As noted in section 3.1, in 2019, the public share of funding for health care was 73.9%, with the remaining 26.1% of health spending coming from private sources.[8] Of the share of private expenditure, OOP expenditure (i.e. cost sharing and direct payments) accounted for 23.3%, with the rest coming from VHI (2.1%), payments made by companies (e.g. occupational medicine, 0.5%), and services offered by non-profit entities (e.g. health care for undocumented migrants, 0.2%).

Until 2019, private expenditure had grown over time, both in absolute terms (from €34.4 billion in 2012 to €40 billion in 2019) and in relation to total health expenditure (from 21.5% in 2010 to 26.1% in 2019). In particular, OOP expenditure steadily increased from €31.5 billion in 2012 to €35.8 billion in 2019, reaching a peak of €36.1 billion in 2018. This growing trend was interrupted in 2020, when OOP expenditure by households dropped to €33.9 billion (Del Vecchio et al., 2021).

Tax deductions may be an incentive for people to use services that incur OOP payments, since 19% of medical expenses exceeding the ceiling of €129.11 incurred in the previous year can be deducted from personal income tax (IRPEF). In 2019, 46% of taxpayers benefited from tax deductions related to health care costs (Del Vecchio et al., 2020). However, it is also worth noting that in Italy OOP expenditure is mainly borne by households directly rather than through other forms of expenditure brokered by third-party payers – for example, VHI purchased by individuals or companies for their employees (see section 3.5).

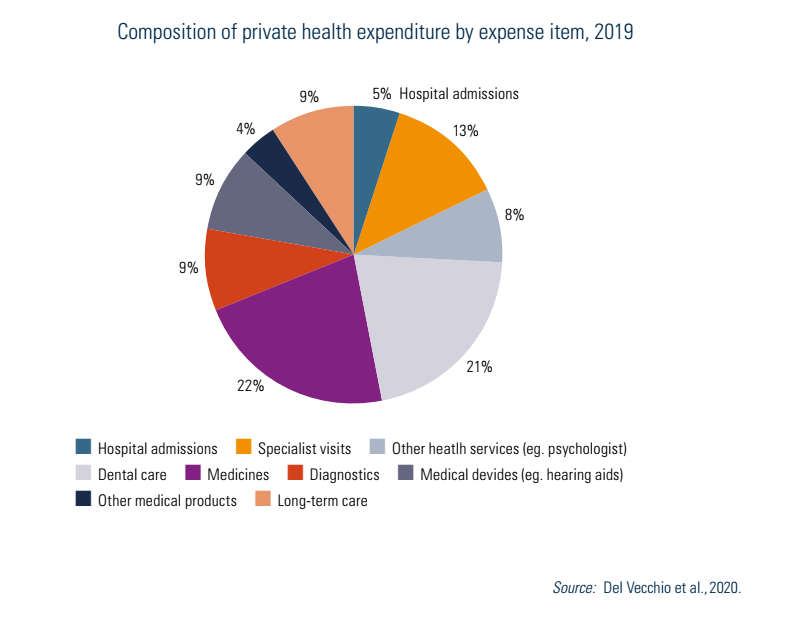

Fig3.6 provides a more detailed breakdown of private health expenditure by function. Total private health expenditure (in 2019) was made up of 65% of spending on services, divided between hospital services (14.3%, including hospital admissions and long-term care) and outpatient services (50.7%), of which dental care represents the predominant component (21.2%), followed by specialist visits (13.2%). The remaining 35% is devoted instead to health care goods: medicines (22%), therapeutic equipment (9%, of which eyeglasses, contact lenses and hearing aids make up the bulk) and other medical products (4%). All these components showed a reduction in 2020 (−9% for hospital service, −6% for outpatient services, −1% for health care goods) (Del Vecchio et al., 2021).

Fig3.6

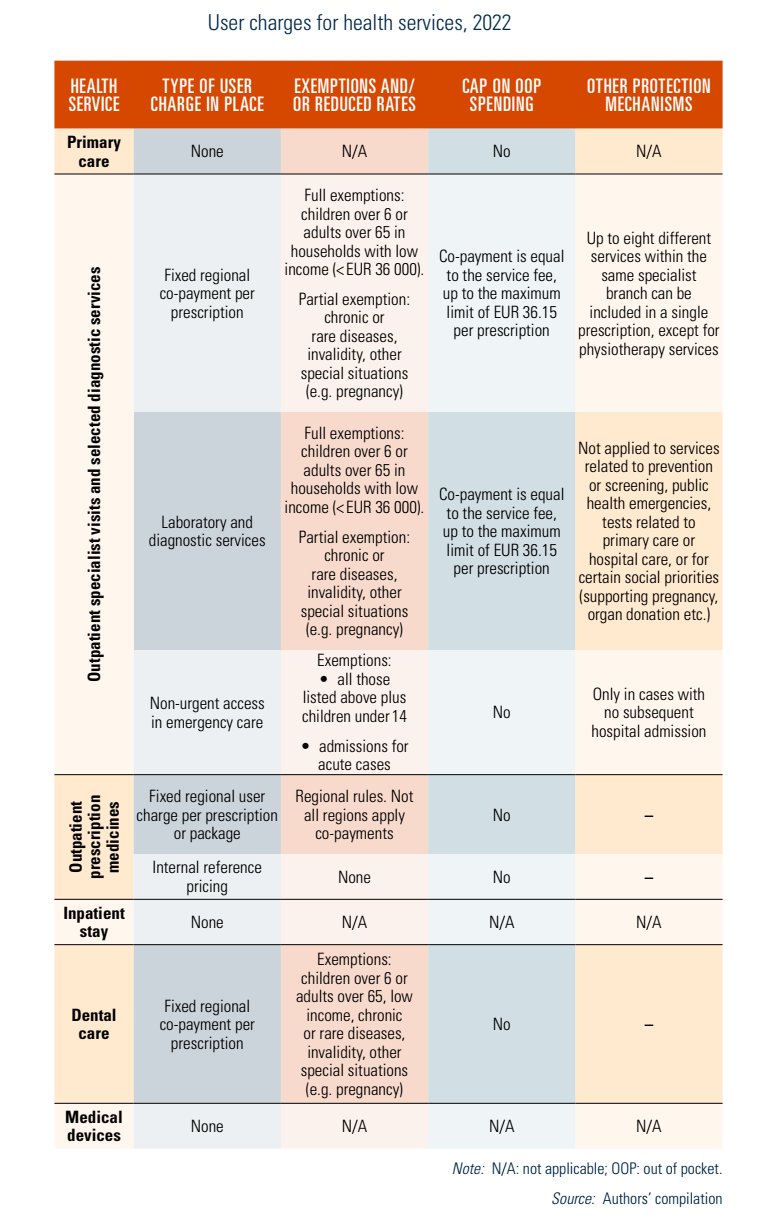

In Italy, co-payments are made up of two broad categories: 1) co-payments for goods (i.e. medicines) and 2) co-payments for services (e.g. outpatient specialist services, some laboratory and diagnostic tests, and non-urgent access to emergency care). The cost sharing for medicines is further divided into: 1) a fixed amount user charge (known as the “ticket”) per package, which is set by regions, and 2) the difference between the market price and the reimbursement price for off-patent medicines (i.e. internal reference pricing). There are several exemption categories (e.g. by age or income level) but no overall annual cap on co-payment spending or other major financial protection mechanisms. Primary and inpatient care are totally free at the point of use for everyone (Table3.3).

Table3.3

In 2019, the level of co-payment spending was estimated at €2.9 billion and has been stable both in absolute terms and as a percentage of household consumption expenditure between 2009 and 2019, despite the introduction of an additional user fee of €10 (with regional variations) charged on specialist outpatient services between 2011 and September 2020 (known as the “super ticket”). The only relevant growth concerned the revenues deriving from internal reference pricing differences, which increased from €0.4 billion in 2009 to €1.1 billion to 2017 (Del Vecchio et al., 2020). This data suggests that policies aiming to incentivize the prescription and use of generics were not so effective in deterring the consumption of branded drugs, with a consequent increase in the financial burden on households. In 2020, the level of co-payment spending dropped to €2.3 billion. This was particularly evident for outpatient services (from €1.3 billion in 2019 to €0.8 billion in 2020), and in line with the overall trend of the other private expenditure components (Del Vecchio et al., 2021) (Fig3.7).

Fig3.7

Cost sharing for reimbursable medicines (Class A) includes two different forms of payment. The first component (“ticket”) is a fixed user charge per package (or per prescription) set by the regions. In 2000, all forms of patient contributions to pharmaceutical expenditure were abolished at the national level, so medicines are categorized as either totally free (Class A) or paid for in full (Class C). However, most regions introduced a user charge system for Class A medicine purchases, which generally consists of a fixed amount per package, although variations do occur. For example, in some regions, the amount of the user charge per pack increases according to family income, while in others it is adjusted to the cost of the medicine and whether the generic (lower cost) or the branded medicine (higher cost) is prescribed. Some regions also apply a fixed amount to be paid per prescription which is added to the amount per package (e.g. Basilicata) or a maximum amount to be paid for each prescription (e.g. Lombardy), or both (e.g. Puglia). Regions also specify exempted categories; in some cases, these categories also pay a user charge, but a lower amount (partial exemption). Lastly, there are regions that do not apply any user charges on medicines or have progressively reduced or abandoned them. For example, in 2019, Emilia-Romagna abolished the “super ticket” for households with income below €100 000 and also abolished co-payments on first visits for families with two or more children; similarly, Piedmont abolished the “ticket” following other regions, such as Friuli-Venezia Giulia, Marche and Sardinia.

The second component of cost sharing for medicines is internal reference pricing, which consists of asking the patient to pay the difference between the branded medicine price and the lowest price among all the equivalent drugs available in the regional market. The defining feature of this type of cost sharing is that the payment derives from consumer choice, in cases where individuals prefer to buy a branded drug, or from physician choice, in cases where the doctor indicates that the medicine should not be substituted on the prescription. A few regions (Liguria, Veneto, Bolzano, Molise, Calabria, Sicily) have also established restricted exemption categories (e.g. war invalids, victims of terrorism) which do not pay the price differential.

The services for which co-payments are required are: 1) specialist visits, and diagnostic and laboratory exams provided by public and private providers; 2) non-urgent access to emergency rooms (known as “white codes”), only if the attendance is not followed by hospital admission; and 3) thermal therapies (see also Table3.5).

Table3.5

Conversely, cost sharing is not applied to: 1) diagnostic and laboratory exams included in early diagnosis and collective prevention programmes organized by regions (e.g. HPV testing for cervical cancer screening); 2) diagnostic and laboratory exams performed during epidemics to protect collective health (e.g. nasal swabs for the diagnosis of COVID-19); 3) GP and paediatrician visits and examinations; 4) treatments provided during a hospital stay, including admissions to rehabilitation wards or post-acute long-term care facilities, and the examinations strictly and directly connected to the planned hospitalization and previously provided by the same hospital (e.g. visit with the anaesthetist, electrocardiogram, etc.).

Moreover, co-payments are not levied on services provided in situations of particular social interest, such as: 1) maternity care; 2) preventing the spread of HIV, limited to ascertaining the state of infection in individuals belonging to categories at risk; 3) promotion of blood, organ and tissue donations, limited to services related to the donation activity; 4) protection of individuals injured by irreversible complications due to compulsory vaccinations, transfusions and administration of blood products; and 5) vaccinations included in the National Vaccine Prevention Plan (Piano Nazionale Prevenzione Vaccinale, PNPV) for individuals identified as recipients.

In the area of cancer prevention, the following examinations can be received without co-payment: mammography, every two years, for women aged between 45 and 69 years; cervical-vaginal cytological examination (Pap smear), every three years, for women aged between 25 and 65 years; colonoscopy, every five years, for the population aged over 45 years. In addition, HIV tests are anonymous and free in public facilities.

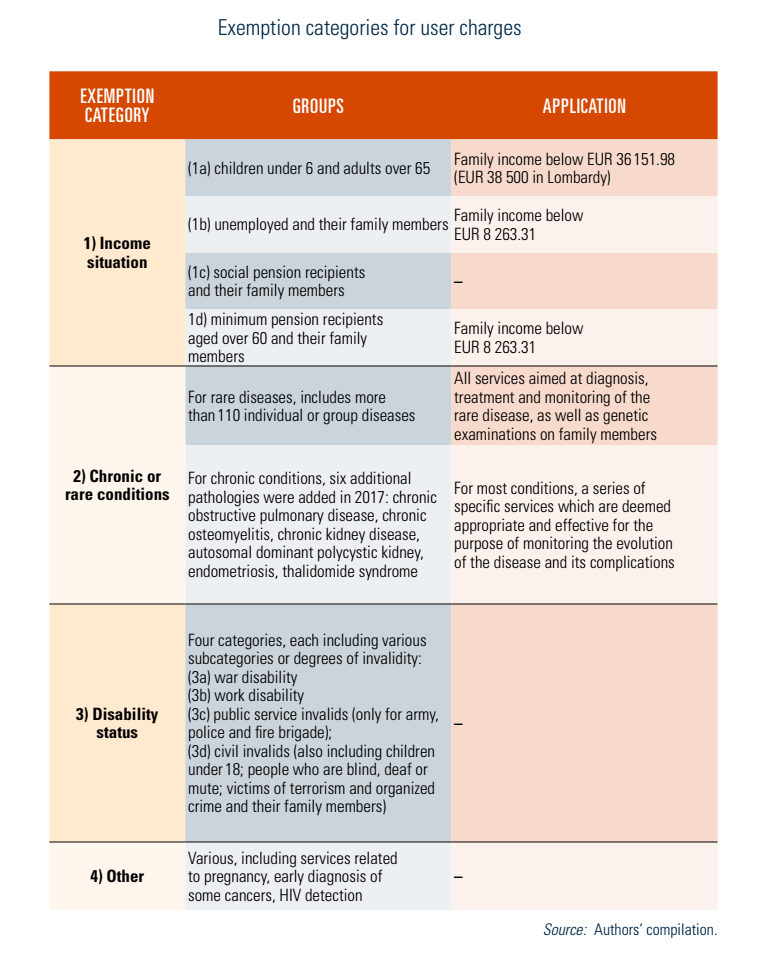

In general, for all health services that do require a co-payment, patients are entitled to exemption (for some or all services) in the following cases: 1) particular income situations associated with age or social condition; 2) people affected by certain chronic or rare conditions; 3) recognized disability status; and 4) other (e.g. pregnancy, early diagnosis of some cancers, HIV detection) (Ministero della Salute, 2021c). These are summarized in Table3.6.

Table3.6

Co-payments (of varying amounts depending on the region) are levied for interventions provided by emergency rooms to patients classified as “white codes” (i.e. non-urgent services, patients with non-critical conditions) not followed by hospitalization. For this co-payment the same exemption rules as outpatient specialist services apply with the addition of children under 14 years (Table3.5).

Direct payments refer to payments by users to purchase health care services and OTC medicines that are not covered by the SSN. Given that in 2019, the level of co-payment spending was estimated at €2.9 billion, out of a total OOP expenditure (i.e. co-payments and direct payments) of €35.8 billion (section 3.4.1), it is clear that the overwhelming majority (92%) of OOP spending in Italy is attributable to direct payments (€32.9 billion).

There is no evidence of informal payments in Italy.