail to meet standards. The major arm’s-length bodies of the DHSC with a regulatory role are the Care Quality Commission and NHS England in England, NICE, and the Medicines and Healthcare products Regulatory Agency (MHRA) (see section 2.2 Organization).

2.7.1. Regulation and governance of third-party payers

In England, third-party payers are the CCGs, which negotiate contracts to purchase mental health and community health services from public and private service providers, and NHS England, which negotiates contracts for most primary care services and specialist services. CCGs are due to be replaced with ICSs from July 2022, which will undertake similar functions, but for all health and social care services for predefined local populations in conjunction with local authorities (see section 2.2 Organization). The financial sustainability of CCGs is monitored by NHS England, which sets efficiency targets and provides additional support through the Commissioner Sustainability Fund to CCGs, which persistently post deficits (NHS England, 2020f). In Wales and Scotland, health boards are essentially integrated purchasers and service providers and are answerable to their respective national governments (see section 2.4 Planning). In Northern Ireland, the Health and Social Care Board is the default commissioner for all health and social care services, although due to a limited choice of providers, the relationship between the Health and Social Care Board and providers is understood more as governance and oversight, rather than commissioning. Similar to Wales and Scotland, the Health and Social Care Board in Northern Ireland is accountable to the Minister of Health. In all four United Kingdom constituent countries, there is a National Audit Office, which has a key role in scrutinizing public spending, including public spending by local commissioners and health boards.

2.7.2. Regulation and governance of provision

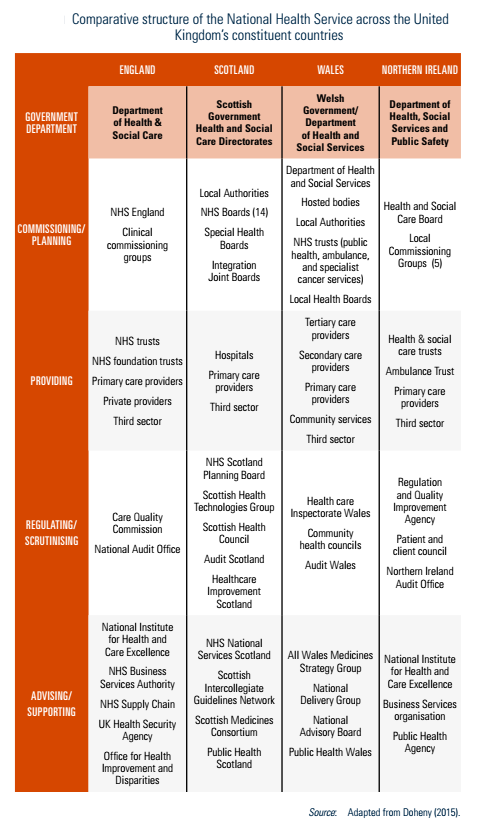

England, Scotland, Wales and Northern Ireland each has its own regulatory bodies, including the Care Quality Commission and NHS England, Healthcare Improvement Scotland, Healthcare Inspectorate Wales, and the Regulation and Quality Improvement Authority in Northern Ireland (Table2.1).

Table2.1

In England, the Care Quality Commission registers, monitors, inspects and regulates both NHS and independent sector services in England to ensure that they meet fundamental standards of quality and safety (Cylus et al., 2015). The remit of the Care Quality Commission extends to health and social care, including hospitals, dentists, GPs, ambulances, care homes and the care given in people’s own homes. The Care Quality Commission sets the minimum standards of care, as well as determining what constitutes good and outstanding care. If services fall below the minimum standards, the Care Quality Commission has the power to define what providers need to do to improve the quality of care or, if necessary, can limit a provider’s activities until the necessary changes have been made. Its regulatory powers include issuing cautions and fines, and where patients have been harmed or put at risk, they can also prosecute.

Similar to CCGs, NHS England is the economic sector regulator for all providers, including private and not-for-profit groups that provide NHS-funded care. Between 2004 and 2016, this function was undertaken by Monitor, an executive non-departmental public body of the DHSC. The function was transferred to NHS Improvement in 2016, and since 2019, NHS Improvement was incorporated into NHS England. NHS England monitors the financial sustainability of providers and setting efficiency targets. For those providers that persistently post deficits, there is increased scrutiny of financial planning and financial targets, which if met, release additional financial support through the Provider Sustainability Fund (NHS England, 2021d). Since 2002, NHS hospitals that meet criteria around financial sustainability and managerial structures have been allowed to apply for Foundation Trust status, which allowed a degree of higher autonomy in financial planning (Collins, 2016). However, since the financial crisis, when over half of NHS hospitals persistently posted deficits, there has been greater regulation of financial planning, and there is little distinction between NHS hospitals with or without Foundation Trust status in terms of regulatory oversight from NHS England.

In Scotland, Healthcare Improvement Scotland oversees quality of care delivered by both the NHS and the independent sector (Cylus et al., 2015). The remit of Healthcare Improvement Scotland inspections is health care services, whereas the Care Inspectorate is responsible for inspections for social care providers. Healthcare Improvement Scotland drives health care practice improvements, scrutinizes care to ensure quality and safety, and develops guidelines, advice and standards for effective clinical practice. Healthcare Improvement Scotland inspects every acute hospital in Scotland at least once every three years and more often if needed. NHS boards are expected to adhere to the Scottish Intercollegiate Guideline Network (now part of Healthcare Improvement Scotland) guidelines, and Healthcare Improvement Scotland conducts performance reviews to ensure this. Healthcare Improvement Scotland does not have enforcement powers against NHS boards, although it does have such powers against independent sector providers.

In Wales, Healthcare Inspectorate Wales monitors NHS and independent sector services in order to ensure safety and quality (Cylus et al., 2015). Healthcare Inspectorate Wales focuses on improving patient experience and strengthening the voice of the public in reviewing health services. Like its counterpart in Scotland, the remit of Healthcare Inspectorate Wales is health care services only, and Healthcare Inspectorate Wales does not have enforcement powers against NHS hospitals but does have such powers against independent sector providers. A separate Care Inspectorate for Wales is responsible for inspecting social care providers.

In Northern Ireland, the Regulation and Quality Improvement Authority monitors the availability and quality of health and social care services, ensuring that services meet standards and are easy to access, whereas the Department of Health is responsible for setting safety and quality standards (Cylus et al., 2015). The Regulation and Quality Improvement Authority inspects services ranging from children’s homes to nursing agencies, as well as health and social care trusts and agencies. It has a range of powers including issuing notices of failure to comply with regulations, placing conditions of registration, imposing fines and closing services.

2.7.3. Regulation of services and goods

Basic benefit package

Unlike some countries, constituent countries of the United Kingdom have neither a legally enforceable right to health nor a defined benefit package setting out their entitlements (Mason, 2005). As a result, since establishment, there has been a progressive withdrawal by the NHS from certain types of care, most notably a large share of dental care and optometry. There has also been growing efforts to disinvest in low-value care, most notably the Evidence-Based Interventions programme in England, Prudent Healthcare in Wales and Realistic Medicine in Scotland (see section 3.3.1 Coverage), which has explicitly outlined certain procedures, such as breast reduction and surgical intervention for snoring, which will not be routinely funded via the NHS. There are also a growing number of other procedures of low clinical value that will only be funded under certain circumstances, and activity levels are closely monitored to assess for unwarranted clinical variation. For procedures that are not routinely funded through the NHS, the only mechanism to secure NHS funding is through an independent funding request, whereby local commissioners review evidence on the potential benefit for individual patients, taking into account their specific context.

Health technology assessment

For novel health technologies, a rigorous and transparent system of health technology assessment has been developed in the United Kingdom, using the cost per QALY and threshold approach (Charlton, 2020). In England, NICE undertakes this function and has several programmes for appraising new technologies, including drugs, devices, diagnostic procedures and public health interventions. All the programmes, except for the Interventional Procedures Programme (which considers only clinical evidence), consider both clinical and cost-effectiveness. The central feature of NICE’s approach for appraising technologies is the calculation of the incremental cost per QALY gained, over and above the current standard of care, and to compare this with a decision-making threshold, currently set between £20 000 and £30 000 per QALY (NICE, 2015). The QALY is intended to provide a generic measure of “health gain” and combines data on extension of and quality of life. The decision-making threshold is intended to represent the opportunity cost of the current NHS budget constraint. However, there are a number of additional circumstances under which this threshold changes, for example for therapies that add more than three months to the life expectancy of patients having no more than 24 months to live (Bovenberg, Penton & Buyukkaramikli, 2021). In practice, this has resulted in NICE valuing QALYs gained at end-of-life at 2.5 times “standard” QALYs, implying a decision-making threshold of £50 000 per QALY. There are also circumstances in which NICE may deviate from this threshold, for example when agreeing management access agreements with the pharmaceutical industry that may involve confidential financial discounts or requirements to collect additional data to establish cost-effectiveness. The remit of NICE also extends to pre-existing technologies through its clinical guidelines programmes, which explicitly consider costs through a systematic review of economic evaluation literature and identify candidates for disinvestment. However, unlike the technology appraisal programmes, adoption of recommendations is not mandatory for the NHS (Drummond, 2016).

Similar bodies assess health technologies in other parts of the United Kingdom, most notably the Scottish Medicines Consortium (SMC) and Scottish Health Technologies Group (SHTG) in Scotland, both part of NHS Healthcare Improvement Scotland. SMC assesses medicines and SHTG assesses non-medicine devices. The All Wales Medicines Strategy Group (AWMSG) in Wales assesses pharmaceuticals. The remit of AWMSG is complementary to that of NICE, only including the assessment of new pharmaceuticals that are not on the 12-month work programme of NICE (Varnava et al., 2018). Moreover, NICE guidance can supersede AWMSG recommendations (Varnava et al., 2018). In contrast, the scope of SMC and SHTG are not complementary to NICE, and each organization issues separate recommendations on new pharmaceuticals and devices. Northern Ireland does not have an equivalent body; instead, the Northern Ireland Department of Health endorses NICE guidance, unless it is not found to be locally applicable.

2.7.4. Regulation and governance of pharmaceuticals

The manufacture, licensing and regulation of medicines and the control of pharmaceutical prices is all done at United Kingdom level (Cylus et al., 2015). From 1 January 2021, following the withdrawal of the United Kingdom from the EU, the MHRA became the United Kingdom’s stand-alone medicines and medical devices regulator. Before this, medicines could be launched in the United Kingdom via the European Medicines Agency centralized authorization procedure (Criado & Bancsi, 2021). The MHRA is an executive agency of the DHSC; it authorizes clinical trials of drugs, assesses the results of trials, monitors the safety and quality of products and can remove products from the supply chain if it finds sufficient evidence that they are substandard.

The 2012 Human Medicines Regulations is the main legislation that governs medicines in all four United Kingdom constituent countries, replacing the previous 1968 Medicines Act. The regulations are concerned with processes for the authorization of medicinal products for human use; for the manufacture, import, distribution, sale and supply of those products; for their labelling and advertising; and for pharmacovigilance (UK Government, 2021c). The regulations list three types of pharmaceutical products: those on the General Sale List, which do not need a pharmacist and can be sold over the counter; those dispensed through pharmacists only; and prescription-only medicines. There is a formulary of licensed medicines, known as the British National Formulary, that contains available medicines, dosages, known side effects and monitoring requirements. Health care professionals are required to report suspected adverse effects to the MHRA through the Yellow Card Scheme, which is the system for recording adverse incidents with medicines and medical devices in the United Kingdom (MHRA, 2021). Advertising of prescription drugs is not allowed and advertisements for non-prescription medicines are strictly regulated.

Pharmacies in England and Wales are reimbursed through the NHS Prescription Services, which is part of the NHS Business Services Authority, according to the NHS Drug Tariff (NHS Business Service Authority, 2021). A similar system exists in Northern Ireland, operated by the Health and Social Care Business Services Organisation, and in Scotland, operated by the Chief Medical Officer Directorate of the Scottish Government. The NHS Drug Tariff details reimbursement levels for drugs and medical devices supplied to patients and rules to follow when dispensing. This includes a black list of pharmaceutical products that should not be prescribed or supplied to patients, and a grey list of pharmaceuticals that may be prescribed under certain circumstances, or for certain groups of patients or certain conditions only. Pharmacies are encouraged to procure medicines at cheaper prices than reimbursement levels set out in the NHS Drug Tariff because they can retain the difference as profit. There is, however, a clawback mechanism to ensure that a proportion of the difference between the price paid for the drugs by the pharmacy and what is reimbursed goes back to the NHS. Although the average clawback across all medicines is not routinely reported, according to the Pharmaceutical Services Negotiating Committee it is usually around 8% (PSNC, 2021).

In addition to the clawback mechanism for pharmacies, the DHSC claws back a proportion of NHS pharmaceutical expenditure via the voluntary scheme for branded medicines pricing and access (VPAS), dependent upon the profit margins of the pharmaceutical industry (DHSC & ABPI, 2018). In 2020, this amounted to £594 million, a reduction from £844 million in the previous year (UK Government, 2021g). VPAS and its predecessor, the pharmaceutical price regulation scheme, were developed to limit the costs of pharmaceuticals to the United Kingdom NHS in ways that would not undermine national interests in the pharmaceutical sector. They place a limit on the profits that individual companies can earn from supplying medicines to the NHS, estimated to allow a return on capital within certain limits. However, innovators remain free to set the prices of new products as they decided. Generic medicines are not subject to VPAS. Prices of generics can change over time to reflect the average market price of manufacturers or wholesalers after discounts. Generic manufacturers are regulated according to an anti-competition legislation, which is enforced by the Competition and Market Authority. Despite this, there have been some high-profile cases of gaming of prices of generic medicines; for example, an investigation by the Competition and Market Authority into the supply of fludrocortisone in 2019 exposed anti-competition agreements, resulting in a payment of £8 million to the NHS (UK Government, 2019).

The VPAS also includes a range of measures for the NHS to support innovation and better patient outcomes through improved access to novel and cost-effective medicines (DHSC & ABPI, 2018). This includes commitments by NICE to the accelerated assessment of novel medicines, including speeding up appraisals of non-cancer medicines to be in line with cancer medicine appraisal timelines, and for the NHS to invest in data infrastructure to understand and promote the uptake of cost-effective medicines. The Accelerated Access Collaborative, a partnership among NHS England, NICE and the pharmaceutical industry set up in 2018, works to achieve these objectives by identifying medicines that are considered as highly cost-effective to be designated as “rapid update products” that are prioritized for widespread adoption across the NHS (NHS England, 2021m). There is also an MHRA scheme, the Early Access to Medicines Scheme, to accelerate regulatory approval for medicines that do not yet have a marketing authorization when there is a clear unmet medical need for patients with life-threatening or seriously debilitating conditions (UK Government, 2021a). Under this scheme, patients can access medicines that receive a “Promising Innovation Medicine” designation up to 12–18 months before receiving formal marketing authorization.

On 1 December 2025, the United States of America and the United Kingdom announced an agreement on pharmaceuticals, with the UK promising its national health services (NHS) would accept higher prices and spending on branded medicines in exchange for zero tariffs on exports [1].

Key elements

The health technology assessment body for England and Wales, the National Institute for Health and Care Excellence (NICE) will raise its standard threshold for cost per incremental quality-adjusted life year from £20,000–£30,000 to £25,000–£35,000. Full details of this commitment are yet to emerge. NICE recommendations are often also transferred to Northern Ireland: Scotland has a separate body, the Scottish Medicines Consortium.

The agreement also commits that the primary UK-wide scheme for controlling NHS spending growth on branded medicines, the Voluntary Scheme for Branded Medicines Pricing, Access and Growth, will not require rebates greater than 15% between 2026 and its conclusion at the end of 2028 [2]. Under this scheme, participating pharmaceutical companies have to pay money back to the Department of Health and Social Care if their sales growth of eligible drugs exceeds an agreed-upon rate.

The UK’s representative body for the branded pharmaceutical industry also stated that the UK had committed to increase investment in new medicines from around 0.3% of GDP to 0.6% of GDP in stages over a decade, though this was not mentioned by either government [3].

The US has undertaken to place zero tariffs on UK-origin pharmaceuticals, pharmaceutical ingredients and medical technology exported to the USA for a three-year period.

Implications and reception

The agreement was praised by the pharmaceutical industry, which claimed that it would encourage investment in research and production [4]. Representative bodies for healthcare in the UK as well as the main academic units for health economics, both expressed concern that it represented a significant diversion of funding towards medicines with lower cost-effectiveness than most existing NHS care, shifting spending away from the most efficient use for health outcomes [5, 6].

There is no additional funding to cover spending under the agreement, and the UK government has not published any estimates of cost.

Authors

References

- https://www.gov.uk/government/news/landmark-uk-us-pharmaceuticals-deal-to-safeguard-medicines-access-and-drive-vital-investmentfor-uk-patients-and-businesses

- https://ustr.gov/about/policy-offices/press-office/press-releases/2025/december/us-government-announces-agreement-principle-united-kingdom-pharmaceutical-pricing

- https://www.abpi.org.uk/media/news/2025/december/uk-us-deal-is-good-news-for-nhs-patients-and-will-help-to-support-uk-life-sciences-competitiveness-says-abpi

- https://www.abpi.org.uk/media/news/2025/december/uk-us-deal-is-good-news-for-nhs-patients-and-will-help-to-support-uk-life-sciences-competitiveness-says-abpi

- https://www.nuffieldtrust.org.uk/news-item/nuffield-trust-response-to-reports-that-government-is-considering-raising-the-nice-threshold

- https://www.sciencemediacentre.org/expert-reaction-to-announcement-on-uk-us-pharmaceuticals-deal-and-changes-to-nices-cost-effectiveness-thresholds

2.7.5. Regulation of medical devices and aids

The MHRA is responsible for assessing the safety of novel medical devices, and post market surveillance and vigilance. Although it is compulsory that all medical devices, including in vitro diagnostic medical devices, placed on the United Kingdom market need to be registered with the MHRA, it is not compulsory that they are assessed by a health technology assessment agency before reaching the market. In 2010, NICE introduced the Medical Technologies Evaluations Programme to assess the cost-effectiveness of novel medical technologies (NICE, 2021). Manufacturers can volunteer to submit medical technologies to ask for a positive NICE recommendation if their device can be shown to reduce NHS costs, for example, by switching care from an inpatient to an outpatient (ambulatory) basis.

The procurement of medical devices and aids in England and Wales is conducted by health care providers through the centralized NHS Supply Chain service, which manages the procurement and delivery of a wide range of products. From 2018, logistics and operational management of the NHS Supply Chain service has been provided by Supply Chain Coordination Limited, a company wholly owned by the Secretary of State for Health and Social Care. Supply Chain Coordination Limited contracts with a variety of private logistic companies, whereas before this, DHL held a 10-year contract for NHS logistics. In Scotland, procurement is undertaken by NHS National Services Scotland, and in Northern Ireland by the Procurement and Logistics Service, part of the Health and Social Care Business Services Organisation.

In recent years, there have been efforts to accelerate the adoption of cost-effective medical technologies in the NHS. This includes the introduction of the MedTech Funding Mandate from April 2021, an NHS England commitment to give patients access to selected NICE-approved cost-saving devices, diagnostics and digital products more quickly (NHS England, 2021k). The Mandate aims to direct the NHS on which medical technologies are effective and likely to give savings on investment, with dissemination of medical technologies monitored at the local level. Criteria for inclusion in the MedTech Funding Mandate includes a positive recommendation from NICE, estimated savings to the NHS of over £1 million over five years, and the budget impact to the NHS should not exceed £20 million in any of the first three years (NHS England, 2021k).