-

15 April 2024 | Policy Analysis

Reform to reduce dual VHI coverage for surgery

3.5. Voluntary health insurance

Context

More than 80% of Israeli residents covered by national health insurance (NHI) also have voluntary health insurance (VHI). VHI in Israel is mainly duplicative and is used to access care provided by private hospitals and private health professionals, to shorten waiting times or to choose a particular surgeon. VHI may also be supplementary in order to access services not covered by NHI, such as specific pharmaceuticals or dental care. VHI in Israel is not complementary, as it does not cover user charges for NHI-covered services (Sagan & Thomson, 2016).

There are two types of VHI. The first type is a group insurance marketed by HPs to their members, known as HP-VHI, and the second type is commercial VHI (individual or group insurance) sold by for-profit insurers. HP-VHI provides benefits in-kind while commercial VHI reimburses patients in cash, with higher reimbursement rates than HP-VHI. Commercial VHI premia are higher than HP-VHI, which are based only on age. In addition, HP-VHI does not require medical underwriting and must cover any interested individual. About half of the adult population own both types of VHI, resulting in dual VHI coverage for some aspects of care (Laron, Maoz Breuer & Fialco, 2022 ). Dual coverage leads to an unnecessary financial burden on households and in 2018, VHI premiums represented 40% of households’ private spending on health (Central Bureau of Statistics, 2023).

Several reforms have attempted to regulate and reduce inefficiencies in the VHI market (see https://eurohealthobservatory.who.int/monitors/health-systems-monitor/analyses/hspm/israel-2015/changes-to-improve-the-commercial-vhi-market). A change from 2021 attempted to reduce dual VHI coverage, increasing competition among commercial insurers, and enhancing transparency for informed VHI purchase (for example, making policies easier to understand and compare, reducing barriers to switching insurers). A uniform and basic policy for surgical insurance was also introduced, with the option to purchase additional insurance coverage separately, for example, for surgeries abroad, pharmaceuticals or to cover the treatment of severe diseases. (Capital Market Authority, Insurance and Savings, 2018).

Impetus for the reform

The Committee for the Empowerment of Health Services in Israel, and the regulation of the public and private health system, headed by Prof. Nachman Ash, recommended a set of policy changes to reduce inefficiencies in the VHI market in 2023. The government approved the committee’s recommendations.

Main purpose of the reform

To reduce inefficiencies and dual VHI coverage for surgical care, to reduce premiums, and to curb the revenues of commercial insurers.

Content/characteristics

Government decision 198, taken on 24.02.2023 (Ministry of Health, 2023)

- In case of dual coverage for surgery in private hospitals, the commercial insurer will always bear the cost of the surgery. The patient can apply directly to the commercial VHI for reimbursement, or the commercial insurer reimburses the HP-VHI using the surgery (private) tariff set by the MoH’s price list. Reimbursement will be coordinated via an exchange of information between the commercial VHI and the HP-VHI.

- From 11 March 2024, commercial insurers are not permitted to sell overlapping/dual VHI. Commercial insurers can only sell a “HP-VHI complementary commercial policy for surgery” instead of the “regular commercial VHI for surgery”. The HP-VHI complementary policy only covers the costs of surgery beyond the coverage of the HP-VHI. This would include materials and products not covered by the HP-VHI, any out-of-pocket costs due to HP-VHI cost sharing (Capital Market Authority, Insurance and Savings, 2024).

- From June 2024 commercial insurers must automatically move insured persons from the “regular commercial VHI for surgery” to the “HP-VHI complementary commercial policy for surgery” when their current policy is up for renewal. Policies are usually renewed every two years, and there is an option to opt out from the change (Capital Market Authority, Insurance and Savings, 2024)

Authors

References

Capital Market Authority, Insurance and Savings (2018). Health Insurance Reform – In-Depth Review. Available at https://www.gov.il/BlobFolder/reports/head-of-the-authority-reports/he/Home_memone-reports_2017_report2017_3.1-review.pdf

Capital Market Authority, Insurance and Savings. (2024, 3 11). Amendment to the Unified Circular Instructions – Section 6, Part 3, Chapter 2 – Obligation to Propose Supplementary Insurance Coverage to HP-VHI. Jerusalem.

Capital Market Authority, Insurance and Savings. (2024, 03 11). Transferring insured individuals to a supplementary אם HP-VHI surgery insurance policy. Jerusalem. Retrieved from https://www.gov.il/BlobFolder/dynamiccollectorresultitem/notice-2023-060/he/health%20regultion_110324.pdf

Central Bureau of Statistics (2023) Households income and expenditures survey 2021, summary of findings. Available at: https://www.cbs.gov.il/he/publications/DocLib/2023/1924_household_income_expenditure_2021/h_print.pdf

Laron, M., Maoz Breuer, R. & Fialco, S. (2022). Population Survey on the Level of Service and Health Care System Performance in 2021–2022. Jerusalem: Myers-JDC-Brookdale Institute. Retrieved from https://brookdale.jdc.org.il/en/publication/population-survey-on-the-level-of-service-and-health-care-system-performance-in-2021-2022

Ministry of Health. (2023, 02 24). decision 198: Reducing the phenomenon of insurance duplication in private health insurances (in Hebrew). Jerusalem. Retrieved from https://www.gov.il/he/pages/dec198-2023

Sagan, A. & Thomson, S. (2016). Voluntary health insurance in Europe: Country experience. In Observatory Studies Series (Vol. 42). http://www.euro.who.int/__data/assets/pdf_file/0011/310799/Voluntary-health-insurance-Europe-country-experience.pdf?ua=1

3.5.1. Market role and size

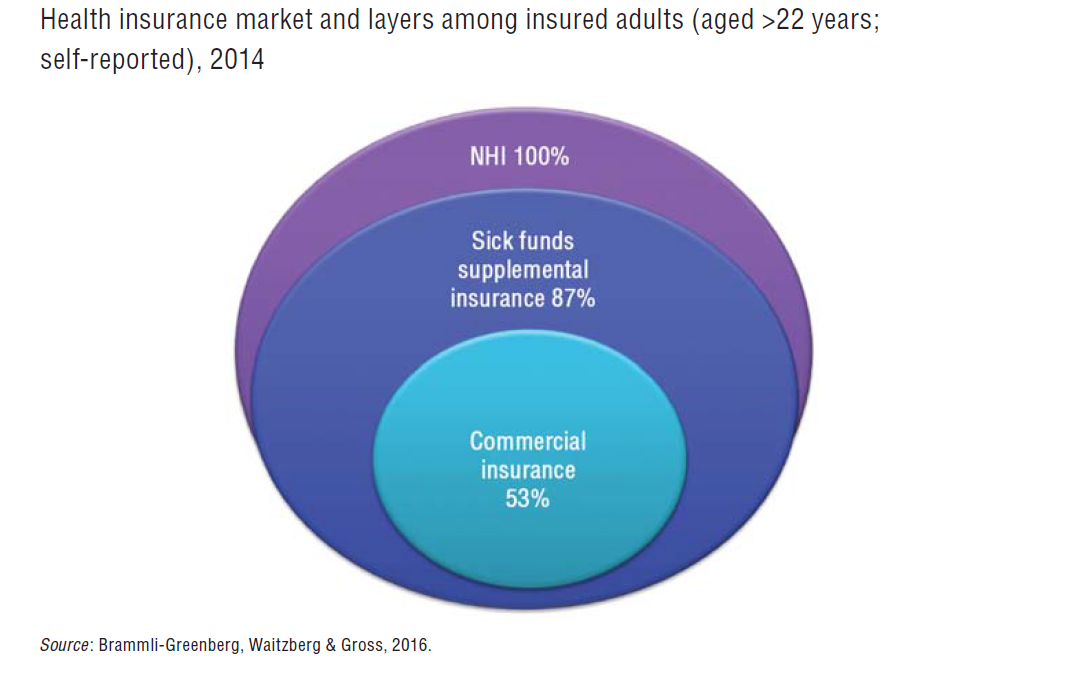

Over and above the NHI, two forms of VHI are available in Israel: supplementary insurance, offered by the HPs to all of their own beneficiaries (HP-VHI); and commercial insurance offered by commercial insurance companies to individuals or groups. Even though the Israeli NHI benefits package is broad compared with that in other OECD countries, Israel’s VHI market is still one of the largest. In 2014, 87% of Israel’s adult population had HP-VHI, and 53% had commercial insurance (Brammli-Greenberg & Medina-Artom, 2015). In 2010, this was higher than in all other OECD countries except for France and the Netherlands (OECD data for 2010).

The share of the Israeli population covered with VHI has been growing rapidly since the early 2000s, and it is the fastest growing component of private health care spending. Between 2002 and 2011, household spending on supplemental insurance increased by 70% and on commercial insurance by 90% (Ministry of Finance, 2012; Ministry of Health, 2012). The payments for premiums of both supplemental and commercial health insurance increased by more than 100% from 2005 to 2013, compared with an increase of 18% in other insurance sectors. The Israeli per capita expenditure on private insurance in 2005–2012 skyrocketed by 111%, much faster than the average of 39% in OECD countries.

According to the Ministry of Health, the VHI market is not achieving the goal of financing health care privately while reducing OOP payments: household expenditure on health care has not changed since the early 2000s except for the sharp increase in spending on VHI premiums (Ministry of Health, 2012). Along with the increase in the number of VHI policyholders in recent decades, Israel witnessed an expansion of dual coverage: in 2014 50% of the adult population owned the two types of VHI, up from 5% in 1995 and 30% in 2005 (Brammli-Greenberg & Medina-Artom, 2015; Brammli-Greenberg, Waitzberg & Gross, 2016). It is worth noting that all the VHI owners are also covered by NHI. Multiple and dual coverage may be contributing to increases in THE, including in private spending (Brammli-Greenberg & Waitzberg, 2014). The Ministry of Health has included among its strategic goals restraining the growth in VHI ownership, and strengthening the public system.

One of the possible reasons for the high demand for VHI in Israel is the low trust and confidence in the public health care system. In 2014, about 50% of the adult population (aged 22 years or more) reported that they were confident or very confident that they would receive the best and most effective treatment. Only 40% reported that they were confident they would be able to afford the treatment needed. In these two measures, Israel had the lowest score of all 11 countries in the 2010 Commonwealth Fund survey. This could be due, in part, to differences in terminology between the surveys, with the United States survey (and perhaps the surveys in other countries) asking about confidence in the system’s ability to meet their needs, and the Israeli survey using a Hebrew term that has connotations of both confidence and certainty (Brammli-Greenberg & Medina-Artom, 2015).

Another reason for the broad VHI coverage is that it is used by insurees to “jump queues”, both for elective surgery and for specialist consultation in the community. Insurees can receive faster access to elective surgery in private hospitals and can visit specialists in their private clinics – both financed by their VHI. This is instead of waiting for the public services provided by HPs under the NHI law.

3.5.2. Market structure

In 2014, 87% of the adult population had HP-VHI, and 53% had commercial insurance (Brammli-Greenberg & Medina-Artom, 2015). Residents can only purchase HP-VHI from their HP. There is some variation in coverage rates among HPs ranging from 91% in Maccabi and 86% in Clalit to 77% in Leumit and Mieuhedet (in 2014) (Brammli-Greenberg & Medina-Artom, 2015). HP-VHI is considered by the insured as part of the public health care system, and coverage is high among almost all the population, including among vulnerable population groups apart from Arabs: 92% among the chronically ill, 90% among older people, 85% among immigrants from the former USSR, 81% among the lowest income quintile and only 54% among Israel’s Arab citizens (Brammli-Greenberg & Medina-Artom, 2015; Brammli-Greenberg, Waitzberg & Gross, 2016).

Commercial VHI offers individual and group policies. Commercial cover is offered mainly by five insurers, who account for 97% of commercial premiums. There are two types of buyer in the commercial market: people who buy their policies directly from an insurer for a risk-rated premium based on age, gender and pre-existing conditions (for whom enrolment is dependent on medical underwriting); and organizations (e.g. employers, labour unions) who purchase group policies for their members for a community-rated premium, reflecting the risk level of the group. Group premiums are lower than individual premiums for the same level of coverage, and usually less profitable.

The demographic profile of people with commercial VHI differs somewhat from that of those with HP-VHI, in that they tend to have higher incomes and better health (Brammli-Greenberg, Waitzberg & Gross, 2016). In the commercial market for VHI, limitations not related to price (e.g. coverage limits, waiting periods, risk-rated premiums, the exclusion of pre-existing conditions and the rejection of applications for cover) serve as a means of selecting healthier people and rejecting or charging higher premiums to less healthy people (Shmueli, 1998, 2001).

3.5.3. Market conduct

HP-VHI

VHI offered by the HPs (HP-VHI), called in Hebrew “supplemental insurance”, plays several roles in the health system. It can provide: (a) complementary services (that are not included in the NHI benefits package) such as adult dental care or alternative medicine; (b) supplementary services that are covered by NHI, but only to a limited extent (e.g. IVF and physiotherapy); or (c) reimbursement for care purchased in the private sector that provide enhanced choice of provider, faster access or improved facilities (Brammli-Greenberg, Waitzberg & Gross, 2016). It does not include “substitutive” insurance for people excluded from the NHI system or coverage for user charges and co-payments in the public system.

Since the mid-1990s, there has been a substantial increase in the range of services covered by HP-VHI. Whereas initially these packages focused on services that were nonmedical (e.g. recuperative care), the newer services include many that are definitely medical in nature (such as advanced oncological and prenatal tests).

HP-VHI is a standard package of supplemental insurance offered by each HP to all of its policyholders, with relatively low fees that are determined solely by age (and not influenced by health status). No policyholder can be denied coverage, and HPs are prohibited from excluding pre-existing conditions. HP-VHI packages and rates must be approved by the Ministry of Health.

Since 2007, all HPs have developed a second layer of VHI coverage with extended coverage such as organ transplantation abroad and more genetic testing during pregnancy, which they have marketed for an additional premium. One of the HPs even created a third layer in 2013, which included aesthetic procedures, dental care and physical activity promotion. However, it later had to cancel its first layer in order to remain with two layers, as in all the other HP (Brammli-Greenberg, Waitzberg & Gross, 2016).

Commercial VHI

Commercial insurance is not considered part of the publicly funded health system. It is offered by private insurers who are free to insure any medical service but who can offer cash benefits only. Commercial plans cover dental care and catastrophic events (such as transplants, operations abroad and LTC), as well as financial compensation for services in the private sector. Many of the policies also cover medications not covered in the NHI benefits package. They usually offer higher indemnity payments and greater choice of provider than HP-VHI. Consequently, commercial VHI has become an additional layer of insurance rather than an alternative to supplemental insurance, resulting in less direct competition between the two parts of the market (Fig3.9) (Brammli-Greenberg & Gross, 2003).

Fig3.9

Life-saving medications

Currently only commercial VHI can cover life-saving medications that are not in the NHI benefits package. HPs attempted to include these medications in their policies in 2007. Adding these benefits in the supplemental coverage put the HP in direct competition with commercial insurers, particularly as they can offer coverage more cheaply than commercial insurers. However, in 2008 the Ministry of Health and the Knesset prohibited HPs from doing so on the grounds that it would lead to inequality in access to health care (for those who do not own VHI) and would weaken the public pressure to add new medications to the NHI benefits package. The Ministry of Finance also feared that the change would increase total spending on health (Gross & Brammli-Greenberg, 2004). This debate was brought back onto the public agenda in 2014 (see section 6.2), and the Ministry of Health is currently considering allowing HPs to include coverage for life-saving medications in their VHI.

3.5.4. Public policy

The Ministry of Health regulates HP-VHI, while the Insurance Commissioner at the Ministry of Finance regulates commercial VHI. In mid-2015, the government’s policy is to allow both HPs and private insurers to offer VHI, with the proviso that the HPs do not offer LTC insurance.[12] In addition, the HPs must operate supplementary VHI under separate financial accounts and may not use NHI public funds to cross-subsidize supplementary VHI.

In practice, however, in some years the HPs have used profits from supplementary VHI to help to offset deficits in the NHI-related part of their activity. Lately, the HP-VHI has been perceived, and used more intensively, as a competitive tool by HPs seeking to attract low-risk and low-cost insured. They started offering benefits that are particularly attractive to young and healthy people, as well as large and young families. These included vaccinations for travellers (e.g. for tropical diseases), pregnancy diagnostic examinations, optical services for children and diagnostic examinations for child development, such as for attention deficit hyperactivity disorder. By offering such benefits, the HPs hope to earn more from supplemental premiums, and to increase the plan’s enrolment of young families, thus to earn more governmental funds from the NHI capitation formula (Brammli-Greenberg, Waitzberg & Gross, 2016).

Addressing dual coverage

One of the reasons for the dual coverage phenomenon is information asymmetry: Israelis lack knowledge about the coverage they are entitled to in each type of insurance, and about how to realize their benefits. Another factor may be that a significant portion of the Israeli public is not confident that their needs will be met if they become seriously ill (Brammli-Greenberg & Medina-Artom, 2015). This problem is reflected in the limited utilization of services covered both by NHI and VHI. However, sometimes VHI divert (profitable) services from the public to the private system (Brammli-Greenberg et al., 2014).

The phenomenon of dual coverage has led to concerns that many consumers may unknowingly be paying twice for insurance for the same risk (particularly private operations). As a result, the Insurance Commissioner has recently required commercial insurers to also offer policies that add to, rather than duplicate, the coverage available via the HP-VHI packages.

In order to tackle the lack of information, the Ministry of Health launched a website in 2014 that gives access to transparent information about the coverage of the NHI and VHI benefits packages (see section 2.9). The idea is to empower insurees with knowledge and awareness of their rights and eligibility to benefits so they can demand them from the HPs and/or private insurers; if refused, they can refer the case to the supervisor (the Ministry of Health). This policy instrument addresses market failures related to information asymmetry and can potentially improve competition among the HPs and within the VHI market (Brammli-Greenberg et al., 2014).

In view of the increasing dual coverage, the Insurance Commissioner is currently consolidating a series of changes in commercial VHI in order to combine the commercial VHI market with the HP-VHI market. In 2014, the Insurance Commissioner expanded the allowable commercial insurance coverage to include, apart from surgery, also consultations with specialist physicians, alternative treatments, choice of surgeon (by covering the surgeon’s fee in private hospitals) and other costs of private surgery. The change aimed to increase the competition of commercial VHI with HP-VHI, since these services were already provided by the latter. The Insurance Commissioner also created a “standard” policy with uniform coverage, including new technologies, and uniform premiums by age group. The main coverage is private operations, which is the main reason that people buy VHI in Israel. The premiums and co-payments can vary only based on individual risk, gender and health condition (Ministry of Finance, 2014, 2016). In the future, this standard policy will be marketed also by HPs. The intention is to offer low-risk people a cheaper policy with unique basic coverage and thereby increase competition in the VHI market both among commercial insurance companies and between these companies and HPs. The standard policy also increases transparency in the VHI market and makes it easier for consumers to make comparisons among insurers. With greater competition and the same types of coverage, insurees might be able to make wiser choices of type of insurance and might give up dual coverage.

- 12.The HPs may market LTC insurance policies offered by the private insurers but cannot serve as the insurer for these policies.