-

14 July 2025 | Policy Analysis

Controversial healthcare reforms to ensure accessibility, sustainability and quality -

26 March 2025 | Country Update

Compulsory health insurance budget 2025 finally adopted -

28 November 2022 | Country Update

2023 budgetary objective of the compulsory health insurance -

17 June 2021 | Policy Analysis

A multi-year trajectory for the health care budget (analysis) -

01 March 2021 | Country Update

A multi-year trajectory for the health care budget

3.3. Overview of the statutory financing system

Context

On 4 June 2025, a preliminary draft law concerning several healthcare reforms was distributed to all organizations active in the healthcare sector in Belgium. This draft is part of the government’s commitment to establish a legal framework for healthcare reforms by the end of the year to ensure the sustainability, accessibility and quality of care.

Impetus for the reform

The government emphasizes the critical need for these reforms to tackle both current and future challenges within the healthcare system. They highlight that without substantial changes, it will be impossible to sustain high-quality and accessible healthcare for all.

Main purpose of the reform

According to the authorities, the primary purpose of the reform is to create a clear and unified legal framework that addresses various aspects of the healthcare system. These include better budget control, reduced administrative burdens and a stronger fight against fraud and abuse. The reform also aims to clarify responsibilities and prevent excesses while maintaining the freedom of healthcare providers. One of the most important, and controversial, goals of the reforms is to reduce the supplements charged above official tariffs by non-conventioned or partially conventioned healthcare professionals.

Content and characteristics

The reform is divided into six main areas:

- Budgetary process: Establishing clear guidelines and responsibilities for budget creation and control, including new mechanisms to address budget overruns.

- Convention mechanism and tariffs: Simplifying and unifying the convention process for all healthcare providers who agree to respect tariffs, and making it more attractive (e.g., some premiums will only be available for conventioned providers). For non-conventioned providers, caps on supplements are under discussion. The current proposal sets the maximum supplement at 25% of agreed tariffs for ambulatory care and 125% for inpatient care. At present, supplements can reach up to 300% of tariffs, which undermines accessibility.

- Consultation model: Streamlining the consultation process within the National Institute for Health and Disability Insurance.

- Digitalization: Reducing administrative burdens through increased digitalization.

- Control: Enhancing measures to combat fraud and abuse in the healthcare system.

- Anti-tobacco measures: Introducing stricter regulations against tobacco and vaping products.

Implementation steps

The government has begun discussions with all relevant stakeholders. A preliminary draft has been presented, and feedback is being gathered. The final law is expected to be approved by the end of the year, with certain measures, such as changes to the convention mechanism and tariffs scheduled to take effect in 2028.

Outcomes to date

The preliminary draft has sparked considerable attention and debate. On 7 July 2025, a first strike was organized, widely supported by various healthcare professionals. The reforms were perceived as a threat to their professional autonomy, remuneration and the quality of care. The government plans to address these concerns through further consultations and clarifications.

Authors

References

To control expenditure, a real growth cap has been established since 1995 to determine the budgetary objective of the compulsory health insurance. This cap is determined based on the previous budgetary objective (€31.8 billion in 2022), increased by a real growth norm (2.5% for 2023) and indexed (health index: 8.14% for 2023). The 2023 budget is therefore set to €35.3 billion. This budget is based on the new methodology, that is, a multi-year budget trajectory for health care (2022–2024) that integrates health care objectives. Within this budget, new initiatives are foreseen to improve the financial and physical accessibility of care, to increase the well-being of health care providers and to support physicians who fully agreedto respect the national fee schedule without asking for extra-billings in ambulatory care (‘conventioned physicians’). Savings are also foreseen by decreasing inappropriate care. Additionally, specific amounts beyond the budget are planned to compensate for the rising energy costs in hospitals or specific costs related to COVID-19.

For more details see: https://www.inami.fgov.be/SiteCollectionDocuments/budget_2023_conseil_general.pdf (in French).

Authors

3.3.1. Coverage

Breadth: who is covered?

Inspired by the Bismarckian model, the Belgian health system is based on compulsory health insurance characterized by the solidarity between all citizens and there is no selection based on health risks.

There are two requirements to be covered by the compulsory health insurance. First, each individual must register with a sickness fund. The choice is free, except for railway workers (see Section 2.4.1). Second, social contributions must have been paid.

About 99% of the Belgian population is covered by the compulsory health insurance. There are two main schemes: (i) the general scheme covering the main part of the population (employees, employees in incapacity, unemployed, retired people, widows, orphans, students, residents) and (ii) the scheme for the self-employed. This means that both economically active and non-active people, as well as their dependants, are covered. The approximately 1% that is not covered concerns people whose administrative and/or financial requirements have not been fulfilled. This does not mean that uninsured people have no right to necessary medical care. They can be covered by the public centre for social assistance (Openbare Centra voor Maatschappelijk Welzijn/Centres Publics d’Action Sociale (OCMW-CPAS)) of their municipality.

It should nevertheless be noted that some categories of vulnerable people (for example irregular migrants) are excluded from this calculation and are not covered by the compulsory health insurance. Nevertheless, they can benefit from health care through other provisions (see Box3.1). People covered by another insurance scheme are also not included in this calculation (for example foreign people working for the European Commission and other international organizations).

Scope: what is covered?

All reimbursed services are described in the nationally established fee schedule (called the nomenclature), which specifies the official fees and cost-sharing mechanisms determined through conventions and agreements negotiated yearly or every two years between representatives of sickness funds and health care providers. These conventions and agreements can also contain specific conditions related to the content, quality or quantity of care. Each agreement must fall within the budget and is submitted to the Budget Control Committee of the NIHDI (see Section 3.3.3).

A large range of services is covered, with about 15 500 codes in the national fee schedule in December 2018. Services not included in the fee schedule are not reimbursed. Sickness funds are legally bound to reimburse the claim from their registered members at the official reimbursement levels.

Reimbursement decisions are under the responsibility of different commissions within the NIHDI, such as the Commission for the Reimbursement of Medicinal Products, which assesses the request based on criteria such as the therapeutic added value of the product and the budget impact (see Section 2.4.4). Evidence-based practices with a high therapeutic value are preferentially reimbursed, whereas aesthetic services such as plastic surgery or orthodontics are only reimbursable under certain conditions (for example, breast reconstruction after cancer). Alternative therapies such as acupuncture, homeopathy and osteopathy are excluded but may be partially covered by the complementary advantages provided by the sickness funds (see Section 3.5). Some preventive health care services are co-financed by the Federal government and the Federated entities, and are provided free to patients (for example, programmed vaccinations for children and programmed breast cancer screening).

Depth: how much of benefit cost is covered?

The share of out-of-pocket payments in current health care expenditure slightly decreased from 19.2% in 2007 to 17.6% in 2017. Since 2014, it has been below the EU15 average (17.8% in 2017). VHI represented 5.1% of current health expenditure in 2017. Looking at the extent to which different health services are financed through out-of-pocket payments indicates the main gaps in health coverage (see Box3.2).

However, it is important to note that in Belgium, precise data on out-of-pocket payments in the ambulatory sector are not available and there are some doubts on the reliability of these estimations (Calcoen et al., 2015).

3.3.2. Collection

Since 1995, the financing of the Belgian social security system has been based on the principle of pooling funds (so-called financial global management). This means that the majority of resources used to finance the seven branches of social security are combined and then transferred to each branch depending on its respective financial need. The seven branches include: old-age and survivor’s pensions; unemployment; insurance for accidents at work; insurance for occupational diseases; family benefits; annual vacation; and the compulsory health insurance managed by the NIHDI.

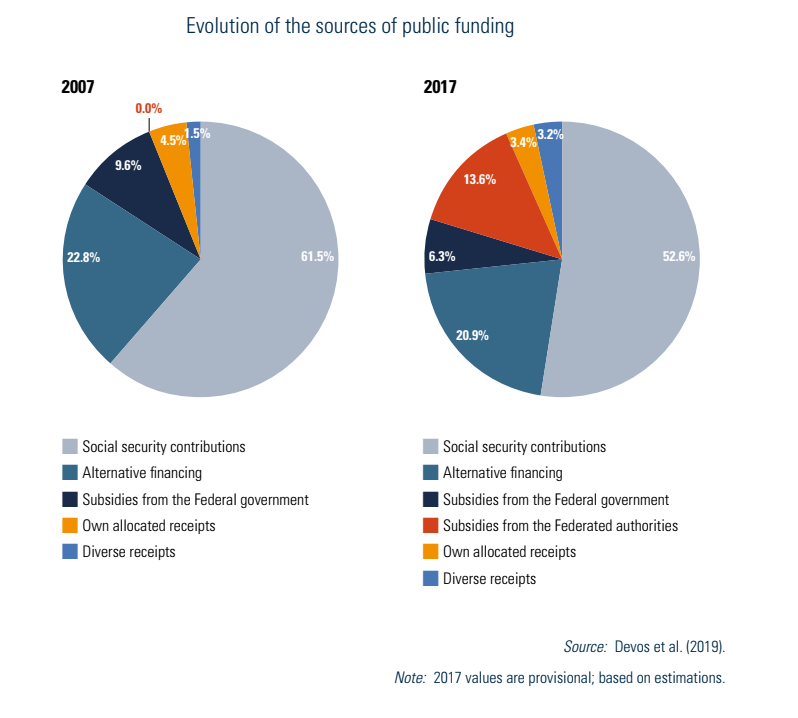

Public financing of the compulsory health insurance is only partly funded through this financial global management, the rest being financed by “own receipts”. Social security contributions are the main public funding revenue sources (52.6% of the public financing of health in 2017, based on KCE estimates) but their share has slightly decreased compared with 2007. The other sources of public financing of health include alternative financing (mainly from VAT), government subsidies, own allocated receipts and diverse receipts (see Fig3.7 and Devos et al. (2019) for details). The decrease in the share of social security contributions is the result of, on the one hand, an increase in direct government subsidies as a source of finance related to the transfer of competences to the Federated entities in the 6th State Reform, and on the other hand, a tax reform to lower labour costs, which in particular led to a reduction of social contributions from employers.

Fig3.7

Both in the general system and in the system for the self-employed, social contributions are proportional to income level and are independent of health risk.

In the general scheme, there are both employee’s and employer’s contributions, which are paid to the NSSO. They are based on a proportion of the entire gross income, which varies according to the statute of the worker (for example, working in the private or the public sector). As an example, for a person working in the private sector, the contribution is 13.07% and 24.92% of the entire gross income for employees and employers, respectively (for more details, see NSSO (2019)). In addition, a range of additional (special) social contributions for employers and reductions of social contributions for both employers and employees exist (NSSO, 2019).

Self-employed people pay their own social contributions to the Social Insurance Fund to which they are affiliated, which in turn forwards the contributions to the Social Security Office for Self-employed. In 2019, the social contributions of a self-employed person varied between €709.68 and €4067.20 per trimester according to their net income, excluding management costs of the Social Insurance Fund of approximately 4%; see FPS Social Security (2019b) for details and exceptions, such as for those with annual income below €7253.83. Since 2015, social contributions have been calculated on the basis of the income of the year itself. As this income is not yet known, the Social Insurance Fund initially requires a provisional quarterly contribution based on indexed income from three years ago.

A reform of the financing of this social security system was undertaken in 2017, among other things to better control the growth in public expenditure on health (see Box3.3).

3.3.3. Pooling and allocation of funds

To control expenditure, a real growth cap has been established since 1995 to determine the overall budgetary objective of the compulsory health insurance. This cap is determined based on the previous budgetary objective, increased by a real growth norm and indexed (health index). Variation in the real growth norm can be observed over time (4.5% in 2012 and 1.5% in 2019). It should be noted that this is a cap on an objective and not on actual expenditure, meaning that actual expenditure may exceed this estimated expenditure. A procedure is nevertheless established to detect early any budget overrun and thus take corrective measures to remain below the objective. The overall budgetary objective is broken down into partial budgetary objectives for each sector (e.g. physicians, hospitalizations, pharmaceuticals, etc.). The determination of these objectives and related measures are based on the procedures described in Box3.4.

To control actual expenditure and compare it to estimated expenditure, the so-called continuing audit procedure has been established. These audit reports contain information such as the evolution of expenditure for each sector, the difference compared with the budgetary objectives, or the impact of savings measures and initiatives of the government and of the conventions and agreements commissions. The Minister of Social Affairs and the General Council of the NIHDI (potentially after the advice of the Budget Control Committee) can suggest corrective savings measures at any time to prevent an overrun of the budgetary objectives.

The first attempt to adopt the 2025 overall budgetary objective of the compulsory health insurance failed in October 2024 when outgoing government representatives refused to approve the proposal to avoid interfering with the formation of the new federal government. The budget was not passed until February 2025, after the new government was formed. On 28 February 2025, the Council of Ministers adopted the 2025 budget, totalling over €45.22 billion. Corrective measures amounting to over €216 million were planned to prevent actual expenditure from exceeding the the overall budgetary objective. For example, about €73 million are to be saved by eliminating the reimbursement of physicians for teleconsultation by phone and reducing some specific fees, while about €113 million are to be saved in pharmaceutical spending.

More details can be found here: https://www.inami.fgov.be/SiteCollectionDocuments/budget_soins_sante_2025.pdf (in French) / https://www.riziv.fgov.be/SiteCollectionDocuments/gezondheidszorgbegroting_2025.pdf (in Dutch)

Authors

The Belgian health care system is generally known as being accessible and of high quality. The regular controls and feedback undertaken by the National Institute for Health and Disability Insurance (NIHDI) nevertheless provided a nuanced picture of the health system, especially in terms of appropriateness. A lack of long-term and cross-cutting health objectives was also highlighted (see also section 7.7 of the Belgium Health System Review – Transparency and accountability).

Therefore, on 1 March 2021 the NIHDI launched the project of developing a multi-year budget trajectory for health care that integrates health care objectives into health care insurance choices. By combining a dynamic multi-year budget framework with a greater focus on appropriate care (that is, the right care at the right time), the objective is to develop a medium- and long-term strategic vision of the compulsory health insurance and to provide the necessary resources to achieve these objectives. The aim is not about saving money, but rather about making the best use of available resources, improving the performance of the system, and having a long-term vision for effective care.

Three task forces have been set up on appropriate care, health care objectives and the dynamic multi-year budget framework including participation of many stakeholders and experts. A structured approach has been decided, that is, starting from general health objectives that are achievable in the longer term (strategic objectives) and determining more precise health care objectives that lead to concrete and achievable initiatives in the shorter term (operational short-term objectives).

Based on the preliminary work of the task forces, five priority area have been selected, that is, preventive care and chronic diseases, health care access, care pathways, mental health, and integrated care. The Quintuple Aim (QA) philosophy was then used as a guide for the strategic and operational objectives. Such QA describes the “underlying values” that will be pursued in these five selected priority areas, that is:

- Health status: Improve the health status of the population;

- Quality of care: Improve the quality of care as experienced by the persons in need of care and support;

- Cost-effectiveness: Based on the allocated resources, realize more “value” in terms of care and well-being for the persons in need;

- Social justice and inclusion: To achieve health equity, improve accessibility and make extra efforts for the most vulnerable; and

- Welfare of health professionals: Ensure that professionals in health care and welfare can perform their job properly and sustainably.

The 2022 budget of the compulsory health care insurance will be based on this new methodology and will foresee a financing of projects to achieve the defined objectives.

Authors

References

NIHDI 2021. Lancement de la trajectoire budgétaire pluriannuelle en 2021. (Launch of the multi-annual budget trajectory in 2021.) https://www.riziv-inami.fgov.be/fr/themes/financement/Pages/lancement-trajectoire-budgetaire-pluriannuelle-2021.aspx.

NIHDI 2021. Budget de l’assurance soins de santé : pluriannuel et dynamique à partir de 2022. (Health care insurance budget: multi-annual and dynamic from 2022.) https://www.riziv.fgov.be/fr/themes/financement/Pages/reunion_lancement_comite_assurance_elargi.aspx#:~:text=%E2%80%8BPourquoi%20une%20trajectoire%20pluriannuelle,sant%C3%A9%20%C3%A0%20partir%20de%202022

NIHDI 2022. Vers un budget pluriannuel pour les soins de santé assorti d’objectifs de soins de santé: Rapport du Groupe de travail Quintuple Aim. (Towards a Multi-Year Health Care Budget with Health Care Goals: Report of the Quintuple Aim Task Force.) https://www.inami.fgov.be/fr/publications/Pages/rapport-groupe_travail_quintuple_aim.aspx.

Authors

3.3.4. Purchasing and purchaser–provider relations

The budget for the compulsory health insurance is allocated between sickness funds so that they can make reimbursements and payments to their members. The sickness funds are paid each month based on their income and expenditure during the previous year (divided by 12). Over the years, sickness funds have been made increasingly accountable for the health expenditure and health status of their insured members (see Box3.5).

Health care providers in Belgium are not directly contracted by the sickness funds. They are independent and their practice is private, but they can commit to respecting the national tariffs (so-called conventioned physicians). These conventions and agreements are established to determine the official fees and cost-sharing mechanisms. These tariffs are specified in the nationally established fee schedule and are determined by the conventions and agreements commissions of the different sectors (see also Section 3.3.3). These commissions include both representatives of sickness funds and health care providers. Health care providers who accede to these agreements are called conventioned practitioners and must respect these tariffs in ambulatory care. Those who do not accede to these agreements and conventions are called non-conventioned practitioners and can ask for extra-billings (see Section 3.4 for more details). They may (or may not) renew this membership each time a new agreement is concluded. In exchange for this membership, they receive certain social benefits. For physicians, 84.3% of them acceded to the 2018–2019 agreement; see NIHDI (2018c) for details per specialty and district.